")

Chubb Limited (NYSE:CB) has had a phenomenal financial performance after my previous analysis, posting increasing margins and solid revenue growth beyond my previous analysis’ expectations. More recently in Q1, Warren Buffett seems to have noted the stock as a good buying opportunity, as a recent 13F filing shows Berkshire Hathaway’s (BRK.A) (BRK.B) newly bought stake in Chubb.

I previously wrote an article on Chubb titled “Chubb: A Relatively Cheap Savehaven“, rating the stock at buy due to a seeming undervaluation with Chubb’s stable earnings. The text was published on the 11th of September in 2023. Since, the stock has had a total return of 34% compared to an S&P 500 appreciation of 18%. The company continues to post good financials, and the stock continues to be undervalued despite a higher stock price.

My Rating History on CB (Seeking Alpha)

Chubb’s Financial Performance Has Been Great

Chubb has had an incredibly good financial performance after my previous analysis, posting great growth throughout Q3/2023 to Q1/2024. Most recently in Q1, Chubb showed a 14.2% year-over-year growth in net premiums written with a constantly good performance between segments. Most notably in the quarter, life insurance premiums written showed a growth of 26.3%.

Along with good revenue growth, Chubb has posted increasing margins. Chubb had a 20.3% year-over-year growth in core operating income in Q1, raising the margin compared to written premiums to 18.1% compared to 17.2% in Q1/2023. Chubb continues to see favourable effects from higher pricing contributing both to growth in written premiums in dollar terms and higher margins.

The Q1 financials follow a good second half of 2023, where Chubb also managed to grow written premiums and operating margins beyond my previous analysis’ DCF model expectations. While pricing increases can’t be extrapolated further very much, they still look to sustainably raise Chubb’s operating margin level expectations. As Chubb’s earnings have grown well, the company recently raised its dividend into a quarterly payment of $0.91, making the stock’s current dividend yield a relatively low 1.33%.

Warren Buffett’s Berkshire Hathaway Buys a Stake in Chubb

With a recent 13F filing released on the 15th of May, Warren Buffett’s investment firm Berkshire Hathaway disclosed a 25.9 million share stake in Chubb worth around $7.1 billion at the time of writing. The stock rose by 5% on the 16th of May following the 13F disclosure as Berkshire Hathaway has taken a significant position in the company, representing around 6% of Chubb’s total shares.

Berkshire Hathaway had been building a position in the company in previous quarters under a confidential filing. It seems that the position has now been built with no significant further add-ons likely as Berkshire Hathaway has no longer seeked confidentiality for the stock purchases. With Berkshire Hathaway already holding significant positions in insurance, I don’t expect that an acquisition is likely due to regulatory issues – Warren Buffett’s position in the company doesn’t look likely to concretely affect the investment case for Chubb, although a vote of confidence from the investment mogul strengthens faith in the investment.

Competitive Industry

The property and casualty insurance industry has a large number of competitors. For example, publicly traded The Progressive Corporation (PGR), The Travelers Companies (TRV), and The Allstate Corporation (ALL) have a combined market capitalization of $218 billion. Insurance is overall a challenging industry to drive differentiation from competitors in, as the service is highly standardized with pricing being the clearest form of differentiation.

Still, compared to the mentioned large publicly traded competitors, Chubb has managed to grow earnings more consistently. While the competitors seem to also have benefited from increased pricing in recent quarters raising margins, Chubb’s growth in the industry has overall been more stable. Chubb boasts a clearly better underwriting ratio compared to several competitors, making the company very competitive in the industry.

Overall, the P&C insurance industry is expected to have a good 2024. The Swiss Re Institute estimates premiums to show a growth of 7.0% in the year driven by personal lines. Easing inflation and better investment returns are also expected to improve the industry’s profitability into a ROE of 9.5% in 2024 and 10.0% in 2025, which can already be seen in Chubb’s and its competitors’ margins.

Valuation Continues to Have Significant Upside

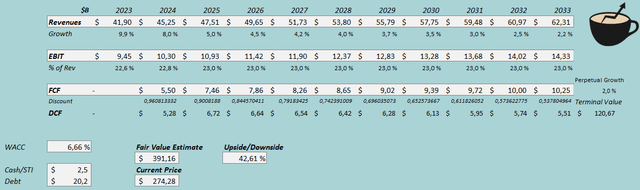

Due to Chubb’s great financials in recent quarters, my DCF model’s assumptions see room for change. I now estimate revenues based on net premiums written in P&C and estimate a CAGR of 4.0% from 2023 to 2033, compared to a CAGR of 3.7% from 2022 to 2032 in my previous DCF model. The perpetual growth rate is unchanged at 2%. Due to Chubb’s higher reported margins, I now estimate the company’s operating income at a significantly higher level – for example for 2024, I now estimate an EBIT of $10.3 billion instead of $8.2 billion in my previous DCF model representing a margin of 22.8% in 2024 and 23.0% from 2025 forward. I adjusted the cash flow conversion downwards.

With the mentioned estimates, the DCF model estimates Chubb’s fair value at $391.16, around 43% above the stock price at the time of writing. The stock continues to have a seeming undervaluation as the recent earnings trajectory has raised my cash flow estimates significantly.

DCF Model (Author’s Calculation)

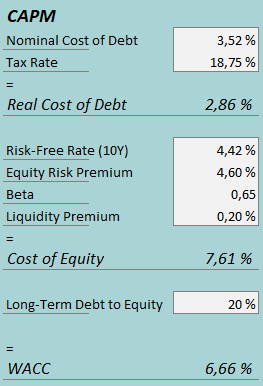

A weighted average cost of capital of 6.66% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q1, Chubb had $178 million in interest expenses. With the company’s current amount of interest-bearing debt, Chubb’s annualized interest rate comes up to 3.52%. I keep my long-term debt-to-equity ratio estimate the same at 20%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.42%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. I use the same beta estimate of 0.65 as in the previous CAPM. Finally, I add a small liquidity premium of 0.2%, creating a cost of equity of 7.61% and a WACC of 6.66%. The WACC is down from a previous estimate of 7.38% due to a lower equity risk premium estimate.

Risks

While Chubb is relatively resistant to macroeconomic turbulence, the company isn’t entirely immune to macroeconomic factors. Chubb has a good amount of debt on the company’s balance sheet – interest rates have an effect on the company, although the effect is quite modest.

Chubb’s recent high margins could also only be high temporarily, and potential margin deterioration could worsen the investment case considerably. A significant catastrophe could cause Chubb significant losses leading to worsening earnings – for example, the company has lost a significant amount due to the Baltimore bridge collapse. Chubb does have a global and diversified insurance portfolio with only 19% of premiums coming from large corporate commercial P&C, though, making very significant one-off payments unlikely to cause too much earnings turbulence.

Takeaway

Chubb’s financial performance after my previous analysis has been great, characterized by good growth and high margins with the company’s price increases. Warren Buffett’s Berkshire Hathaway has also taken notice of Chubb’s good financials, as the company has bought a stake worth $7.1 billion in the company as per a recent 13F filing. While concrete changes in the investment case isn’t altered by the Berkshire Hathaway stake, the company’s stake in Chubb solidifies faith in the investment. The valuation continues to provide a good price for investors, and as such, I keep my rating for Chubb at buy.

Read the full article here

")

")

")

")