Author’s note: Funds are in USD unless marked with C$ for Canadian currency.

Investment Thesis

Debt-free Parex Resources (TSX:PXT:CA) announced a 50% increase to it quarterly base dividend in February 2023. The company has committed to returning at least one third of FFO and 100% of FFF to shareholders. In addition to dividend growth, the company has reduced its share count by over one third since 2017 through share repurchases. Following a year of record production, Parex expects another 14% boost to oil output in 2023.

Parex operates in Colombia where it is subject to geopolitical risks that can have an impact on production. Parex navigates number of above ground operating risks in South America, including a left-leaning national government and guerrilla violence. Parex is a high-quality play on a niche oil opportunity to consider including in the higher risk/higher reward segment of your portfolio.

Company Profile

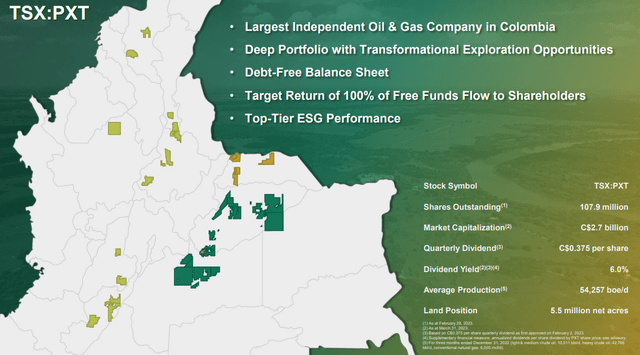

Parex Resources was formed in 2009 out of a spin-off from Petro Andina Resources, a Calgary based exploration and production company operating in South America. Twelve years following the company’s 2011 IPO on the Toronto Stock Exchange, Parex is the largest independent oil and gas company operating in Colombia.

Parex has two main operating areas across the Llanos and Magdalena basins respectively and one non-operated base production area in Llanos called LLA-34, which accounts for the majority of production. The company has 5.5M acres with 1P and 2P reserves of 131 and 201 MMboe respectively. Parex is headquartered in Calgary Canada, with an operating office in Bogota, Colombia. The company has a market capitalization of C$2.8B with average daily volume of 747,000 shares.

One of Parex’s key strategies to add value to its Colombian production is to apply proven technologies from other extraction jurisdictions to its Colombian assets. The company has identified opportunities to pursue horizontal and multilateral drilling, advanced stimulation, and the application of synthetic drilling fluids to boost production. Parex has sounded its intention to put the “E” in E&P with a significant focus on drilling and exploration in its near term capital pan.

Parex Operations Map (Parex Resources)

Colombian Oil Industry

Columbia ranks 60th in the global Economic Freedom index and a similar 67th in the global Ease of Doing Business Index. Both these indicators suggest Columbia is a medium-risk business environment. While Columbia has stable elections and a functioning central government, the country’s property rights are not consistently enforced and often do not include mineral rights.

Parex Office, Bogota (Parex)

Colombia produces approximately 756,400 bbl/day of petroleum making it the 21st largest producer in the world, just behind the UK and ahead of Venezuela and Egypt. The country has proven crude oil reserves of 2.036 billion barrels as of 2021, making it one of the top 40 national reserves globally. Colombia has a well-developed oil infrastructure system with over 6,000 kilometres of crude and liquids pipelines that move crude from the main production basins of Llanos and the Magdalenas to an export terminal at Coveñas on the Caribbean coast.

In January, Colombia’s leftwing government announced that it will not approve any new oil and gas exploration projects, award any new hydrocarbon contracts and will ban fracking. The country’s new leftist President and former guerilla, Gustavo Petro is planning to steer the country towards renewable energy. Despite this commitment and the 15-year transition window identified, the oil and gas industry remains very important to Colombia. According to S&P Global (SPGI), the oil industry in Colombia represents 12% of national earnings, 34% of foreign investment into the Colombian economy, and 56% of all exports. The oil industry employs some 600,000 direct and indirect workers and accounts for 3-4% of GDP.

The 88% state-owned Ecopetrol S.A. (EC) is the country’s largest producer with production averaging approximately 700,000 bbl/day in 2021. These oil revenues are used in part to fund fuel subsidies for the Colombian population. In 2005, Colombia moved away from having Ecopetrol contract individually with foreign operators and moved E&P activity under the state run agency Agencia Nacional de Hidrocarburos or “ANH”. ANH enters into exploration and exploitation contracts that provide full risk/reward benefits for the contractor. Companies including Parex and 118 other operating firms retain the rights to all reserves, production and income from any new exploration block (subject royalty and income tax).

Taxation Environment

As of January 1, 2023, Colombia introduced new tax reforms that includes a base income tax rate of 35%. The measure also introduces a surtax of between of 0% to 15% for Colombian oil production linked to the historical Brent oil price over a 10-year period. An internal corporate restructuring to consolidate Llanos play assets into one corporate entity is expected to deliver a $325M boost to the Parex’s deferred tax asset balance. This maneuver helps mitigate the impact of the tax increase from 2023 through 2027. For 2022, Parex reported an effective tax rate of approximately 23%. For 2023, assuming similar Brent pricing, the company anticipates an effective tax rate in the range of 23% to 27%.

Safety Concerns

Following the success of the FARC peace treaty signed in 2016, the Colombian government announced planned peace negotiations with the Ejército de Liberación Nacional (“ELN”) in 2022. However at this time, no agreement has been reached with the ELN. On its Q1 2023 earnings call, Parex discussed voluntary shut-ins at its Capachos and Arauca blocks due to safety concerns regarding ELN activity in the area. Parex has been working on the Capachos block near the Venezuela border since 2017. This shut-in has exceeded the 20 day suspension of work in 2018 when similar safety concerns were noted. With the ELN presence more concentrated near the Arauca Block, the Capachos site is likely to be back in service first, however there is no estimate of timeline. These concerns are likely to impact Q1 volumes, however Management does not expect a material impact on full-year guidance.

2023 Guidance

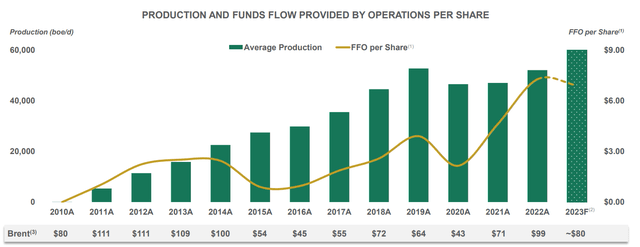

2022 full year production averaged 52,000 bbl/d, a 23% year-over-year increase per share. In 2022, Parex generated record FFO of $725M, a 26% jump from 2021. The company anticipated FFO of $705–780M with FFF increasing to $295 million in 2023. Over the next 3 years, Parex anticipates 5% annual growth on current production assets that would ramp up output from 60,000 bbl/d in 2023 to 67,000 bbl/d in 2025. This is to be driven by capital guidance of $425M-$475M for 2023. Over the next three years, capital drops $450M in 2023 to $375M in 2024 and $325M 2025. All in, Parex is guiding a 14% year over year production increase for 2023 that considers the 5% production growth on current assets and the balance coming from new capital and exploration. At US$80/bbl Brent, the company has provided cumulative FFF guidance of approximately $1B.

Parex Production Growth (Parex Resources)

Capital and Exploration

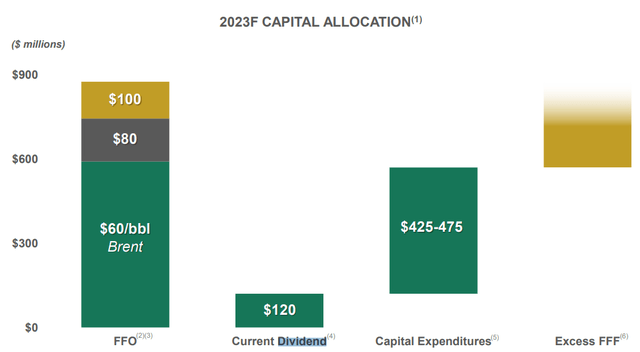

Parex’s full capital program for 2023 is $425-475M, 18% lower than 2022 capex. Despite the more modest expenditure, the company anticipates the majority of YoY production growth coming from exploration. The company “Big E” plans include drilling 65 gross wells with 10-15% of annual capital “’at risk” to pursue exploration growth in Arauca, Llanos, VIM-43, Magdalena, and LLA-122 in the Llanos Foothills. In addition to its plans to spud wells in the first half of 2023, Parex is also pursuing a natural gas play that has been excluded from Colombia’s new tax reform policy. Beyond its aggressive exploration program, the company has noted that maintenance capital demands should drop off over the next few years as efforts to mitigate the base decline rate on current production take effect. Less emphasis on maintenance capital should allow for a greater focus on exploration and development in coming years.

Parex Capital Allocation (Parex Resources)

Dividend Growth

Parex initiated its dividend program in September 2021 with a quarterly dividend of C$0.125 and has increased it three times since. For Q1 2023, Parex declared a dividend of C$0.375 per share, a 50% increase over the Q4 2022 dividend of C$0.25. With annual dividend payout of C$1.5, Parex has a forward yield of 5.7% at current levels. Despite Parex reiterating its commitment to return at least one third of FFO and 100% of FFF to shareholders, the company’s payout ratio is just 16%. While Parex’s board approved a special cash dividend in the amount of C$0.25 in 2021, the company’s most recent guidance suggests that it will focus on the sustainability of its regular dividend and return the balance of free cash flow to shareholders through share buybacks. According to Chief Financial Officer Ken Pinsky:

The focus is on the regular dividend with the buyback then making up the rest of our free cash flow target of returning back to the shareholder, 100% of our free cash flow. And so at — commodity prices at $80 and above, we look to be able to do a full 10% buyback as well as pay that $0.375 dividend, which is up from $0.25 in the previous quarter.

Returning Capital

Parex has been able to grow it dividend through a combination of lower share count and higher cash flow. In 2022, Parex returned approximately 36% of adjusted FFO to shareholders through dividends and share repurchases. With $220M allocated in 2022, Parex fully exhausted its previous NCIB of 11,820,533 common shares at a weighted-average price of $20.68 share. This marks the company’s fourth consecutive full course of NCIB, which has seen the company reduce its share float by approximately 33% since 2017.

In January 2023, the Toronto Stock Exchange approved Parex for a new NCIB that permits the company to purchase for cancellation up to a maximum of 10,675,555 shares, representing 10% of the public float. Parex expects that at $80/bbl Brent pricing, it will be able to fully exhaust its 2023 NCIB.

Risk Analysis

Beyond the obvious commodity price and geopolitical risks inherent to operating a 100% oil-weighted venture in Colombia, there are a number of other considerations for investors of Parex. While the company has good assets in Colombia and there still appears to be meat on the bone within the company’s near term exploration and production portfolio, Colombia has continued to signal its shift away from fossil fuels. The recent ban on fracking and new hydrocarbon contracts, as well as the prospect of higher effective taxes are all signs of a less favourable regulatory environment for oil and gas operators.

The country has seen a secular decline in production from its peak over 1,00,000 bbl/d in 2015 to 760,000 bbl/d in 2021. This production decline is mirrored by a drop in hydrocarbon investment. Stripping out any violence or safety concerns, Colombia is a less attractive operating jurisdiction than it was even a few years ago.

With a net cash position of $72M, Parex does not require any debt to finance its operation. The company has an untouched credit facility of $200M should it require cash flow support. In addition to being debt free, the company has bought back over one third of its equity over the past six years. This balance sheet strength is reflected with a 2022 P/CF ratio of 3.4X and 2.4X EV/DACF. Parex’s valuation is in line with Gran Tierra Energy (GTE) at 23E EV/DACF of 3.0X and 3.1X respectively. Gran Tierra is the other large Canadian E&P firm with Colombian operations. Both these valuations compare favourably to the North American Intermediate Exploration & Production average of 3.9X 23E EV/DACF.

Investor Takeaways

Parex is a quality name to include in the higher risk/higher reward segment of your portfolio. Oil and Gas E&P can be a difficult business in the best jurisdictions, the above ground operating and regulatory environment in Colombia adds a material risk dynamic. However, the company’s pristine balance sheet and strong free cash flow mitigate the company’s total risk.

Parex’s above-average risk rating does not detract from the real opportunity that the company is exploiting in Colombia. Guidance for 14% YoY production growth, a recent 50% dividend boost, 10% share buyback program and a strong exploration program are all catalysts for a strong total return opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here