")

Introduction and thesis

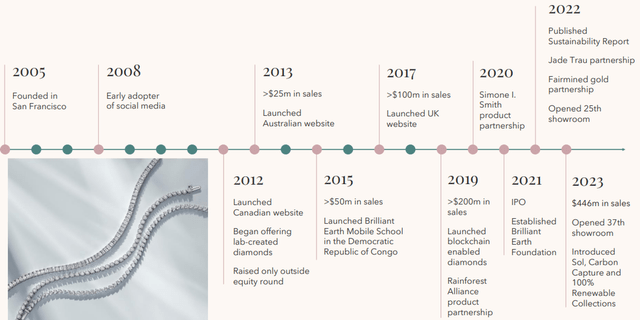

Brilliant Earth Group (NASDAQ:BRLT) is a leading retailer of ethically sourced fine jewelry, specializing in engagement rings, wedding bands, and other diamond and gemstone jewelry. Founded in 2005 and headquartered in San Francisco, California, the company is committed to sustainability, social responsibility, and transparency in the jewelry industry. Brilliant Earth offers a wide range of products, including conflict-free diamonds, recycled precious metals, and ethically sourced gemstones.

BRLT

BRLT has developed well during the last 5 years, albeit remains a small fish in a large ocean. The company has a long way to go before we can confidently say it has a tangible moat and a protectable position. It is highly fragile and will likely see further volatility in the coming decade.

This said, the company is growing well and expanding its geographical presence, underpinned by growth in brand awareness, which should allow market share gains in the years to come. The company must deliver this as the industry growth expected is minimal. This, alongside improving economic conditions, will also deliver some margin improvement.

This alone should be a reason for some positivity, even if you do not believe in the company long-term, yet, BRLT is trading at 3.3x NTM EBITDA. The company’s valuation appears incorrect and seems priced for failure, despite having a net cash position and being a potential takeover target by a PE firm or industry participant.

For these reasons, we rate BRLT a buy.

Share price

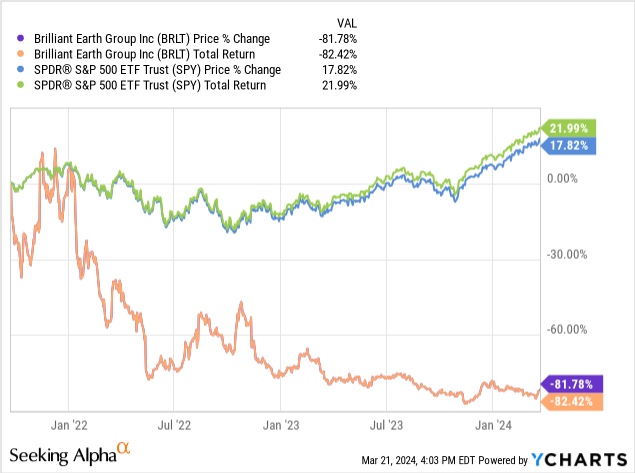

BRLT’s share price has trended in one clear direction during the last decade, losing over 80% of its value since 2021. This is a reflection of a combination of factors, as investor expectations likely priced in a more rapid expansion, while its financial performance has reversed.

Commercial analysis

Capital IQ

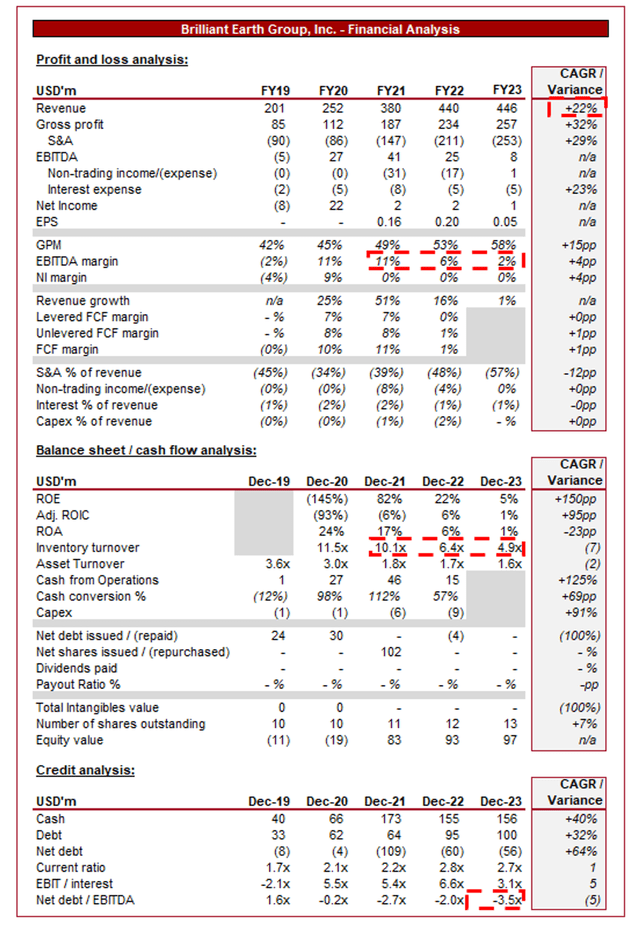

Presented above are BRLT’s financial results.

BRLT’s revenue has grown well during the last 4 years, with a CAGR of +22% into FY23. Unfortunately for the business, its profitability has developed less consistently, with initial gains into FY21, followed by a deterioration subsequently.

Business Model

BRLT specializes in ethically sourcing diamonds and gemstones, ensuring they are conflict-free and mined under fair labor practices. Additionally, the company also sells lab diamonds, further leaning toward the sustainability / ethical cause. This commitment to ethics resonates with socially conscious consumers, who are a growing proportion of society, that prioritize sustainability and ethical business practices.

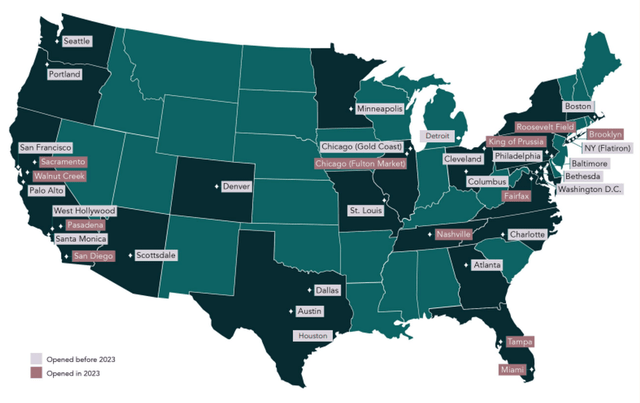

BRLT has quickly developed an omnichannel approach in response to demand, with showrooms nationally alongside its e-commerce offering. The online model provides convenience and accessibility to customers worldwide, particularly those within its core demographic who are increasingly browsing potential purchases online relative to footfall. Underpinning this, however, is a growing showroom network, with over 35 locations and 12 opened in 2023. Given the cost outlay, it is important to support its e-commerce efforts with low friction to viewing its products.

BRLT

One of BRLT’s key selling points is that it offers certified “beyond conflict free” diamonds that adhere to and exceed the Kimberley Process Certification Scheme (KPCS) and other industry standards for ethical sourcing. Each diamond can be fully tracked and comes with a certificate of origin, providing assurance to customers that their purchase supports responsible mining practices. Less than 1% of the world’s diamonds meet this “beyond conflict free” criteria, ensuring the highest commitment to standards and transparency.

As part of the company’s marketing efforts, BRLT prioritizes customer education and transparency, providing comprehensive information about the sourcing, quality, and characteristics of diamonds and gemstones. We believe this is critical for the long-term development of its segment, as relative to the wider jewelry industry, it is tiny. Consumers still lack sufficient education and understanding which will inevitably impact purchasing habits. Management has seen persistent market share growth, with a +46% increase in new customers during 2023. The company is currently winning in the wedding segment, which is expected given this represents a large portion of diamond purchases, however, it must continue to make progress in normalizing the purchase of conflict-free/lab diamonds in a broad range of products.

Finally, in response to industry growth and the company’s momentum, it has progressively expanded its geographic footprint and market presence by targeting new regions and demographics. The company’s online model allows it to reach customers globally already, enabling reduced friction and thus risks. The company has targeted other anglosphere nations, such as the UK and Australia, relying on similar cultures and messaging.

Strategy

Management’s current strategic targets, alongside our comments against each, can be found below:

- Continue on its path to becoming a premier jewelry brand – This is a very vague objective, with no real criteria against which to judge it, other than maybe market share growth. We believe this will be achieved through a combination of further societal education and expanding its retail footprint, the combination of which will expand its addressable market while reducing barriers to purchase.

- Expand and refine its product offering – This sounds oxymoronic. Our interpretation is that in order to operate efficiently and increase margins, a reduction in SKUs and production techniques is needed. Conversely, in order to generate interest and build out its brand, the company must expand its offering. We believe a reduction in SKUs outside of its core wedding offering would be a shrewd decision, focusing on its most popular items. However, it must continue to innovate in different products, such as necklaces, chains, earnings, etc.

- Expand and elevate omnichannel experience – This is fundamentally important. Its brand and experience must foster a mindset that encourages the public to want to purchase its products. Adjacently, as we have mentioned several times, the barriers to purchase must be reduced, consumers are unlikely to spend >$1k from a small brand without seeing the product first, be it a simple returns policy, virtual services, or a showroom experience.

- Invest to drive operational efficiency – BRLT’s margin erosion in the last two years has been a result of runaway operational costs, with S&A spending as a % of revenue increasing by +18ppts since FY21. Management is slightly trapped in that growth is decelerating and so “topping up” marketing spending is required, however, this is currently dilutive. The business needs to find tangible efficiency, be it through an improvement in customer conversion allowing revenue growth to exceed costs or a straight reduction in costs. Currently, we see limited progress outside of one-off costs expected to fall away.

Competitive Positioning

We are not entirely convinced by BRLT’s competitive position. The company is relying upon the following factors (for each we will challenge the value it provides as a moat):

- Providing consumers with “beyond conflict free” diamonds – Whilst this is clearly very important, the company is almost running before it can walk. Conflict-free diamonds now comprise ~99% of all diamonds (this is challenged). For many consumers, this is enough. BRLT, rather than developing a brand purely around its sustainability efforts, seems hell-bent on the perception of being “beyond conflict free”, which is more costly and so may have been better off as a premium line, with lab and conflict free as its standard offering. Essentially, we are not convinced consumers care enough yet about the additional value BRLT provides in this regard.

- Its omnichannel offering – Whilst this is a primary growth driver, it is no different from what many of its peers offer. The company is not different but instead is doing what it needs to generate growth.

- Its designs – This company is seeking to develop distinct, modern, and different designs, which is commendable but designs can be copied and so similar to the point above, it supports growth but does not sufficiently differentiate.

- Its brand – BRLT’s brand development has been impressive and should be praised. As the following illustrates, the company is currently at its peak and (potentially) climbing. This said, it is still a small fish in a big pond. At a market cap of ~$37m, markets assign limited value to this brand after tangible assets.

Google

Conflict-free diamond industry

In recent years, there has been a growing demand for ethical and sustainable jewelry products among consumers who prioritize ethical sourcing and environmental stewardship. We expect this trend to continue in the coming years, as this has been observed across a number of other industries.

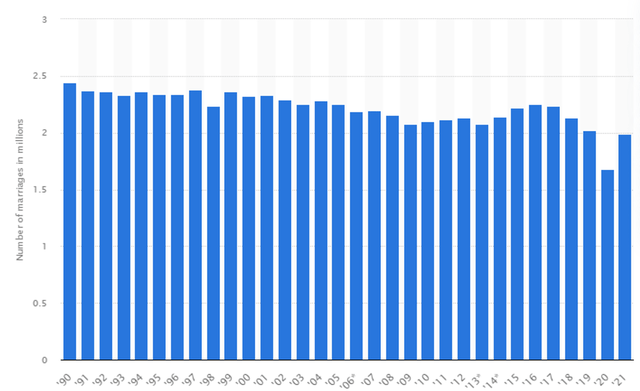

The diamond jewelry industry is forecast to grow at a CAGR of +1.2% in the coming years, a mild figure representing its highly mature nature and limited scope for disruption. Further, we believe this is a reflection of changing consumer behaviors. We have broadly seen a reduction in the number of marriages in the US, despite population growth (which is also expected to slow). This is likely also having a negative impact on growth.

Statista

Competitors in the ethically sourced jewelry market include other online retailers such as James Allen and Blue Nile, as well as traditional brick-and-mortar jewelry stores.

Financials

BRLT’s recent performance has been poor, with top-line growth of -2.3%, +1.3%, +2.5%, and +3.9% in the last four quarters. In conjunction with this, the company’s margins have continued to decline.

During difficult economic conditions, as observed currently with elevated rates and inflation, the demand for jewelry usually declines considerably. This is a highly discretionary purchase that can be easily foregone. Compounding this is a slowdown in the marriage industry, again, as consumers can or are forced to delay. Despite this, BRLT has broadly maintained growth, which is respectable, albeit appears to be a reflection of its wider momentum and also is supported by increased cost investment.

The concern for BRLT is its ability to quickly and effectively lift margins. We believe this will not be an easy task, albeit its existing levels are far below what it can achieve on a normalized basis we feel. Inventory turnover has almost halved since Dec21 and Management is investing heavily in fixed costs (and one-off costs) which are expected to generate future revenue (showrooms). As these factors unwind, the company should see its cost base dilute, allowing for margins to expand.

For this reason, we expect BRLT to see a gradual margin improvement from FY25F onward, with a larger bump between FY24F and FY25F as economic conditions materially improve and strong growth begins its return.

Speaking of growth, we are less certain in this regard. We have seen businesses completely derailed by a slowdown while others have seen downturns as a blip and continued to soar subsequently. Given the investment in growth and its positive brand development, BRLT does appear to fall in the latter category.

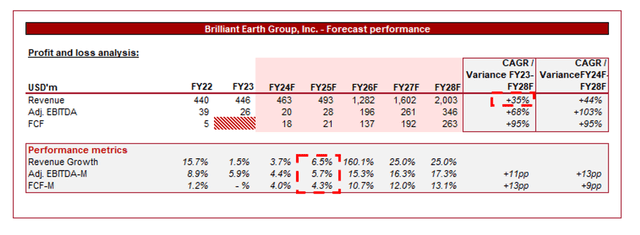

Analysts are expecting impressive revenue growth, with a CAGR of +35% into FY28F. Alongside this, margins are expected to improve considerably, with EBITDA-M up +11ppts.

This appears incredibly bullish in our view, but with insufficient evidence to confidently forecast this. We would see the business closer to a growth rate of ~20%, aligning to historical trends (with upside coming from compounding investment in growth) and margins growing to its post-pandemic levels and slightly beyond (~13%).

Capital IQ

Industry analysis

Seeking Alpha

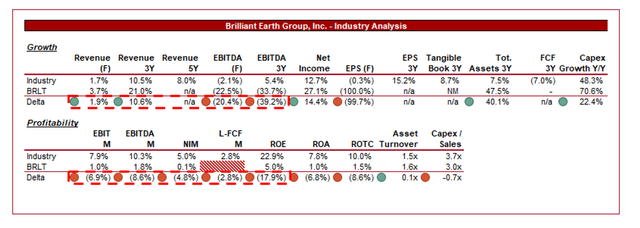

Presented above is a comparison of BRLT’s growth and profitability to the average of its industry, as defined by Seeking Alpha (18 companies).

We will not spend too much time comparing BRLT, given its size and current development cycle. The company has exceeded its peers on growth and comfortably so, albeit generating considerably lower margins.

Importantly, the company should be able to exceed its peers’ 5Y growth rate of ~8%, while its normalized margins could exceed its peers’ average. If Management is able to execute, the company could easily be an attractive specialist retailer.

Valuation

Capital IQ

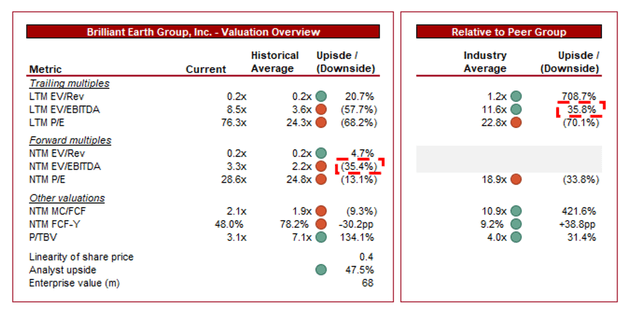

BRLT is currently trading at 9x LTM EBITDA and 3x NTM EBITDA.

A discount to its peer group average is likely a reasonable view, as despite the scope to outperform, BRLT requires strong execution and a long runway for growth to achieve the scale necessary to generate attractive returns. This said, at its current valuation, we do see upside. The company generated FCFs of ~$40m in FY21, which compares to its EV of $68m. Markets have lost all interest in this stock, pushing it into deep value territory, particularly if you buy into its growth story. Importantly, there is no solvency risk here, the company is in a net cash position and could easily burn cash for years without any issue (not that it will).

At a NTM EBITDA multiple of 3.3x, the company’s downside appears protected. At such a valuation, we believe the business is the perfect takeover target for a PE that believes it can brand build, conduct incremental bolt-ons, and expand its geographical presence to grow, with the view of selling the company to a market participant.

Key risks with our thesis

The risks to our current thesis are:

- Competition from Traditional Retailers – Traditional brick-and-mortar jewelry retailers will pose a growing threat to BRLT’s market share as it continues to grow, particularly if they start offering similar ethically sourced products.

- Supply Chain Risks – Disruptions in the supply chain, such as issues with diamond or gemstone sourcing meeting its strict criteria, could impact BRLT’s ability to maintain its commitment to ethical and sustainable practices.

Final thoughts

We are not convinced by BRLT’s long-term value proposition. Whilst Management has done well to take this business this far, it still has many weaknesses which have yet to be addressed. Further, the industry’s growth as a whole is unlikely to be attractive, increasing reliance on market share gains to generate strong returns.

This said, valuation is key to putting things in context. At a 3x NTM EBITDA valuation, we believe the company is fairly solid. It may not look amazing in isolation, but it does at 3x NTM EBITDA. We believe investors could do well from holding this stock for the medium-term, expecting an improvement in performance to drive a re-rating of its valuation to a more reasonable level (5-8x).

For this reason, we rate the stock a buy.

Read the full article here