")

Medical Properties Trust (NYSE:MPW) is managing its poor liquidity position by performing asset sales, a profile that is not sustainable, and a serious liquidity crunch can happen in the coming quarters.

As I’ve analyzed in previous articles, I have been bearish on MPW over the past year, due to its fundamental issues that led to a significant dividend cut and because I have serious concerns about its ongoing cash burn. Since my first article on MPW in March 2023, its shares are down by more than 50%, including dividends, while the market went up by more than 28% during the same time frame.

MPW coverage (Seeking Alpha)

In this article, I update MPW’s recent events and analyze its liquidity issues in the coming quarters, which can lead to serious financial distress ahead.

Recent Events & Liquidity

Since my last article on MPW, back in October 2023, the company announced intentions to improve its liquidity position by potentially doing some asset sales or evaluating joint venture opportunities, plus it was also considering to raise secured debt financing. The company expected to raise some $2 billion in funding over the following twelve months, which would be more than enough to cover its debt maturities over the next couple of months.

As I’ve analyzed in detail in a previous article, MPW’s cash flow generation and liquidity position are not great, thus one of my key concerns is its cash burn that could lead to a financial distress situation during 2024.

If MPW were able to raise new funding in the expected $2 billion amount, this would certainly be a great step in the right direction, but so far the company has been able to only raise about $500 million through the sale of assets and a loan investment. Given that it has now passed almost six months since this announcement, this raises serious questions about MPW’s ability to raise new funds, particularly secured bank loans.

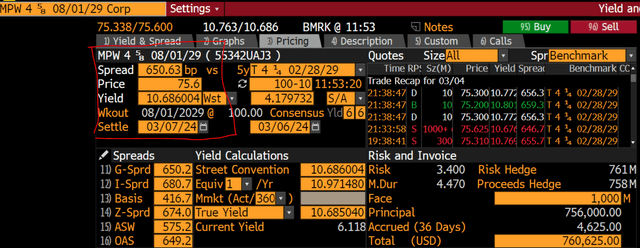

Indeed, market concerns about the banking industry exposure to the Commercial Real Estate (CRE) sector don’t help MPW to raise secured loans, while raising new bonds in the capital markets remains at prohibitive levels. For instance, its senior bonds that mature in 2029 are currently trading with a yield-to-maturity of around 10.7%, thus issuing new bonds doesn’t seem to be an option for the company due to very high potential costs.

2029 Bond (Bloomberg)

Investors should also note that MPW’s credit rating is ‘high yield’, thus it’s not likely that MWP’s funding costs will come down significantly in the short term, even if the Federal Reserve eventually starts to cut interest rates in the coming months.

Beyond its refinancing issues, MPW also announced a couple of months ago that its largest tenant Steward Health Care System only paid 25% of rent and interest owed in Q4 2023, which is another headwind for MPW’s liquidity profile in the short term. For investors who follow MPW closely, this was not surprising, as there were concerns about Steward’s financial profile over the past few years, thus it was only a matter of time until Steward would become a major problem for MPW.

As I’ve covered previously, MPW’s exposure to Steward goes beyond rental income, given that MPW has financed its tenant for years and has several real estate ventures together with its largest tenant, plus other equity and loans investments in its balance sheet. This means that MPW has almost $1 billion exposure to Steward in its accounts, on top of about 20% of its annual rental income generated from Steward.

With its largest tenant now publicly in financial distress, it makes it even more difficult for MPW to raise new funding, thus I think it will be tough for the company to raise $1.5 billion during 2024, as the company expects. This means that MPW most likely will continue to do asset sales to raise cash, and will also use its own cash flow from operations to finance upcoming debt maturities.

However, as I’ve discussed several times before, its cash flow from operations is not enough to cover its capital expenditures and dividend payments, leading to negative free cash flow. This means MPW has been burning cash on a quarterly basis, a profile that is clearly not sustainable over the long term.

So far, the company has been able to offset this operating cash burn by borrowing from its revolving credit facility with JPMorgan (JPM). This revolving credit facility only has about $200 million still left to use as of February 2024, thus, going forward, it will be more difficult for MPW to cover its cash burn and some serious liquidity constraints may emerge in the coming quarters.

At the end of 2023, its cash was about $250 million, a small increase compared to the end of 2022 ($235 million). This could suggest a stable cash position throughout the year, but as I’ve analyzed this was only possible by increasing indebtedness from the revolving credit facility. Together with its revolving credit facility, this means that MPW’s liquidity was about $450 million at the end of 2023.

While this may appear to be enough to cover upcoming debt maturities, this is not likely to be the case, given that MPW’s operating performance has been quite weak and should continue to burn cash on a quarterly basis.

Indeed, MPW’s financial performance was quite weak in 2023, as the company’s asset sales to raise cash and manage debt maturities, plus its struggling tenants, led to annual revenues of only $872 million, representing an annual decline of 43% YoY. Its profitability was also hit by impairments related to Steward, leading to a negative net income of $556 million in the year. Its Funds From Operations (FFO) were only $288 million in 2023, a decline of 69% YoY. Regarding its cash flow, the company generated $505 million from operating activities (-32% YoY), which were not enough to finance capex of about $350 million and $615 million in dividends.

This clearly shows that MPW needs urgently to raise cash, through asset sales or new loans, or it will face a liquidity shortage in the coming months.

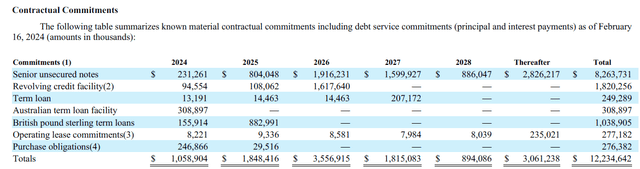

Indeed, MPW has additionally financed Steward by more than $100 million since the beginning of 2024, plus its quarterly dividend paid last January represents a cash outflow of about $75 million. This means its current cash position should have declined to about $75 million, assuming that MPW has not borrowed more from its revolving credit facility. While MPW has already some agreements that will raise about $350 million in the coming months, this is not enough to cover its more than $1 billion commitments in 2024, as shown in the next table.

Contractual commitments (MPW)

While MPW, when discussing liquidity, only talks about two maturing loans in 2024 for a total amount of $430 million, as shown in the previous table, there are much other cash outflows already committed, putting significant pressure on the company’s liquidity position.

Moreover, its refinancing needs and contractual commitments in 2025 amount to close to $1.9 billion, and some $3.6 billion in 2026. This means that MPW’s cash outflows are huge in the next couple of years, putting its business model under serious threat. Indeed, REITs need to roll over debt to maintain a sound business model, something that MPW has already shown it is not currently capable to do.

Therefore, raising cash by performing asset sales is not sustainable over the long term, thus investors should not overlook MPW’s risk of going bankrupt in the next 12-18 months, in my opinion, as the company’s liquidity position is likely to not be enough to cover its expected cash outflows.

On the other hand, if the company can raise new funds, most likely secured bank loans, this would give it some more time to potentially issue new bonds at reasonable costs. However, this largely depends on when the Fed starts to cut interest rates significantly, something that is out of the company’s control. Moreover, even if the Fed cuts by 1-2% in the coming year, this would only reduce MPW’s senior funding costs to 8-9%, which is still above its cap rates and doesn’t make much sense financially to do.

Conclusion

Medical Properties Trust operating performance has clearly deteriorated in recent quarters, and the company is doing asset sales to keep it afloat, but serious liquidity issues are likely to emerge in the coming quarters. While MPW can manage its liquidity in the short term by selling assets, this is not sustainable over the long term and huge refinancing needs in 2025 and 2026 are likely to lead the company into serious financial distress, most likely not leaving much value left for shareholders.

Read the full article here