Since October’s surprise Hamas attack of Israel and Israel’s subsequent invasion of Gaza in retaliation, Middle East geopolitical tensions have been gradually ratcheting higher. Those tensions came to a boil this past weekend when Iran launched an unprecedented attack on Israel, sending more than 300 missiles and drones from Iranian soil. This was in response to Israel’s attack on Iran’s embassy in Damascus, Syria, earlier in the month.

Although almost all of Iran’s rockets and drones were shot down by Israeli and American forces, the attack highlights that the Middle East tinderbox could potentially be ready to spiral into a regional war on any geopolitical miscalculation by Iran, Israel, or the United States.

With so much fear and uncertainty abound, investors are naturally looking at ways to hedge their portfolios. One possible solution is to buy investment products tied to the VIX Index like the iPath Series B S&P 500 VIX Short-Term Futures ETN (BATS:VXX).

Brief Fund Overview

The iPath Series B S&P 500 VIX Short-Term Futures ETN (“VXX”) is an exchange traded note (“ETN”) issued by Barclays Bank PLC, offering investors exposure to short-term VIX futures.

The CBOE Volatility Index (“Vix Index”) is a popular measure of the market’s expectation of future volatility based on 1-month S&P 500 Index options. The VIX Index is also commonly referred to as the ‘fear gauge’, as volatility tends to spike when fear and risks are prevalent. Investors cannot invest directly in the VIX Index; instead, they must trade either VIX futures (futures contracts that bet on the level of the VIX Index at a future date) or VIX Index options.

The VXX ETN achieves its investment objective by tracking the S&P 500 VIX Short-Term Futures Index, which holds a rolling long position in the first and second month VIX futures contracts (Figure 1).

Figure 1 – VXX portfolio (ipathetn.barclays)

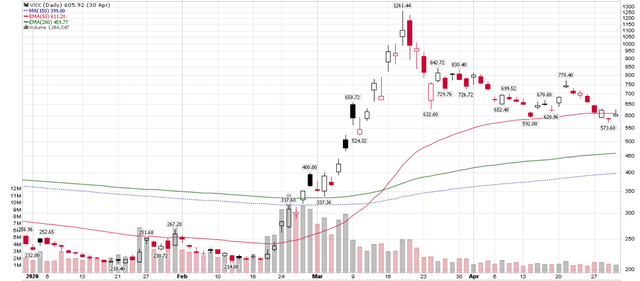

If timed correctly, holding a long position in a VIX product like the VXX can generate some eye-popping returns when tail-risk events hit the markets. For example, over the early days of COVID-19 pandemic, the VXX ETN went from a split-adjusted $215 on February 18, 2020 to an intraday high of $1260 on March 18, 2020 or a 400%+ return in a matter of weeks (Figure 2).

Figure 2 – VXX can generate eye popping returns if timed correctly (stockcharts.com)

VXX Is Not A Buy And Hold

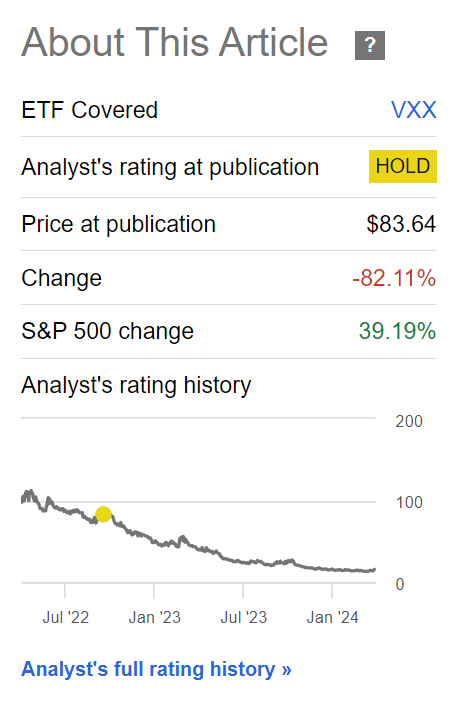

However, over the long-run, a buy-and-hold strategy in the VXX ETF is a losing proposition. For example, compared to when I last wrote about the VXX ETN in late 2022, the VXX is down an incredible 82% (Figure 3).

Figure 3 – VXX has lost 82% in value since late 2022 (Seeking Alpha)

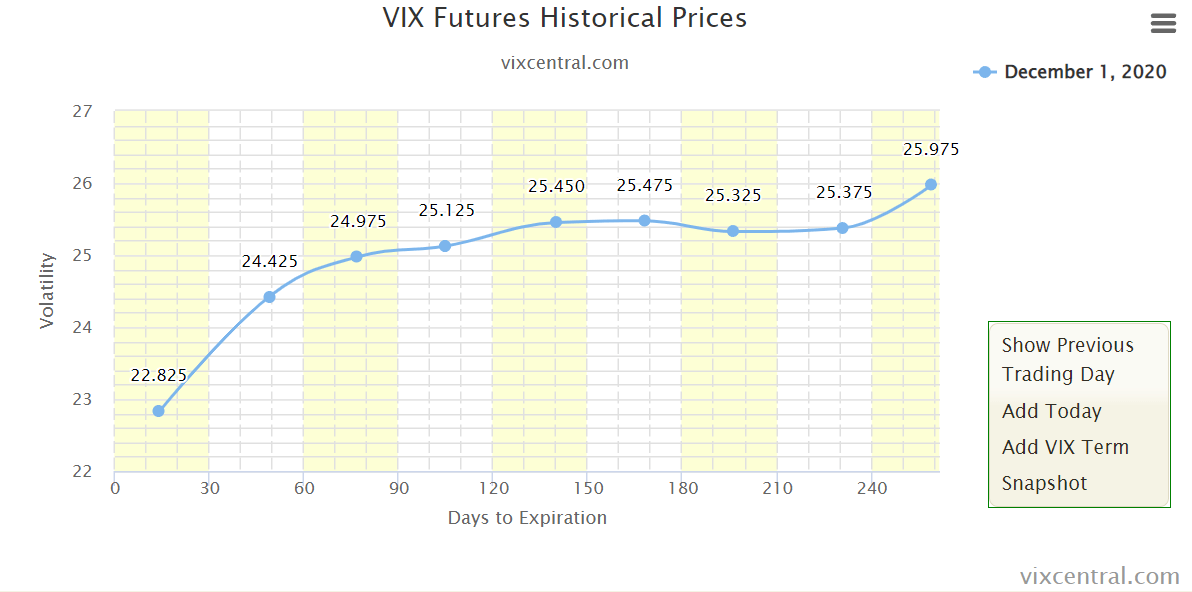

VXX’s poor long-term performance is mostly due to the structure of the product itself. Since the VXX ETN holds a rolling position in front-month VIX futures, it experiences negative roll expense each and every month in ‘normal’ environments when the VIX curve is upwards sloping (Figure 4).

Figure 4 – Illustrative VIX curve (vixcentral.com)

In other words, when the 1st month future expires, assuming no shift in overall level of volatility, the 2nd month future that VXX owned will ‘roll’ down to be the 1st month and its value will decrease. VXX will also need to buy new 2nd month futures to replace the one that rolled off.

This constant futures roll decay has caused VXX to be one of the worst destroyers of capital over the long run, with a -43.1% CAGR return since inception (Figure 5).

Figure 5 – VXX has terrible long-term performance (ipathetn.barclays)

Whatever investors decide to do, they must not hold the VXX ETN for any extended period of time.

Middle East Tension Could Reignite Inflation Worries

As we mentioned at the beginning of this article, worsening geopolitical tensions in the Middle East is a cause for concern for many investors. Not only does a direct conflict between Israel and Iran risk dragging the United States and Israel’s Western allies into yet another costly regional war, it could also reignite inflation worries, which are already simmering in the background in many Western countries.

Oil Is The First Casualty

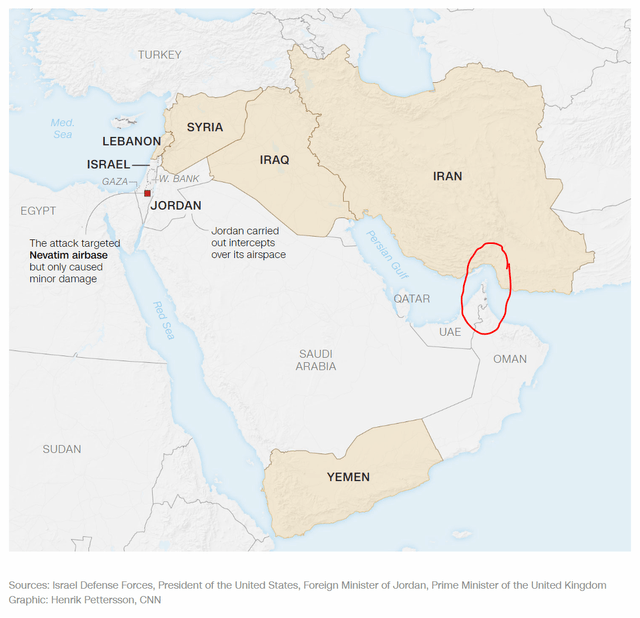

It is not hard to imagine additional sanctions being placed on Iran as a result of its latest attacks which could restrict its oil output and cause energy prices to increase ahead of a crucial U.S. election season. Furthermore, a belligerent Iran may decide to shut the Strait of Hormuz and disrupt the global crude oil trade. As a reminder, approximately 25% of the world’s oil transits through the Strait of Hormuz (Figure 6).

Figure 6 – Strait of Hormuz is crucial to oil trade (CNN)

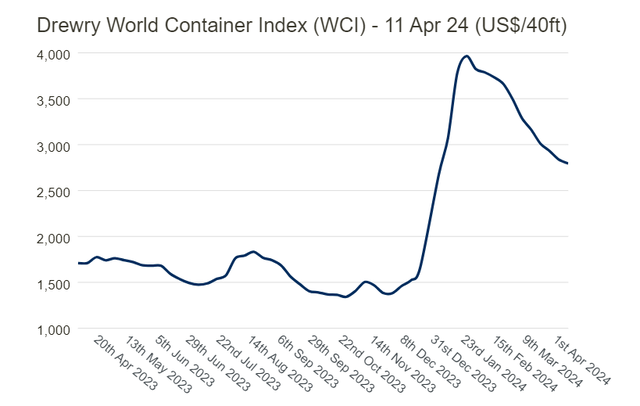

Shipping Rates Set To Surge

Furthermore, with Iran commandeering an Israeli-containership, likely as part of its retaliation against Israel in my view, shipping rates are set to surge higher, inflicting further goods inflation and supply-chain disruptions.

Already, container shipping rates have risen in 2024 as Houthi-rebel attacks in the Red Sea have caused Asian containerships to divert away from the Suez Canal and take a much longer route around South Africa to reach Europe (Figure 7). I believe with Israel and Iran possibly on the brink of an all-out war, shipping rates will likely rise even higher.

Figure 7 – Shipping rates are set to surge higher (drewry.co.uk)

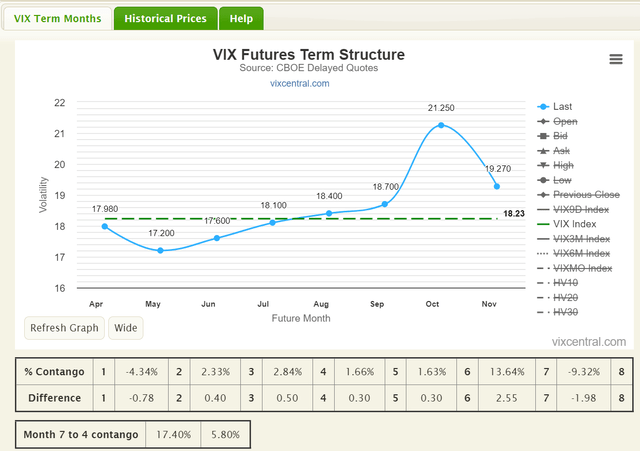

VIX Traders Appear Worried

As we mentioned above, in normal times, the VIX curve is upwards sloping, as traders generally have a good sense of short-term risks. However, in recent days, we have seen an inversion of the VIX curve, with spot VIX levels of 18.2 being higher than April futures at 18.0 and May futures at 17.2 (Figure 8).

Figure 8 – VIX futures curve inverted (vixcentral.com)

My interpretation of the inverted VIX curve is that traders are worried about near-term geopolitical risks. As a result of the VIX curve inversion, the VXX ETN actually gains value during the futures roll, as its expiring April futures are priced higher than the June futures that it must roll to.

Downside Risks To VXX

Although tensions are high, there are reasons to be hopeful that the latest spat between Israel and Iran will not morph into an all-out war. First, Iran’s attack was well-telegraphed, with the United States and other Western countries warning their citizens ahead of time about an imminent attack. This likely allowed American and Israeli forces to prepare for the barrage of missiles and drones, limiting casualties and damage.

Furthermore, before the missiles even landed, Iran had already sent a letter to the United Nations stating that it considered its retaliation operation concluded. My interpretation is that Iran only half-heartedly launched its attack to save face and does not wish to escalate the situation.

Finally, although the United States helped defend Israel against the Iranian attack, the U.S. is also counselling restraint to Israel. In fact, President Biden’s message to Israel is to ‘take the win’ given that Israel was largely unscathed from the attacks.

If the Iran/Israel situation is able to de-escalate, then we should naturally see the VIX curve re-steepen. VIX levels should also decline, which would be detrimental to the VXX ETN.

Conclusion

A potential direct conflict between Israel and Iran risks starting a regional war that can cause oil and VIX to spike. Investors may want to hedge their portfolios with a small allocation to short-term volatility products like the VXX ETN.

I am upgrading the VXX ETN to a speculative short-term buy as a portfolio hedge.

Read the full article here