")

Investment Thesis

Franklin Electric’s (NASDAQ:FELE) growth prospects remain mixed for the current year. Revenue should continue to see headwinds in the near term from a declining backlog due to lower demand, channel inventory destocking, and project delays by clients in a high-interest environment. Further, tough comparisons in 1H24, and the dissipating impact of price increases should also negatively impact revenue. This revenue decline should start bottoming in the second half of 2024 as the company benefits from easing comparisons in 2H24, and a potential interest rate cycle reversal helping project investments.

Margin should see a similar trajectory with headwinds from volume deleverage in the first half and then some improvement in the back half. The stock is trading at a slight discount versus the historical average but is not compelling enough given the near-term headwinds. Hence, I continue my neutral rating.

Revenue Analysis and Outlook

In my previous article, I discussed the concerns regarding near-term revenue growth due to a declining backlog, channel inventory destocking, and project deferrals from clients due to high-interest rates. The company reported earnings for its fourth quarter of 2023 since then and similar dynamics were seen there as well.

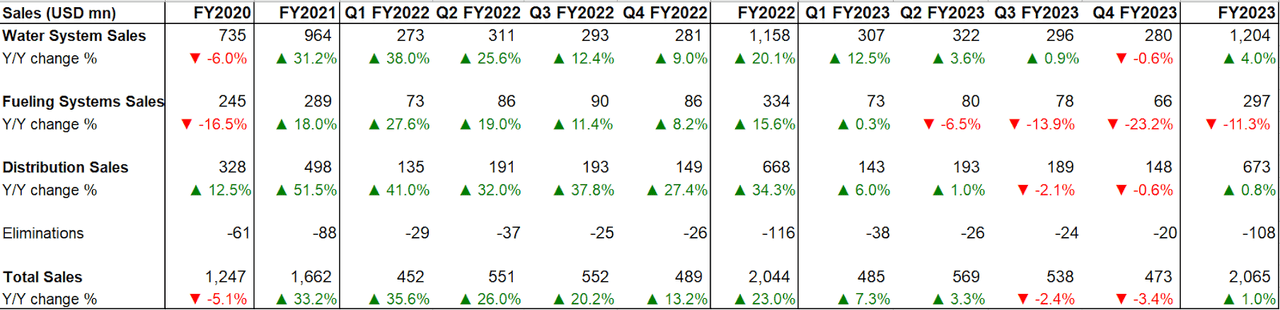

In the fourth quarter of 2023, the company’s revenue growth was negatively impacted by lower volume due to continued channel inventory destocking, adverse weather conditions, unfavorable foreign exchange, and project deferrals from a high-interest rate environment. These headwinds more than offset benefits from price increases, and good demand for large dewatering products in the Water System segment. As a result, revenue declined by 3.4% YoY to $473 million. Excluding a 3% impact from unfavorable FX, revenue growth was flat as compared to last year’s quarter.

On a segment basis, the Water System segment’s revenue declined by 0.6% YoY as good demand for large dewatering products was more than offset by unfavorable FX, lower volumes in brown water pumping systems due to channel inventory destocking, and weather conditions. The Fueling Systems segment’s revenue declined by 23.2% YoY as a result of continued inventory destocking by customers, and project deferrals in an inflationary environment. Lastly, the Distribution System segment’s revenue declined by 0.6% YoY due to general seasonality, channel inventory destocking, and continued unfavorable weather patterns in the U.S.

FELE’s Historical Revenue (Company Data, GS Analytics Research)

Looking forward, I believe the company’s revenue growth should continue to be impacted by a declining backlog, channel inventory destocking, project deferrals, and lower pricing benefits in the coming quarters. I expect the revenue decline to start bottoming in the second half of 2024 due to easing comps, and a potential interest rate cycle reversal.

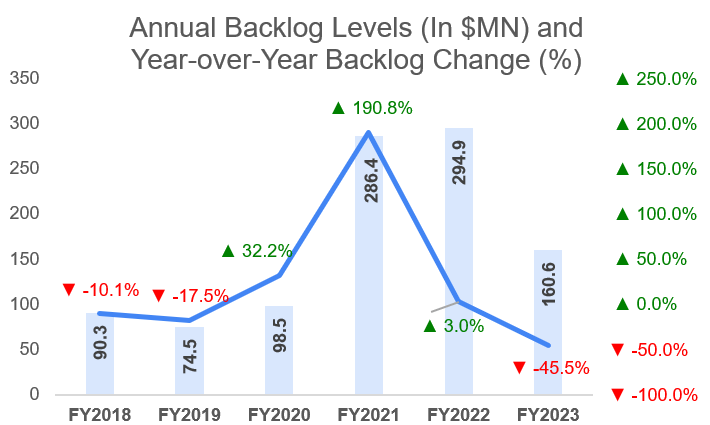

In 2021 and 2022, the company’s backlog and sales benefited from strong end-market demand and price increases. Further, channel partners built inventory and increased orders due to supply chain disruptions. However, as we entered fiscal 2023, the end market began to slow down with lower housing starts and project deferrals in a high-interest rate environment. The channel partners also began reducing inventory levels as supply chain constraints eased and end-market demand slowed. This impacted the backlog levels and the company’s backlog decreased by 45.5% YoY to $161 mn at the FY2023 end.

FELE’s Historical Backlog Levels (Company Data, GS Analytics Research)

Since backlog is a leading indicator of revenue, this backlog decline doesn’t bode well for the company’s growth in the current year. Moreover, the company entered 2023 with elevated backlog levels from peak demand years, which benefited the sales growth in 1H23 despite weakening end markets. This has resulted in tough comparisons in the next couple of quarters which should negatively impact sales growth.

Another factor that has helped the company’s revenue over the last few years was the strong pricing environment but with inflation moderating, I don’t expect the company to take significant pricing action moving forward, implying pricing benefit should dissipate.

While the near term remains challenging I expect the company’s sales decline to start bottoming in the second half of 2024. In the second half, revenue growth comparisons are becoming easy, which should help with year-over-year growth. In addition, there is a potential expectation of interest rate cycle reversal in 2H24, which should boost client confidence and stop the project deferrals, helping back-half recovery. Moreover, with potential interest rate cycle reversal housing starts are also expected to improve from last year’s lows. This should benefit sales growth in the Water System segment. Hence, I expect revenue to start recovering towards the end of the current year.

In a nutshell, while the company’s near-term revenue outlook remains challenging, I am expecting some improvements starting back half of this year.

Margin Analysis and Outlook

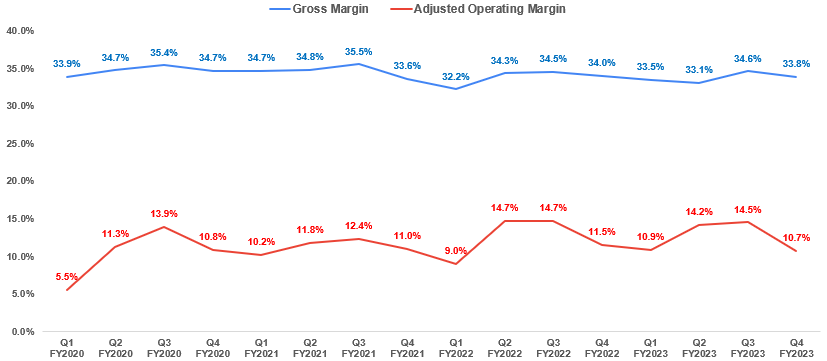

In the fourth quarter of 2023, the company’s margins were negatively impacted by volume deleveraging from declining sales volume across the three segments. In addition, higher operating expenses also impacted the margins. This more than offset benefits from pricing, and high-margin product mix at the company’s Fueling system segment. As a result, gross margin declined by 20 bps YoY to 33.8%, and the total company-adjusted operating margin declined by 80 bps YoY to 10.7%.

FELE’s Adjusted Operating margin and Gross margin (Company Data, GS Analytics Research)

On a segment basis, Water System’s adjusted operating margin declined by 10 bps YoY due to volume deleveraging and high operating costs. Fueling Sytem’s adjusted operating margin increased by 100 bps YoY due to cost control measures, and high margin project mix. Lastly, the Distribution System’s adjusted operating margin declined by 120 bps due to lower pricing on commodity-based products, and volume deleveraging.

FELE’s Segment-wise Adjusted Operating margin (Company Data, GS Analytics Research)

Looking forward, the company’s margin outlook also remains mixed in the near term. In the first half of 2024, the margins should continue to be negatively impacted by volume deleveraging due to declining sales as discussed in the revenue outlook above. This should more than offset the benefits of cost control measures by the company. However, as we move into the second half of the year, moderating inflation, high margin project mix at the fueling system segment, and benefits from volume leverage with sales bottoming should help margins to recover.

Valuation and Conclusion

The company is trading at a 24.14x FY24 consensus EPS estimate of $4.32, which is below its historical 5-year average forward P/E of 24.95x. While the valuation is at a slight discount versus historical levels, I don’t find it attractive enough given the near-term headwinds the company is facing. I also have concerns about the company’s Fuel segment which primarily serves traditional gas stations. While the company has begun offering some products targeting the EV space, they are relatively smaller and the majority of sales of the segment faces secular risk from a shift towards EV vehicles. So, I am not comfortable buying the stock at a mid-20s P/E valuation. I will revisit the company towards the back half of this year as the sales bottom and probably wait for a better price point before becoming more optimistic about the stock. For now, I have a neutral rating.

Read the full article here

")

")

")

Q2 2025 Earnings Call Transcript")

")

")

")