")

Introduction & Investment Thesis

Duolingo (NASDAQ:NASDAQ:DUOL) is a language learning app that expanded its offerings to Maths and Music in FY23. The company has been underperforming the S&P 500 and Nasdaq 100 YTD. I had last covered the stock on May 10 after its Q1 FY24 earnings report, where I held my “buy” rating as I believed that the stock offered an attractive entry point after it beat estimates for revenue and earnings growth. Unfortunately, since then, the stock has declined over 12%, underperforming the indices.

The company is due to report its Q2 FY24 earnings on August 7th, where revenue and Adjusted EBITDA are expected to grow 38% and 82% YoY to $176.25M and $37.95M respectively. While beating these estimates will be a positive sign, I believe investors will be looking at whether the management raises its guidance for the full year FY24. On that front, since its Q1 earnings, OpenAI has launched ChatGPT 4-o, which can stand to compete with Duolingo’s target market of language, Math and Music learners. Therefore, it will be important to look at the trend of Daily and Monthly Active Users along with the penetration rate of Paid Subscribers as a percentage of Monthly Active Users to understand how the management is planning to build out its product roadmap to maintain its competitive positioning.

After assessing both the “good” and the “bad,” I believe that it is important to stay prudent, as any slowdown in revenue or earnings growth can lead to short-term downward pressure on the stock. Therefore, I will downgrade my rating from “buy” to “hold” at the moment as I await the quarterly results.

A quick preview of Duolingo’s Q1 FY24 earnings

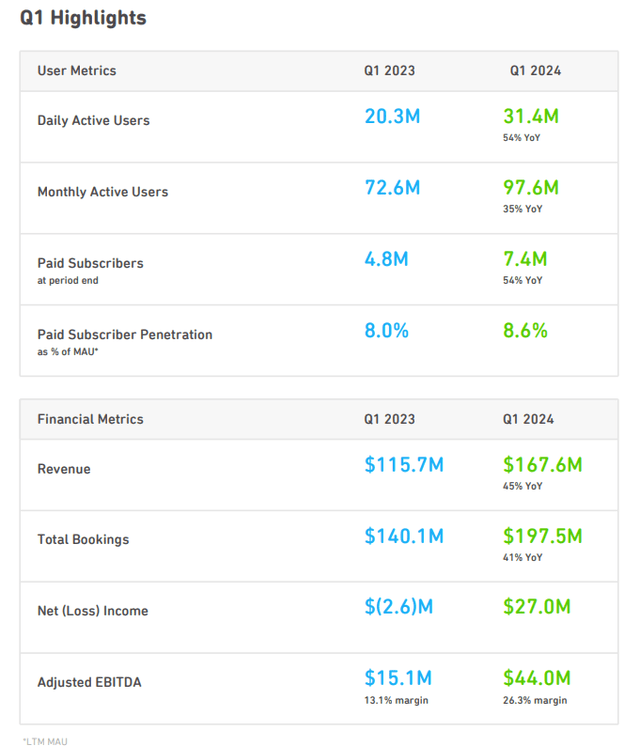

Duolingo reported its Q1 FY24 earnings in early May, where revenue and operating income grew 45% and 190% YoY respectively, beating estimates. What was particularly strong in the report was that Paid Subscribers had grown 54% YoY and 12% sequentially to 7.4M indicating a higher conversion rate from MAUs, as the company was continuing to drive deep user engagement on its platform through creative acquisition marketing campaigns as well as iterating on its gamification strategies by integrating AI into their products.

At the same time, the company continued to expand its operating margins as it grew from 13.1% to 26.4% YoY, as they streamlined their operating expenses while unlocking operating leverage from a higher conversion rate from freemium to paid subscribers, increasing the rollout of their highest subscription tier, Duolingo Max, and growing in-app purchases on the platform.

Q1 FY24 Shareholder Letter: Performance of Key Metrics

Key updates since the earnings call

-

Since Duolingo’s last earnings call, OpenAI has announced ChatGPT 4-o, which will be available for free for everyone as a desktop app soon. People are just starting to get access to Advanced Voice Mode, which can translate languages, have real-time conversational speech, and even be sarcastic. During its demo in mid May, we saw that it can solve math problems, help you learn languages, and more. What I am trying to say is that although Duolingo has been leveraging the capabilities of ChatGPT 4-o on its Duolingo Max subscription tier to provide advanced learning experiences, the natural language processing capabilities of ChatGPT 4-o can similarly engage users in conversational practice, provide instant feedback, and tailor lessons to individuals needs, thus threatening Duolingo’s market share in the language learning space as well as its emerging categories such as Maths and Music. Although Duolingo differentiates itself with its engaging gamification strategies, I believe it needs to continue to innovate by integrating AI-driven features or expanding into educational domains to retain and grow its user base.

-

At the same time, Duolingo also acquired Hobbes, which is an animation and motion design studio, where I believe it is likely to look to amplify its game mechanics to make its products fun, engaging, and sticky, something that differentiates it from ChatGPT 4-o and upcoming startups in personalized learning and enables it to defend its moat on “edutainment.” While specific financial terms of the deal have not been publicly disclosed, I believe it will likely fund the acquisition using its cash reserves.

Things to watch out for in Q2 FY24 earnings

Duolingo is due to report its Q2 FY24 earnings on August 7th, where it is expected to report a revenue growth of 38.9% to approximately $176.25M, with an Adjusted EBITDA margin of approximately 21.5% to $36.8M. While beating its Q2 estimates will be a positive sign, I believe that investors will be looking for commentary and insight on the following metrics when assessing its long-term investment opportunity.

-

Revenue growth: In the last earnings call, the management raised its revenue and earnings guidance for the full year FY24, where revenue is expected to grow 38% to $731M. Investors will be looking to see if the management keeps its guidance anchored or raises it. Any softness in its projection will point to growing competitive threats in the industry as well as a pullback in consumer spending.

- DAU/MAU and Paid Subscribers: One of the ways in which investors can assess how effectively the company is acquiring and retaining its customers on the platform will be through the growth rate of its Daily and Monthly Active Users, which will suggest that its product innovation strategies to drive user engagement are continuing to pay off. In the last quarter, Daily and Monthly Active Users stood at 20.3M and 72.6M respectively. At the same time, we would also need to pay attention to the Paid Subscriber Penetration rate, which stood at 8.6% and investor sentiment will be highly dependent on this metric, as it is directly linked to the effectiveness of Duolingo’s monetization strategies.

- Individual revenue segments: Meanwhile, Duolingo’s revenue consists of four categories that include Subscription, Advertising, Duolingo English Test and In-App Purchases. While Subscription revenues are the heavyweight contributing over 78% to Total Revenue in Q1, they are also the fastest-growing among all other revenue segments. Therefore, investors will focus on this metric. However, lately, In-App purchases have been growing steadily, indicating the level of customer engagement on the platform. And while it only contributes 6% to Total revenue growth, it is, in my opinion, a good indicator to track overall user sentiment.

2. Adjusted EBITDA: For FY24, the company is expected to generate Adjusted EBITDA of approximately $171.8M with a margin of 23.5%. This is compared to 17.6% Adjusted EBITDA in FY23, which highlights the management’s financial discipline. Once again, investors will be looking to see where the management holds or raises its guidance on this front. However, I would like to point out that should it start to see a slowdown in new customer acquisition, increased churn, or a slower conversion rate from freemium to Paid, it will start to squeeze margins, especially as it needs to continue investing in product innovation to maintain its competitive positioning.

Revisiting my valuation: It’s time to exercise caution.

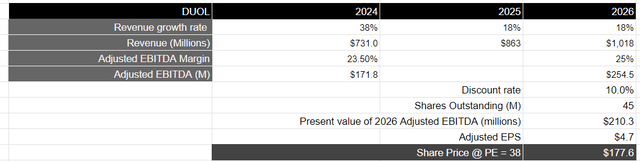

In my previous post, I assumed that Duolingo would meet its FY24 revenue target of 38% while growing in its high twenties range after that as it develops advanced English content along with driving market share in new addressable markets such as Maths and Music. However, in this earnings call, we will get an early sentiment check from the management as to the current threat ChatGPT 4-o presents and how they are planning to navigate the current and future environments. While it is certainly possible that Duolingo will find innovative solutions to continue to attract, engage, and monetize users on its platform as it expands its addressable market, I believe that the threat from OpenAI cannot be fully quantified, and as a result, I will take a bearish scenario, where I will now expect the company to grow its revenues in the high teens range, which is much slower than my previous estimate of the high teens range. Please note that this is also below the consensus estimates for revenue growth. In this scenario, Duolingo will generate a total revenue of $1B by FY26, with an Adjusted EBITDA of 25% at $254M, which will be equivalent to the present value of $210M when discounted at 10%.

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% over a 10-year period, with a price-to-earnings ratio of 15–18, I believe that Duolingo will trade at slightly over 2x the multiple (as opposed to 3x in the previous write-up) with a PE ratio of 38 and a price target of $177, which represents an upside of around 8% from its current levels.

Author’s Valuation Model

My final verdict and conclusions

Although the company has operationally outperformed as it is seeing strong revenue growth and expanding margins from targeted product innovation, I believe we need to be on alert at the moment and look for further commentary and guidance from the management to assess how it is planning to navigate the threat that ChatGPT 4-o poses to Duolingo. Should revenue growth indeed slow down into the high teens in the coming years, then I believe that the stock price may face some strong short-term headwinds. On the other hand, Duolingo has mastered the art of user engagement and monetization on the platform, so I will be looking to hear how it will drive product innovation and market share gains moving forward. Assessing both the “good” and the “bad,” I believe it is prudent to stay on the sidelines at the moment. Therefore, I will downgrade my rating from a “buy” to a “hold” at the moment as I await the Q2 results to assess its long-term investment thesis.

Read the full article here

")

(NYSE:SNOW)")

")

Morgan Stanley Technology, Media & Telecom Conference (Transcript)")