")

Thesis

American States Water Company (NYSE:AWR) has delivered strong dividend growth in the past years as compared to its competitors in the market. The company topline has benefited from new rate increases in the recent year and should continue to benefit in the coming years with new rate case increases, for new rates in years 2025 through 2027. The company’s Contract services segment is also showing strength due to new contracts with the U.S. government and is also well-positioned to win projects further, which should drive the company’s operating revenue in the longer term.

While the company’s bottom line continues to grow quarter on quarter, the stock valuation is still more than 50% higher than its sector median, which makes this stock an unattractive investment option at the current price point. Therefore, despite a favorable long-term outlook, I have a hold rating on this stock.

Business Overview

American States Water Company is a utility company based in America. The company provides services related to water and electricity to residential, industrial, and commercial customers in the United States. The company purchases produces, and sells or distributes water and electricity to its customers in the region. The company operates under three reportable segments:

-

Water: This segment is the largest component of the company’s operations. The segment involves the sourcing, treatment, and distribution of water to residential, industrial, and commercial customers, and is mainly represented by Golden State Water Company (GSWC).

-

Electric: Relatively, the smallest business with about 8% of total revenue as of year-end 2023, the segment provides electric services in certain regions.

-

Contracted Services: This segment involves contracted services to various agencies related to water and wastewater systems through its subsidiary, American States Utility Services (ASUS).

Last quarter performance

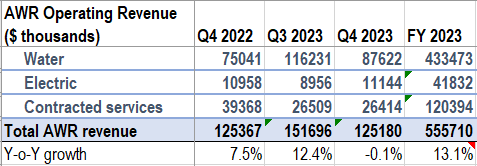

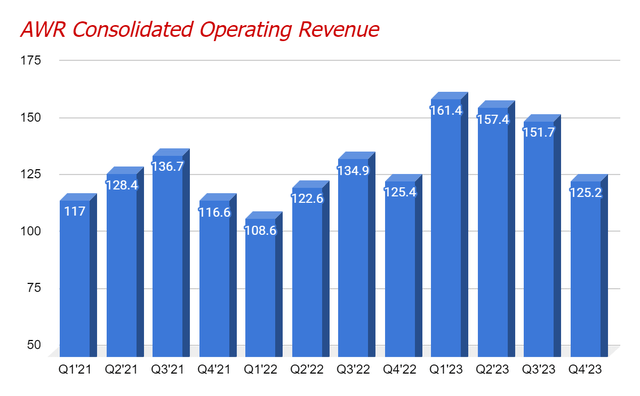

The company’s topline has grown in strong double-digit throughout 2023, however, turned almost flat as the company exited 2023. The company reported a decline of 0.1% in its consolidated revenue to $125.18 million in the last quarter of 2023 as compared to the prior-year quarter.

AWR segment revenue (Research wise) Consolidated revenue (Research Wise)

The flat topline growth was primarily due to the negative impact of the significant decline in the company’s ASUS business of the Contracted Service segment, primarily due to the impact of timing differences in executing construction projects, which fully offsets the growth across the Water and the Electric segment during the last quarter of 2023.

The Water segment was the strongest during the last quarter as it grew in the high teens or by $12.6 million during the quarter as compared to Q4’22. This growth was mainly due to the benefit from rate increases for 2023, which more than offset the negative impact of lower revenue resulting from the cost of the capital decision in July 2023.

The Electric segment’s revenue on the other hand remained flat as compared to the prior year’s quarter due to pending approval for new rates for 2023. And, the Contracted Service revenue, as we discussed, decreased approximately by $13 million versus the prior year quarter. For the full year 2023, the company’s top line grew 13.1% versus the prior-year quarter, due to robust growth in the first half of the year, which more than offset the impact of a relatively weaker second half.

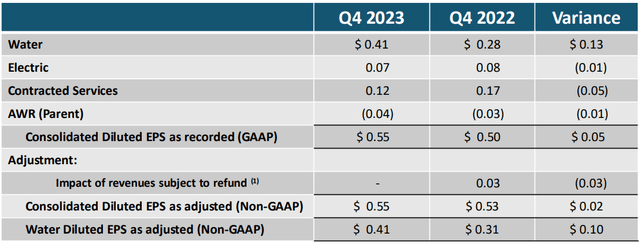

While the company’s topline remained flat during the quarter, the company’s consolidated operating margin experienced a notable increase of 590 bps to 27.9% versus 22% in the prior-year quarter. This margin expansion was mainly driven by the benefit from the rate increase in the Water segment and $9.3 million lower operating expenses largely related to reduced construction costs at ASUS during the quarter. The company’s strong margin growth, particularly in the Water segment benefited the company’s bottom line as well, as the company’s adjusted EPS increased to $0.55 in the last quarter of 2023, beating the Consensus estimates by $0.02.

AWR’s segment wise EPS distribution (AWR Q4’23 presentation)

Outlook

The topline growth of utility companies like AWR is mainly dependent upon regulatory approval on the rate increase, which is generally in line with the recovery of the company’s rising cost and earning a reasonable return on their investments. This key factor has so far benefitted the company’s operating revenue in 2023, as the final decision in the general rate case proceedings set new water rates for the year 2023-2024, which drives the company’s revenue. In addition to this, the company has also filed a general rate case in August 2023 with the California Public Utility Commission (CPUC) to set new rates for the years 2025 through 2027, which should further benefit the company’s operating revenue in the years ahead.

ASUS, the company’s contracted services subsidiary, was awarded a new 15-year contract apart from the existing 50-year contract, in 2023 by the U.S. government to maintain, operate, and provide construction management services for the water distribution, and wastewater collection and treatment facilities at Join base code (JBC) located in Massachusetts, which should fuel the company’s Contract service business of the company in the future.

Additionally, ASUS continues to pursue new construction work on the military base it serves as it gets new awards worth $20.4 million in new construction projects for completion in 2023. Also, this project was in addition to $34.4 million awarded last year for projects to be completed in 2025. These projects should further benefit the company’s top line in the coming years. The company also has strong relations with the U.S. government due to their confidence in AWR’s expertise in managing water and wastewater systems on military bases, which, in my opinion, well positions the company to compete for new contracts in the future.

When it comes to a utility company, apart from the rate increase approvals by the regulatory, another key factor that derives the company’s topline growth is stability in its customer base. In the case of AWR, the company’s GSWC and BVES subsidiaries have a stable customer base with about 90% of its revenue derived from residential and commercial customers. Additionally, to maintain this strong and stable customer base, AWR continues to work on improving operational efficiencies, so that they can reduce the cost to customers while providing outstanding services. Furthermore, the company is also focusing on expanding its customer base in the future through organic as well as acquisition.

Finally, AWR is focusing on growing the regulated utility business through the necessary infrastructure replacement and the company’s regulated utilities have also invested a record $175 million in 2023 and now targeting 2024 capital expenditure to be in the range of $160 to $200 million, which should be beneficial for the company’s topline growth in the coming years. Overall, I am optimistic regarding the company’s long-term prospects due to its strong customer base, upcoming rate increase, and strength in the company’s contract services business.

Dividend growth

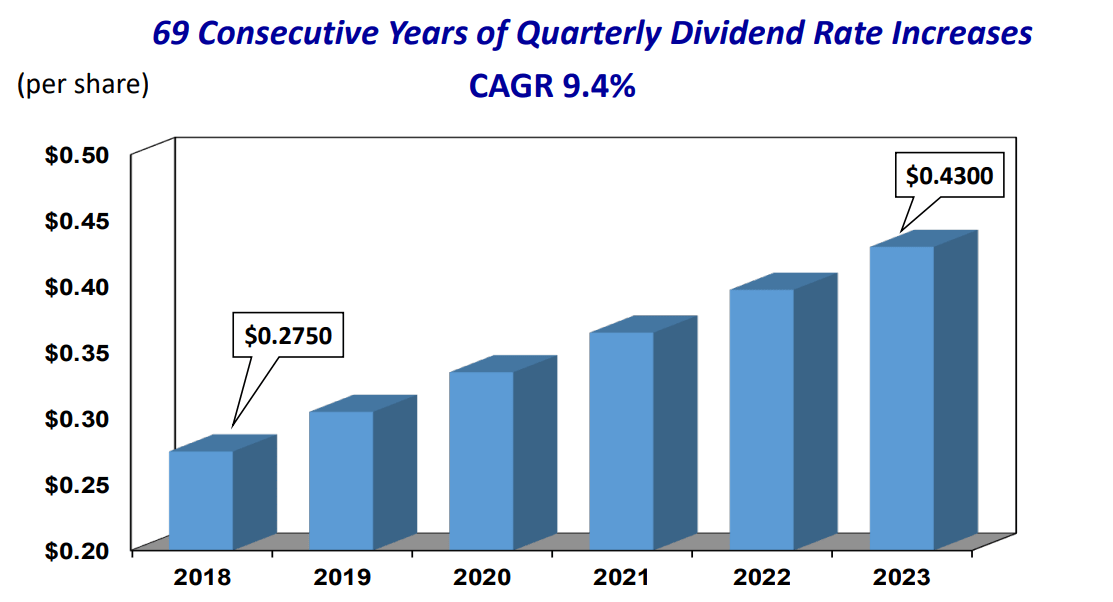

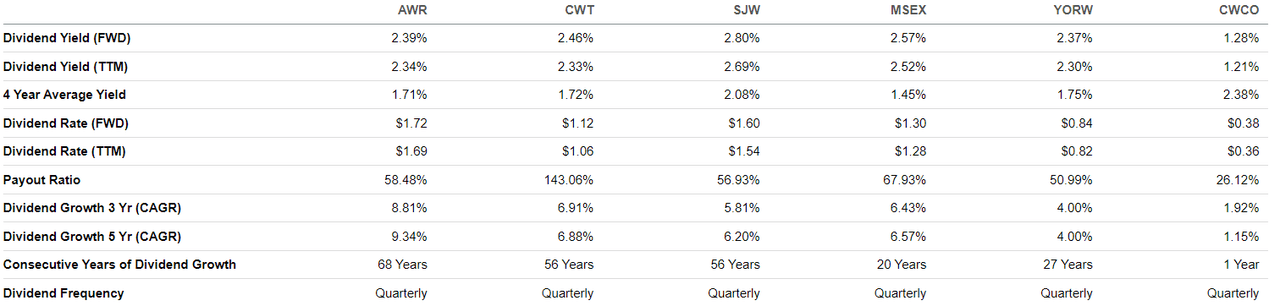

When looking at a Utility company, one of the key reasons that an investor considers while investing in such a company’s stock is its dividend income. And, if we talk about AWR, the company is best in this business in giving an attractive dividend rate that has delivered positive rate increases for the last 68 years consecutively and has reached a dividend yield of 2.39%, which is considered a good figure in Wall Street.

EPS historic growth (Company presentation)

The company’s quarterly dividend rate has grown at a compound annual growth rate of 9.4% over the last 5 years from 2018 through 2023, which is significantly higher than that of AWR’s peers like California Water Service Group (CWT), SJW Group (SJW) and The York Water Company (YORW) which have given 5-year CAGR dividend growth in low to mid-single digits as you can see in the table below.

EPS historic growth versus peers (Seeking Alpha)

In my opinion, this is one of the key deciding factors when it comes to investing in stocks for stability and regular income generation. The Water segment has been contributing significantly to the company’s bottom line, and looking at the promising longer-term outlook of this business, the company’s EPS should continue to deliver above-average dividend growth in the coming years.

Valuation

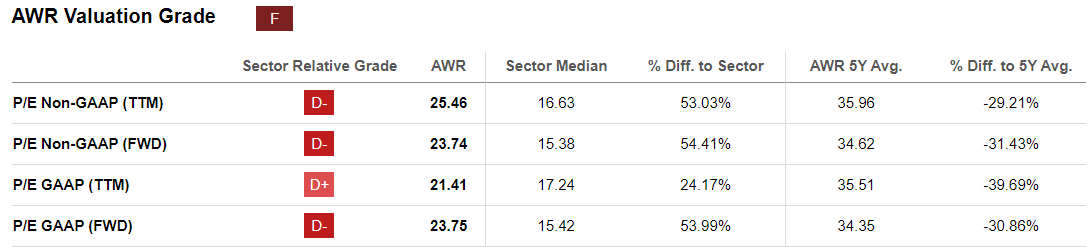

I am using the Price-to-earnings valuation metric as I find it the best way to value a utility company stock which is majorly driven by its earnings growth. Currently, the company’s stock is trading at a forward P/E ratio of23.74 based on 2024 EPS estimates of$3.03. The company’s stock has corrected significantly by more than 20% in the past year, which along with earnings growth has resulted in an improved P/E ratio as it is currently trading at a discount to its 5-year average P/E of 34.62.

AWR valuation grade (Seeking Alpha)

While the stock may look cheaper when compared to its historical levels, it is still at a premium of more than 50% when compared to its sector median. Even if we look at the forward P/E based on FY25 EPS estimates, it appears to be on the higher side than the sector median, which makes this stock valuation unreasonable at the current levels.

Conclusion

As we discussed, the dividend king is currently at a premium valuation as compared to the sector median. The company’s bottom line has experienced strong growth in the past years and should continue to deliver further considering a positive outlook for the company in the longer term. If the stock was trading near its sector median, I would have considered this stock as a good investment for stability and regular dividend income. But, at this level, I am staying on the sideline for now and giving this stock a “HOLD” rating.

Read the full article here