")

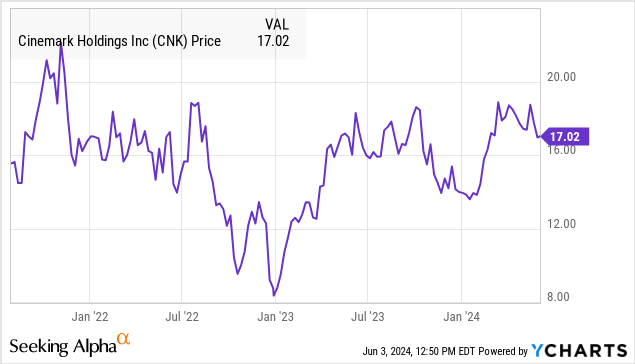

Cinemark Holdings, Inc. (NYSE:CNK) has done a good job of navigating a historically difficult last couple of years in the movie theater business.

Compared to the pandemic-era shutdown, the company is back to profitability and making progress in paying down debt. We last covered CNK in 2022 highlighting these trends while the stock has been nearly flat over the period.

The latest challenge is dealing with disappointing movie theater attendance, which has declined to start 2024 as a global industry trend. Cinemark remains confident conditions can improve, but the backdrop with lower earnings doesn’t inspire much confidence for investors. In our view, until there is evidence of a growth rebound, we expect shares to remain volatile.

CNK Earnings Recap

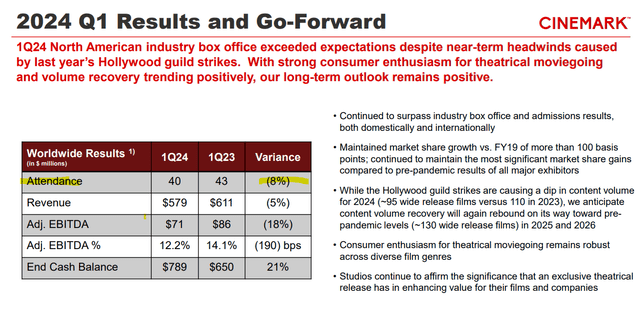

CNK reported Q1 EPS of $0.19, reversing a loss of -$0.03 in Q1 2023. Revenue of $579 million was down by -5.2% year-over-year but did exceed the consensus estimate by $16.8 million.

Cinemark’s worldwide attendance this quarter of 40 million patrons was down by -7.5% from the period last year. Some of the weakness at the box office was anticipated, considering the 2023 Hollywood Guild writers strike slowed the cadence of movie releases into Q1.

Efforts to raise pricing on the ticket side as well as concessions at least helped balance some of that top-line decline. For the North American market where the company generates approximately 79% of total business, the average ticket price of $9.82 was up 1.1% from $9.71 in Q1 2023. Similarly, the average concession sales per patron of $7.57 increased by 2.2%.

Nevertheless, the lower volumes resulted in a Q1 adjusted EBITDA of $71 million, declining by -18% y/y.

source: company IR

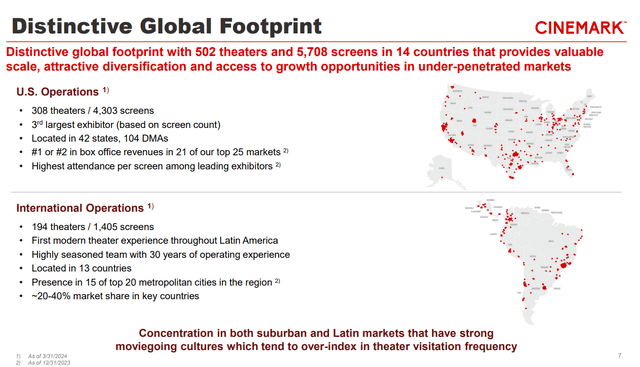

If there is a silver lining, Cinemark notes that it has gained market share in North America which reached 14% in 2023 compared to 13% in 2019 as a pre-pandemic benchmark. The company also accounts for 25% of the box office gross receipts in Latin America, up from 23% in 2019.

source: company IR

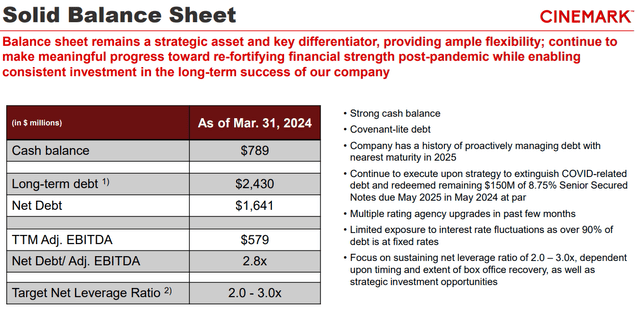

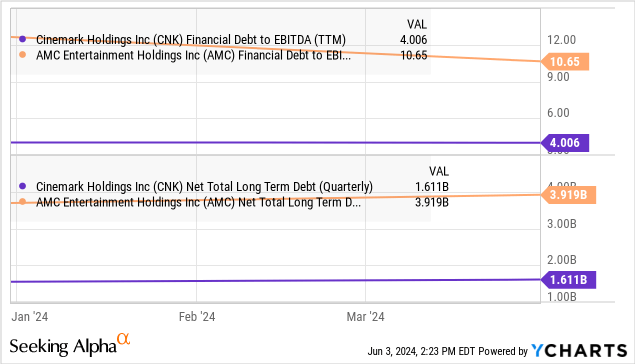

The other strong point is the improving balance sheet. Cinemark ended Q1 with $789 million in cash, against $2.4 billion in long-term debt. Considering trailing twelve-month adjusted EBITDA of $579 million, a net leverage ratio of 2.8x has favorably narrowed from 4.7x in Q1 2023.

source: company IR

What’s Next for CNK?

The attraction of Cinemark is the company’s resiliency in the industry, where it has proven capable of adjusting to changing consumer trends while surviving the pandemic.

Compared to its larger competitor in AMC Entertainment Holdings, Inc. (AMC), which commands a 24% market share of the North American box office, CNK’s advantage is its stronger fundamentals including current profitability and a less leveraged balance sheet.

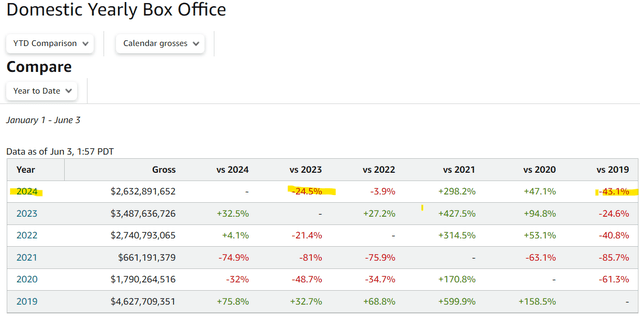

Still, the box office trends have been disappointing and continue to represent a major headwind for financials to keep improving. Data from the industry tracking group, “Box Office Mojo,” shows that year-to-date movie theater box office sales of $2.6 billion are down -24.5% from the same period in 2023. The pace is also below 2022 and -43.1% under 2019 pre-pandemic benchmarks.

There is a concern that the industry rebound in terms of attendance and ticket sales have stalled even beyond the Hollywood writer’s strike impact. The recent Memorial Day weekend was the weakest in more than two decades, excluding 2020 and 2021.

source: Box Office Mojo

The sense is that moviegoers are becoming less excited about the latest premieres, with Hollywood missing a big blockbuster to break records. That’s a problem when thinking about CNK, where the current second quarter is tracking poorly, and it becomes unclear when the trends will turn around.

Again, there is some expectation that the box office will pick up as Hollywood ramps up its release schedule, but it is far from certain whether simply having more options will bring moviegoers back in force.

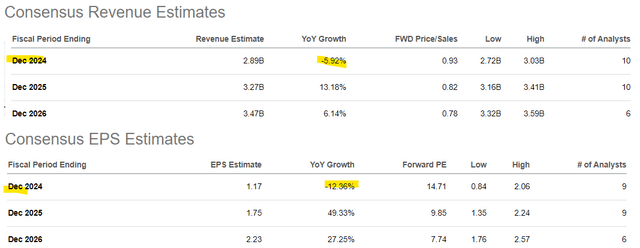

According to consensus, the market forecasts CNK 2024 revenue to decline by -6% while EPS could be -12% lower. The forecasts for 2025 appear aspirational, with the market penciling in a 13% growth rebound and EPS to surge by nearly 50%.

We’d say there is room for skepticism with the risk that these figures need to be revised lower, in the context of the macro setup where consumer spending indicators have been under pressure against stubborn inflation and high interest rates.

Weaker-than-expected results from Cinemark over the next few quarters could open the door for a deeper selloff in the stock.

Seeking Alpha

Final Thoughts

We rate Cinemark Holdings, Inc. stock as a hold, implying a neutral view of the share price over the next six months to one year. We’d suggest most investors simply avoid the name, given the number of near-term uncertainties.

At the same time, we believe the long-term outlook remains positive. Strategic moves to manage pricing or readjusting capacity by focusing on the best-performing locations could be enough to support earnings momentum. Ultimately, even if the movie theater industry remains in a structural decline, Cinemark can still capitalize on its leadership position and regional diversification.

Read the full article here