Indian IT services stocks have been weighed down in recent months by concerns about the disruptive potential of generative artificial intelligence (‘AI’) post-release of OpenAI’s ChatGPT and Microsoft’s (MSFT) ChatGPT-powered Bing search engine. Given the structural margin implications, the sector-wide de-rating seems justified to me. While these companies have reinvented themselves over the years and driven higher tech spending over the years, these shifts tend to be deflationary for client spend and, thus, disruptive for margins. Plus, catching up will require a step up in investment and reskilling to build the right competencies.

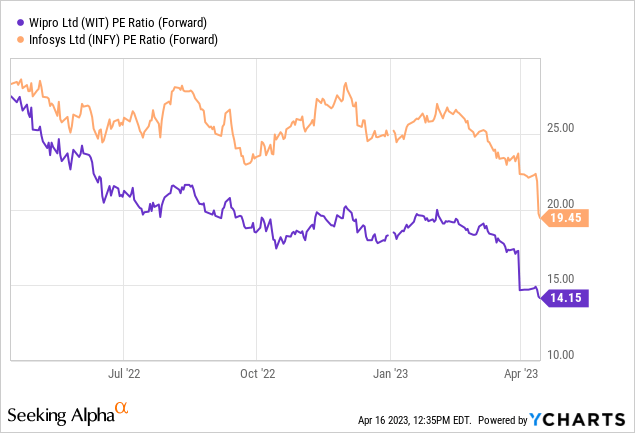

Yet, generative AI could also unlock new revenue streams as more firms look to integrate this into their tech stacks to reap the productivity benefits. Either way, there will be winners and losers from this trend; the superior hiring and training capabilities at bigger firms like Infosys (INFY) should allow it to gain share vs. smaller players like Wipro (NYSE:WIT). With growth for the sector also slowing amid a broader macro slowdown, Wipro’s revenue base could come under further pressure in the coming months without new major deal wins. On a relative basis, the current valuation discount to Infosys seems justified; I would remain neutral here.

Generative AI Innovation Poses Downside Risk for Margins

The release of OpenAI’s generative AI model ChatGPT has sparked an acceleration in the AI race, with Microsoft also unveiling an AI-powered Bing search engine and Edge browser, having expanded its OpenAI stake. The ‘new Bing’ now offers capabilities such as personalized content creation and fairly good summarization (with sourcing), as well as options to follow up on search queries. Given this is only the first instance of a major enterprise incorporating generative AI into its tech stack, there is clear disruptive potential across industries. IT services companies like Wipro are particularly vulnerable – a productivity tool that simplifies and democratizes coding capabilities will inevitably cut into its value proposition.

At first blush, a shift toward generative AI at the enterprise level would be a net negative for margins. Not only does it reduce the need for outsourcing, but any productivity savings for customers are unlikely to flow through to Wipro’s P&L. Also concerning is the implication for operating expenses – building the right capabilities to adapt to generative AI demand likely entails new investments in infrastructure and reskilling existing staff. IT consulting firms further up the value chain, like Accenture (ACN), could gain share. Within the Indian IT services space, larger firms like Infosys and Tata Consultancy Services (OTCPK:TTNQY) have access to a stronger graduate pool and better training infrastructure, as well as bigger budgets, so they could compound the share losses for smaller firms like Wipro.

Silver Linings from the Generative AI Wave

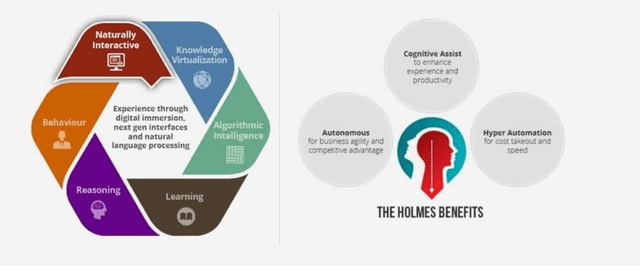

Whether the near to mid-term AI headwind translates into structural pressures is less clear-cut, in my view. The Indian IT services industry has proven its resilience over the years, successfully adapting to new trends from packaged solutions to the digital/cloud transition. None of these shifts have come easy and required hefty reinvestments or M&A to build up the right capabilities at scale. Yet, their partnerships across all the major hyper-scalers and growing role in cloud adoption have emerged as new growth drivers in the face of slowing legacy growth. Plus, AI isn’t a new trend, and even though ChatGPT risks downsizing the legacy Indian IT services pie, companies will still need help integrating generative AI technologies in their tech stacks and reskilling their employees. Alongside the two leaders, Wipro currently has its ‘Wipro Holmes’ platform to tackle the AI addressable market, though it will face stiff competition from TCS’ Ignio and Infosys’ Nia.

Wipro

Internally and externally, the productivity benefits of generative AI will be a tailwind to Wipro’s margins as well via lower staff headcount and costs. In the near term, though, the narrative around ChatGPT’s disruptive potential for the Indian IT services business model and margins will likely weigh on investor sentiment. Alongside a pending macro slowdown across key North America and EU markets, expect the sector to come under further valuation pressure, with Wipro’s relative discount likely to widen in tandem.

ChatGPT Disruption Looms Large

Along with the broader Indian IT services space, Wipro has seen protracted stock price declines in recent months amid cyclical macro concerns and, most worryingly, structural headwinds from generative AI. To be clear, deflationary tech isn’t new, and thus far, tech spending has continued to ramp up over the years, driving equity upside for the sector. But initial shifts tend to be disruptive for margins, and given the need for investment and to reskill to build capabilities to meet new enterprise demands related to generative AI, profitability could suffer in the meantime. Heading into a potentially turbulent period for IT services, larger firms like INFY, with stronger hiring and training capabilities, should weather the storm better than smaller peers like Wipro. With Wipro’s market share gains post-CEO reshuffle also slowing alongside its large deal pipeline, the relative valuation discount to Infosys seems justified.

Read the full article here