")

Introduction & Thesis

Shares of Siga Technologies (NASDAQ:SIGA) are setting new 52-week highs, after a strong earnings report. Siga Technologies is a commercial-stage pharma company focused on health security solutions, including medical countermeasures against chemical, biological, radiological, and nuclear (“CBRN”) threats, as well as emerging infectious diseases. The post-earnings rally is also supported by a special cash dividend of $0.60, going ex-dividend on March 25. Perhaps the most important question on investors’ minds would be if it is too late to buy. This surely appears like an opportunity, given Siga’s strong positioning to benefit from the U.S. Government’s heightened focus and spending on health security subsequent to the Covid pandemic and mpox outbreaks (in 2022), as well as rising international interest in its antiviral, smallpox treatment – TPOXX (with generic name tecovirimat). A potential new long-term contract with the U.S. Strategic National Stockpile (“SNS”) could likely be a key catalyst. Let me expound on why I believe the stock could reach a target price of at least ~$10 as it expands geographically and potentially expands the indications of TPOXX to mpox and post-exposure prophylaxis (“PEP”).

Health Security Preparedness – A profound lesson imparted by the pandemic, bioterrorism concerns

The pandemic has left behind deep scars, accelerating lessons in gratitude and health security preparedness. The global market for infectious disease treatments is estimated to grow from ~$72.4 billion in 2021 to ~$106.3 billion by 2026, while the global biodefense spending reached ~$15.2 billion in 2022. Siga’s value proposition stems from its lead oral drug TPOXX, an antiviral approved by the FDA in 2018, for treating human smallpox caused by the variola virus. Smallpox is both highly contagious and lethal with a historical 30% fatality rate and an outbreak could be deadly as vaccines alone are inadequate to address the formidable threat. While there may be an argument that smallpox has been successfully eradicated globally in 1980 via relentless vaccine campaigns, its potential as a bioweapon continues to raise concerns.

How can smallpox that is wiped off the face of earth remain a bioterrorism threat?

When smallpox was eliminated completely as a disease, the U.S. and Russia publicly acknowledged holding stocks of smallpox virus for research purposes only. The outcry for destroying these last samples has been debated exhaustively. However, the destruction efforts have been stymied by concerns that rogue nations or organizations may be holding secret stashes and may attempt to create a pandemic. The Guardian exposed this possible danger in 2006 citing the lax laws governing the procurement of samples, by delving into an experiment of buying parts of the smallpox genome through mail order and publishing the story. So, the proponents for retaining the samples argued that these small, last samples can be used for developing antivirals and better vaccines, in case of a bioterrorism attack.

In the words of the WHO, “Notwithstanding the recommendations of the Advisory Committee, the Secretariat reaffirms that recalling that advances in synthetic biology and genome reconstruction technology may bring both benefits and risks for smallpox preparedness and that the risk of smallpox re-emergence continues to evolve, the distribution, handling, and synthesis of variola virus DNA continue to be governed by WHO’s recommendations to encompass these new realities.”

While it sounds like a conspiracy theory, the disturbing truth is that a well-funded terrorist organization, Ph.D. level staff and a basic lab should still be able to synthesize from scratch the DNA sequence of smallpox, which is freely available in online public databases. It can also be created by genetically modifying a similar virus-like Camelpox. This should explain why smallpox continues to remain a bioterrorism threat.

Why a smallpox vaccine alone will be inadequate to address any possible outbreak?

A smallpox outbreak could be vicious as the vaccination for the disease ended in the 1970s and most of the current population has no immunity against smallpox. The other limitation is that the vaccine should be administered within 3-5 days of infection to be effective, but the symptoms show up 2 weeks post infection.

Enter TPOXX!

FDA’s novel “Animal Rule” development pathway for TPOXX

TPOXX is the first effective antiviral therapy approved by the FDA in 2018. It works by preventing the formation of a secondary viral envelope, causing viral particles to be trapped inside the cell in which they are produced. This prevents the virus from spreading to and infecting other cells.

When TPOXX was approved, Scott Gottlieb, the FDA Commissioner at the time noted, “To address the risk of bioterrorism, Congress has taken steps to enable the development and approval of countermeasures to thwart pathogens that could be employed as weapons. Today’s approval provides an important milestone in these efforts. This new treatment affords us an additional option should smallpox ever be used as a bioweapon.”

The approval may lead to another interesting question. How can a drug be tested and approved when there is no human population to test it on, given the eradication of small pox many decades back. The FDA applied its “Animal Rule” for the assessment of TPOXX. The novel development path required that safety studies were done in healthy human volunteers, while efficacy and toxicology studies were conducted in animal models. The “Animal Rule” is used when it is not feasible or ethical to conduct efficacy trials in humans. The safety test conducted on 359 healthy human volunteers led to side effects like headache, nausea and abdominal pain.

After a Fast Track and Orphan Drug status, the FDA approved oral TPOXX in 2018 for treating smallpox. This was followed by an approval from Health Canada in 2021 for the same indication. The year 2022 was notable for Siga as oral TPOXX won approvals from the European Medicines Agency (“EMA”) and U.K.’s Medicines and Healthcare Products Regulatory Agency (“MHRA”) for treating mpox, smallpox, cowpox and vaccinia complications following vaccination against smallpox. In the same year, the FDA approved an intravenous formulation (“IV”) of TPOXX for treating smallpox.

What I like about Siga Technologies

1. Support from the U.S. Government – the stable primary customer for TPOXX.

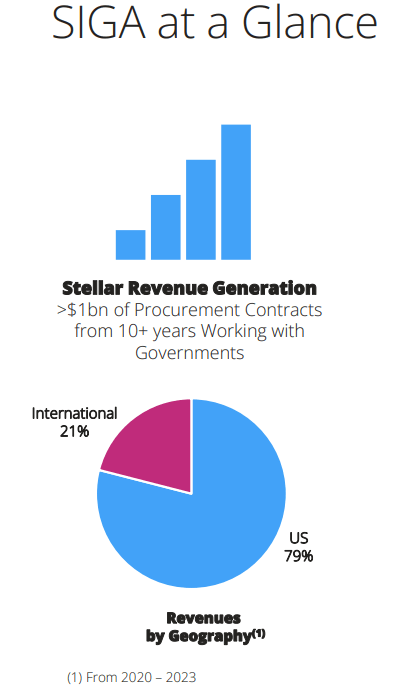

A major chunk of Siga’s revenues is derived from the U.S.

Company Investor Presentation

Since 2011, Siga has received procurement contracts for TPOXX valued at ~$1 billion from the U.S. Biomedical Advanced Research and Dev. Authority (“BARDA”). It has ~$138 million in options remaining under the latest contract in 2018. In 2023, it received a ~$11 million order from the US Department of Defense (“DOD”). The company is targeting a new contract with the Administration for Strategic Preparedness & Response (“ASPR”) for US National Stockpile (“SNS”), which could be a key catalyst.

2. Growing International Traction for TPOXX

International sales totaled ~$21 million in 2023 vs. just ~$2 million in 2020, and the company has sold $100+ million of TPOXX to more than 25 countries since 2020, including ~$28 million of European Commission orders in the past 18 months. Siga has an international promotion agreement with Meridian Medical Technologies, a Pfizer company, by which Meridian will promote the sale of oral TPOXX as a smallpox treatment in all markets, except the U.S. and South Korea. As more nations across the globe embrace stock piling and preparedness for a full range of Orthopox virus risk, the company said in its Q4 earnings call that it is experiencing lot of interest for TPOXX from multiple countries in Europe and beyond, which have ordered in the past and now indicating interest in ordering more TPOXX, often in larger quantity than the prior order.

3. Revenue and pre-tax operating income for 2023 trending above 3-year averages

Strong 2023 numbers

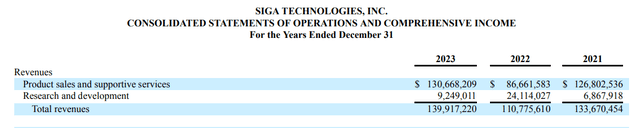

- Product Sales rose ~51% (y/y) to ~$130.7 million in 2023.

- Revenues rose to $139.9 million from $110.8 million last year.

- Net Income rose to $68.1 million or $0.95/share in 2023, from $33.9 million or $0.46/share last year.

Most of Siga’s 2023 topline was derived from Q4 revenues of ~$117 million. However, quarterly revenues are not an accurate indicator of the topline picture here, as such revenues can heavily fluctuate based on the timing of Siga’s contract deliveries. The annual revenues tend to give a more balanced picture.

Annual Revenues of SIGA (Company Press Release)

This is better explained by the guidance from Phil Gomez, CEO of SIGA, when the company reported Q2 and H1-23 results. “Importantly, revenues for the first half of 2023 represent only a small percentage of revenues expected for 2023. In the second half of 2023, the Company expects to generate approximately $113 million of revenues from deliveries of oral TPOXX to the U.S. strategic national stockpile and to generate between $30 million and $45 million of revenues from a broad cross-section of domestic and international deliveries, including deliveries of oral TPOXX to the Department of Defense, IV TPOXX to the U.S. strategic national stockpile and oral TPOXX to international customers.”

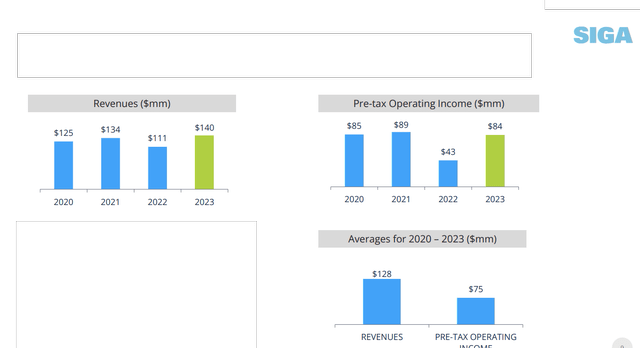

The fact that 2023 revenues and pre-tax operating income trending above 3-year averages, implies positivity.

In 2023, the company reported revenues of ~$140 million and pre-tax operating income of $84 million, beating the 2020-23 period average revenues of ~$128 million and pre-tax operating income of ~$75 million.

Company Investor Presentation

The momentum continued in the first two months of 2024, with ~$15 million of deliveries of oral TPOXX to the SNS and ~$7 million of international delivery. This equals ~$22 million, excluding a month.

4. TPOXX Label expansion opportunities in PEP, mpox

TPOXX is yet to receive FDA approval for TPOXX to treat mpox (monkeypox), although 80,000+ bottles of oral TPOXX and 13,000+ vials of IV TPOXX were distributed in the U.S. under Emergency Use Authorization during the mpox breakout. I’ve already mentioned that it has approvals from EMA and MHRA to treat mpox.

Typically, post-exposure prophylaxis (“PEP”) regimens block or reduce impact of infections in individuals with known or potential exposure to an infectious agent but are not symptomatic. Siga has been awarded a ~$27 million US–DOD contract in 2019 to support clinical studies necessary for a potential label expansion for TPOXX, including PEP of smallpox. The company believes that

TPOXX benefits patients in a prophylactic situation from the studies conducted. While the FDA has not sought any additional studies to prove the efficacy of TPOXX for PEP, it needs extended safety data in humans for a 28-day treatment regimen. The company has completed the requirement and did not find any drug-related serious adverse events, consistent with TPOXX’ existing strong safety profile. Siga plans an SNDA submission for PEP within the next 12 months.

5. Siga has no debt and cash position of $150 million at Dec 31, 2023.

6. Special dividends paid out by the company – The recent special dividend of $0.60/share represents a $0.15/share or 33% increase from the special dividend of $0.45/share in 2023. The ex-dividend date is March 25.

Revenue/EPS Forecast for 2024

BARDA may likely exercise the $138 million in remaining options under the 2018 contract. Rolling over from 2023 BARDA contracts of $15 million for oral TPOXX (already delivered in the first two months of 2024) and $15 million for IV-TPOXX (to be delivered in 2024). The $6 million deliveries to Europe remaining under the HERA (and already delivered) and $0.7 million to Canada. This is ~$175 million and assuming other international sales of at least $5 million, we can set revenue expectations for 2024 at ~$180 million. So, a new procurement contract from the SNS will be something to look forward to.

The average net income margin for the years 2021-23 is around ~44%. So, applying this to our revenue estimate of $180 million for 2024, and based on ~71 million outstanding shares, we can try and model an EPS of $1.1 for 2024.

Valuation and Rating

SIGA stock is further up since the time of submission. The stock currently trades at a ~8x forward P/E (based on my 2024 EPS estimate of $1.1). If the forward multiple reverts to its 5-year average of ~9.5x, it can lead to a price target of $10.50. Assuming a more conservative multiple of ~9x (below the 5-year average), the price target would be ~$10. If you notice on Seeking Alpha’s valuation page, SIGA currently trades at a discount to its 5-year averages on TTM Price/Sales, Price/Book, EV/EBITDA, EV/Sales valuation metrics. It is not easy to predict a price target for many years ahead based on the very limited public information available on SIGA.

Competition

In 2021, the FDA approved Tembexa (brincidofovir) to treat smallpox. I do not perceive this as a competition threat. In the event of an outbreak, the world is going to need as much help as it can get. This was pretty evident during the pandemic when many vaccines were authorized for emergency use. So, the antivirals can coexist. On a side note, the TEMBEXA U.S. Prescribing Information has a boxed warning for increased risk of mortality when used for a longer duration. Emergent BioSolutions Inc. (EBS) has exclusive worldwide rights to TEMBEXA in exchange for a ~$225 million upfront payment to Chimerix and potential milestone payments of up to ~$112.5 million (bringing the potential deal value to ~$337.5 million) plus royalties. Chimerix has a market value of ~$89 million and EBS ~$125 million. If EBS punched above its weight for the rights of TEMBEXA (by paying more than its own market value), it only substantiates the value of the smallpox antiviral, even with an increased risk of mortality boxed warning. This puts TPOXX at a higher value in the absence of such a boxed warning, strong supply chain structure and established relationships with the U.S. Govt. when the regulatory approvals for PEP and mpox come through, TPOXX will keep rising in value far above its current market value of ~$622 million.

Risks

- Customer concentration risks – A significant percentage of Siga’s future operating revenues are expected from BARDA contracts for providing to and maintaining the U.S. Government’s TPOXX stockpile. A failure to procure additional contracts will impact the business severely.

- Failure to win non-government customers could adversely impact business.

- Failure to obtain regulatory approvals for additional indications of TPOXX in PEP and mpox from the FDA could be a huge setback.

Conclusion

Siga is preparing for a dire tomorrow that I sincerely wish never comes. Nevertheless, the concerns related to bioterrorism will always be a priority for governments across the world, and global preparedness to combat these threats will likely keep moving the needle for SIGA in my opinion. The U.S Govt. procurements will continue to provide revenue visibility into the future, while the upside optionality is likely to come from approvals for PEP and mpox (U.S), as well as international expansion.

**

Cautionary Statement: The analyst/author is not a registered investment advisor and readers are asked to do their own due diligence before investing in the stock. The author/analyst is not responsible for the investment decisions made by individuals after reading this article. Readers are asked not to rely on the opinions and analysis expressed in the article and are encouraged to do their own research before investing.

Read the full article here