As an investor, one of the things you don’t want is for your company to do a major announcement via an SEC filing without a press release. Generally, no good comes out of these. We saw one on the Good Friday holiday from First Republic Bank (NYSE:FRC.PK) and it contained news that likely made investors worried.

On April 6, 2023, and as a measure of prudent oversight, the Board of Directors (“Board”) determined to suspend payment of the quarterly cash dividend on each series of the Bank’s outstanding noncumulative perpetual preferred stock set forth below (the “Preferred Stock”). Under the terms of each series of Preferred Stock, the right of holders to receive dividends is noncumulative, and the Board is not required to declare a dividend payable in respect of any dividend period.

Source: FRC April 7, 2023 SEC Filing

The Impact

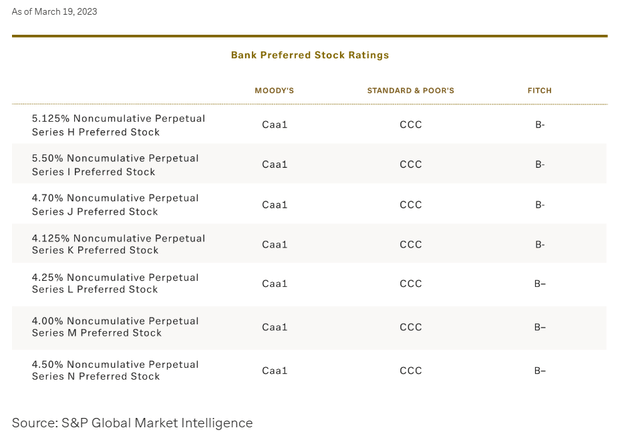

FRC has 7 different preferred shares listed and they could get a jolt on Monday morning.

1) First Republic Bank DEP SHS RP PFD H (NYSE:NYSE:FRC.PH)

2) First Republic Bank 5.5% NON CUM PERP REP SER I (NYSE:NYSE:FRC.PI)

3) First Republic Bank 4.7% DEP RP PF J (BOIN:BOIN:FRC.PJ)

4) First Republic Bank 4.125% DEP PFD K (NYSE:NYSE:FRC.PK)

5) First Republic Bank 4.25% DEP PFD L (NYSE:NYSE:FRC.PL)

6) First Republic Bank 4% DEP PFD M (NYSE:NYSE:FRC.PM)

7) First Republic Bank DEP SHS REP 1/40TH PERP PFD (NYSE:NYSE:FRC.PN)

On our last coverage we highlighted why these were quite risky.

Our take on these is that they are a reasonable viability play, but investors need to keep in mind that par value of these preferred shares is very close to the market value of the common equity. We generally are hesitant to jump into preferred shares when the equity thickness protecting them is weak. So while there are scenarios where preferreds can do better (a brokered marriage with a larger bank), they are almost as risky as the common shares.

Source: Common Shares Remain A Relatively Poor Choice

The dividend suspension comes as no surprise here. In fact, even the rating agencies gave you a big hint.

FRC

While we did not get liquidity data from FRC specifically, and that is of course bad, there has been a lot of other data out and all of that plays into what will happen to FRC over the next few months. Let’s look at that data.

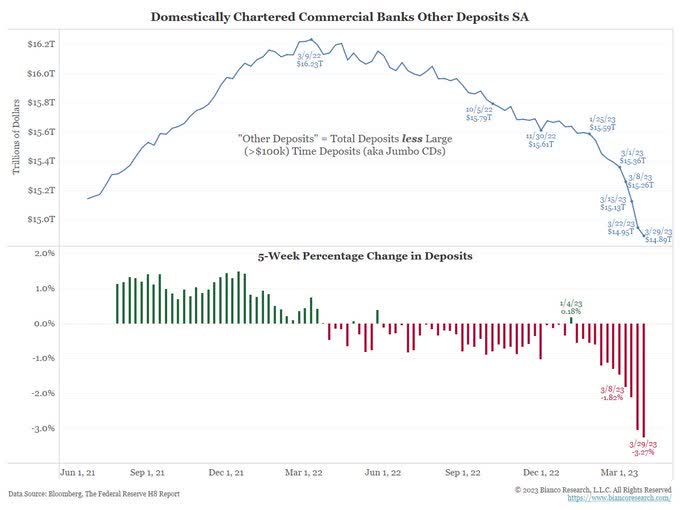

Deposits Dive

So far the deposit run (we don’t want to start a panic by calling it a bank run) has shown zero signs of abating. The latest data confirmed this.

Jim Bianco-Twitter

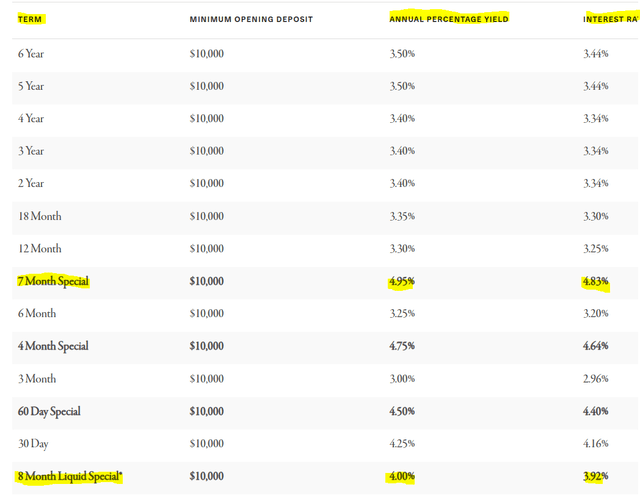

This is interesting as the last two weeks have seen many banks (not all, but many), wake up to the possibility that paying 0% in an era of 5% is a recipe of disaster. Nonetheless, these banks are doing so slowly and trying to protect profitability vs trying to stabilize deposits for as long as possible. This is backfiring and unless dramatic steps are taken soon, we may have a more systemic problem. You have to know that the C-suite has only two known modes. Mind numbing complacency or utter panic. Once they move into the latter mode you can expect a very sudden and very large boost to interest rates. FRC will be at the forefront of this as large banking clients have the additional incentive of wanting to move out of what might be a difficult situation for them. So far FRC has bumped up the CD rates and is trying to incentivize clients for a 7 month lock.

FRC

The 8 months “Liquid Special” CD allows partial withdrawals.

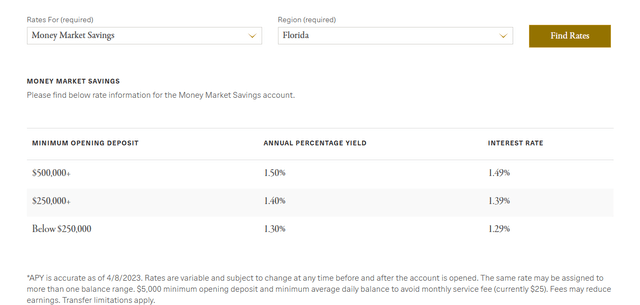

That might stem some of the flow but the bigger bleed will be in areas where investors want high rates and mobility. Here, FRC is not offering much and we think they need this to be bumped up well above 3.5%.

FRC

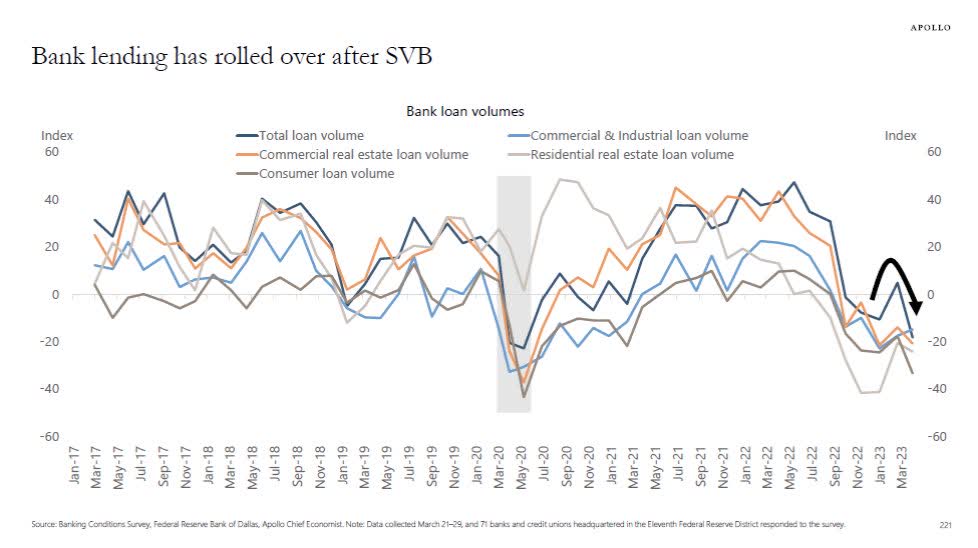

Lending Dives

The other piece of data we got was that bank lending was falling as well.

Apollo-Twitter

This comes from two factors. The first being that banks are trying to protect their assets to liabilities ratio from getting worse as they face depositors exiting. The second is of course that every bank has multiple economists and all of them know that you don’t mess with an inverted yield curve. A recession is not too far away and whatever you are pricing those loans at, it is not worth it at this point.

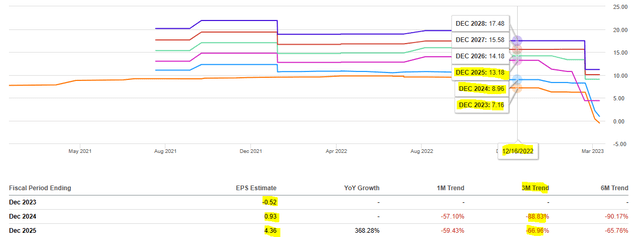

The same plays out for FRC as well. FRC’s lending will be far more curtailed than even regular banks as its deposit flight has been unprecedented. Analysts are still grappling with the impact on this leveraged structure and estimates are all over the place.

Seeking Alpha FRC

What is key though is rate of change in the estimates. For the year ending December 31, 2023, analysts expected $7.18 per share of profits not too long ago.

Seeking Alpha-FRC

The average is now for a modest loss. 2024 numbers have fared just as bad, dropping almost 90% in the last 3 months. Our larger point here is the same one we made with The Charles Schwab Corporation (SCHW). Don’t confuse survival for profitability. Don’t confuse you not losing everything with you making back your losses.

Verdict

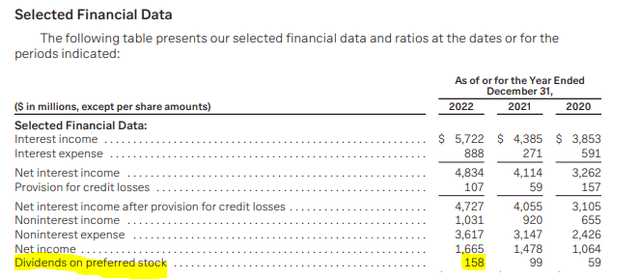

The preferred share dividend suspension saves some cash.

FRC-10-K

But it is a drop in the bucket relative to the flight outflow that we have seen. Ideally they should have suspended this alongside the common dividends out of prudence. Making this a separate announcement, specially in a press release lacking details of the capital situation today, risks making the panic worse. We still think that FRC makes it ultimately. As explained in our previous article, we believe the common shares offer a poor risk-reward. So far, even the preferred shares have not been very appealing but perhaps after this news, they may give the perfect asymmetrical return profile. We are watching them for now and might dive in for a small speculative position, if we see utter chaos.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here