Co-produced with Philip Mause.

It is never pleasant to contemplate or plan for one’s demise, but part and parcel of retirement planning is determining whether and to what extent to plan to convey assets to heirs. There is enormous variation – especially of late – in family structure as well as the sense of obligation various family members feel for one another. Bearing this variation in mind and conceding that generalizations do not apply in many instances, we can still discuss certain types of situations and their investment implications. In thinking through the impact of these considerations about investment strategy, it probably makes sense at the outset to distinguish provisions for spouses (and other close dependents) from provisions for others.

A general rule that applies throughout this analysis is that certain investment strategies necessarily tend to produce a higher residue of assets at death than others. For an extreme example, selling one’s home and all other assets and using the money to fund a simple single-life annuity will result in producing an estate of near zero value. Of course, there are almost limitless variations in annuities and some of them do produce a residue – in many cases, depending upon the time of death. But, as a general rule, annuities and annuity-like schemes tend to diminish what remains to leave behind.

Spouse

In many, although not all, instances, people think in terms of a family unit or a “household” which includes spouses and children. Typically the children become economically independent as the parents age into retirement and so the retired “household” transitions to consist of a husband and a wife (or more generally, two partners). In some cases, assets are pooled and in others, they can be kept separate. At any rate, we will deal with the situation in which each partner feels a deep sense of obligation to the other and in which retirement planning involves planning to have sufficient resources for BOTH partners until they are both deceased.

This immediately has the effect of extending the expected period of retirement as well as creating an increased probability of a very long period in which expenditures have to be made. In many cases, the male partner is older than his wife and this, together with greater female longevity, creates the likelihood of there being an extended period of time during which the widow must carry on after the husband’s death. Given this potential, it would be irresponsible for a husband who feels a strong obligation to his wife to take all of their assets and buy a single life simple annuity based on his own life. It is pretty easy to see that this would create a serious potential – indeed, a strong probability – of leaving his widow in penury.

Although it is easy to see the folly of the above strategy, spousal obligations have many other investment implications. If the life expectancy of the husband is 8 more years but the wife is considerably younger, it is entirely possible that she will live for 20-25 more years. Planning for 25 years involves taking account of the potential for serious inflation, changes in tax laws, and market disruptions. If the husband is “running” the investments, there is a danger that he will subconsciously start planning for 8 years rather than 25.

Planning for a longer period that has to be funded almost necessarily requires that one try to accumulate at least a significant share of assets that have the potential to appreciate in value – or alternatively set aside some of the yields on assets to increase the corpus that is invested. Again, there are situations in which the “nest egg” is large enough to produce an enormous yield on fixed-income investments that will likely cover virtually any projected situation. But absent this massive amount of retirement savings, consideration has to be given to planning for asset appreciation.

As a result, if a long period must be covered for the combined expected longevities of a couple, in many cases it is virtually essential for there to be a significant equity component. As noted above, annuities generally vanish at death and a combined annuity for husband and wife may require a very large initial payment to generate decent cash flow. In addition, unless it adjusts with inflation, there is a danger that as time passes the “real” (inflation-adjusted) value of the periodic payments will decline considerably.

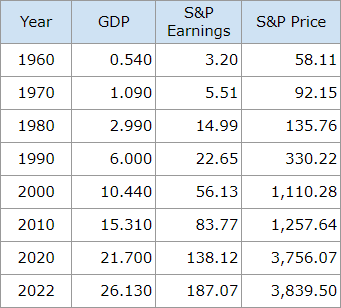

One might consider a portfolio consisting entirely of fixed-income investments, but again, there is a real danger that over a long period of time both the face value and the yield will decline considerably in real terms. On the other hand, equities have tended to increase in nominal value over time partially due to real economic growth and partially due to inflation. The table below provides nominal GDP (in trillions of dollars), nominal corporate earnings, and S&P 500 prices at 10-year intervals since 1960. Earnings for 2022 are for the 12 months ending September 30, 2022.

Data Source: WSJ

It has certainly not been a straight line up for the Index. But over 10 and – even more so – 20-year periods of time the trend is pretty unmistakably upward. This has, of course, been reinforced somewhat by inflation, as the pattern since the end of WW2 has been inflationary – and now with a “target” which assumes some inflation, and also the reality that when the target is missed, it results in even higher long-term inflation. There has also been a fairly consistent but sometimes disappointingly slow pattern of “real” (after inflation) growth in the economy. All of this produces higher nominal GDP. As corporate earnings are generally viewed as a function of GDP, it also produces higher nominal corporate earnings. While the price-earnings ratio for stocks varies enormously over time, the pattern of higher nominal corporate earnings ultimately leads to higher nominal stock prices. It is clear that if you are planning for a long period of time – as you often have to in order to protect the interests of a younger spouse with greater projected longevity or to leave bequests behind – equities have important advantages.

Everyone Else

Once again, there is enormous variation in the concern that retirees have for leaving assets behind to individuals and entities other than spouses. In some cases, there are dependent children. There may be brothers, sisters, nieces, nephews, and others who have needs. In other cases, there is an interest in funding the education of grandchildren. Many retirees feel a strong interest in leaving behind a bequest to a university or charitable institution.

Planning for this requires trying to anticipate what will be left behind after the demise of the longer-lived member of a spousal pair. Once again, annuities typically do not provide for such a residue. Fixed income investments also may decline in real value – or require (as the real value of yield declines) the “invasion of principle” to provide sufficient cash flow. Once again, equities provide an attractive path to the realization of objectives in this direction.

The Advantages of the Income Method

When properly implemented, the Income Method can provide the retiree with a strategy to cover the needs of a spouse as well as leave behind a residue even after a relatively long period of combined retirement. A properly structured portfolio can produce considerable appreciation as well as gradually increasing yield over time. Many of the stocks, ETFs, and closed-end funds in the HDO portfolio include entities that should grow with the economy and keep up with inflation. In addition, HDO often is able to recommend fixed-income securities which have the potential to appreciate in value, and subscribers can buy them and take advantage of both high yield and some appreciation.

At High Dividend Opportunities, our model portfolio currently yields +9%, with exposure to dividend stocks, and lower-risk preferred stocks and baby bonds. Some examples of our stocks that have the potential to keep growing are: Tekla Healthcare Investors (HQH) – yield 9.1% – offering exposure to the important and growing healthcare sector, W. P. Carey (WPC) – yield 6% – a well-managed equity REIT, and Antero Midstream (AM) – yield 8.5% – an energy position which is focused on natural gas which has enormous growth potential both in the U.S. and worldwide.

Read the full article here