The old behemoth that was General Electric (NYSE:GE) in the 90s and 2000s and that legendary CEO Jack Welch built is no more. Headed by CEO Larry Culp who took over a debt-ridden, bloated and inefficient entity in 2018, GE has completed a series of divestments and spin-offs to restructure itself, emerging as a fully transformed new company. Following the spin-off of GE Healthcare in 2023 and with its power and energy division Vernova having spun-off earlier this week, the new GE (now known as GE Aerospace) will be laser-focused on the Aerospace and Defense markets and sport a lean and efficient operating model, inspired by the Japanese “kaizen” management philosophy.

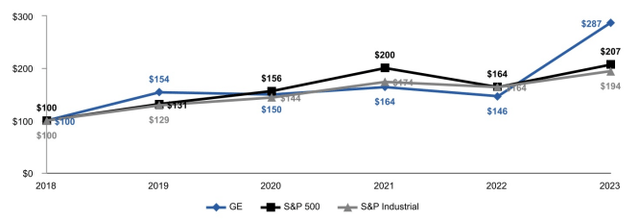

Driven by enthusiasm about Culp’s work and the post-Covid aviation rebound, GE shares have outperformed both the S&P 500 and the broader industrial sector over the past years. I believe this outperformance can continue through an attractive blend of superior fundamentals, an emerging transition towards the LEAP and GEnx engine families and a favorable industry backdrop. I initiate GE shares at Overweight with a YE24 price target of $164, based on a peer-derived 25x multiple on 26E FCF/sh.

GE IR

[Note: “GE” refers to the new standalone company that was formerly GE’s Aerospace division and is now called GE Aerospace, trading under the GE ticker following the spin-off of GE Vernova. All company projections from the March 7 Investor Day and GE’s latest 10-K.]

Company Overview

Following the Vernova spin-off, GE’s operational focus is the design and production of commercial and defense aircraft engines (Original Equipment “OE”) as well as the aftermarket provision of spare parts and maintenance, repair & overhaul (“MRO”) services. As of 2024, engines manufactured by GE or its associated JVs powered 3 in 4 global flights at an installed base of ~70k. Total FY23 sales amounted to $32B, making it the largest engine OEM ahead of RTX’ Pratt & Whitney (RTX), Safran (OTCPK:SAFRF), MTU Aero Engines (OTCPK:MTUAF) and Rolls-Royce (OTCPK:RYCEY).

Commercial Engines and Services (“CES”) – This segment manufactures jet engines for commercial aircraft across narrowbody, widebody and regional jets for all major airframers including Airbus, Boeing and Embraer. Key products include the narrowbody CFM56 engine, designed by CFM, a longstanding 50/50 JV with French Safran and the GE90 which powers the Boeing 777. The division has also an active 50/50 JV with Pratt & Whitney named Engine Alliance, which manufactures one of the two engine options for the A380. During FY23 the segment generated total sales of $23.7B or ~72% of group revenues.

With its workhorse CFM56 and GE90 engines maturing, the segment is currently in the beginning of its transition towards the next generation of commercial engines, namely the narrowbody CFM LEAP and widebody GEnx/GE90 families which have recently began their global rollout. Given high R&D intensity and effects of scale, competition is generally limited with P&W and MTU (as partner in the GTF-program) being the prime contenders in narrowbody, and British Rolls-Royce the main competitor in widebody aircraft through its Trent engine series. Safran would technically also qualify, however due to the large overlap between the two company’s especially in engines developed by their CFM JV I do not view them as a direct competitor.

Defense & Propulsion Technologies (DP&T) – The DP&T division manufactures jet engines for defense airframes including fighters, bombers, helicopters and surveillance aircraft, as well as marine applications. Similar to commercial, competition is relatively limited with P&W manufactured engines being the main alternative across fixed wing and rotary aircraft. It also produces and markets avionics systems and aviation power systems alongside turboprop engines for smaller and regional aircraft. As of FY23 the segment constituted ~28% of group revenues at $9B in total.

Key Investment Thesis

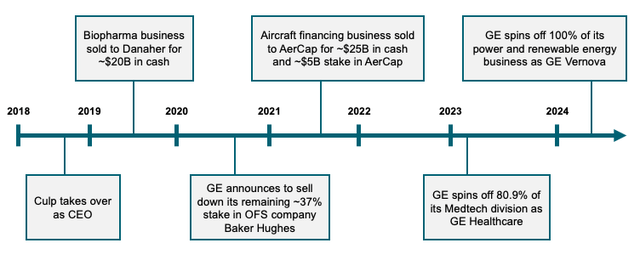

Greatly simplified and deleveraged org structure with Vernova spin-off as final act. When Culp took charge as CEO of General Electric in 2018 he was the first outsider to ever serve on the post, notably not “indoctrined” with the Jack Welch DNA and probably being exactly what the company needed at that time. The GE he inherited was ridden with more than $120B in debt, a late consequence of the Great Financial Crisis of 08/09 and the subsequent implosion of GE Capital, the financial Do-It-All that Welch and Immelt built. Upon his arrival, Culp quickly ditched previous plans to IPO the company’s entire healthcare division, then comprised of Medtech (later spun-off as GE Healthcare) and biopharma, instead aiming to first reduce the massive debt load through targeted divestments.

In 2019 the biopharma business was sold to Danaher, Culp’s previous employer, for a consideration of ~$20B in cash. He further sold the aviation financing arm of what used to be GE Capital to AerCap in 2021, bringing in ~$25B in cash as well as ~$5B worth of AerCap stock which was sold off subsequently. From 2020 on GE also sold its remaining stake in OFS provider Baker Hughes (BKR) which it had created in 2017 by merging its existing O&G business with Baker. Total proceeds from the divestment which was completed in early FY23 were around $11.6B.

GE Timeline under CEO Culp (Company Filings)

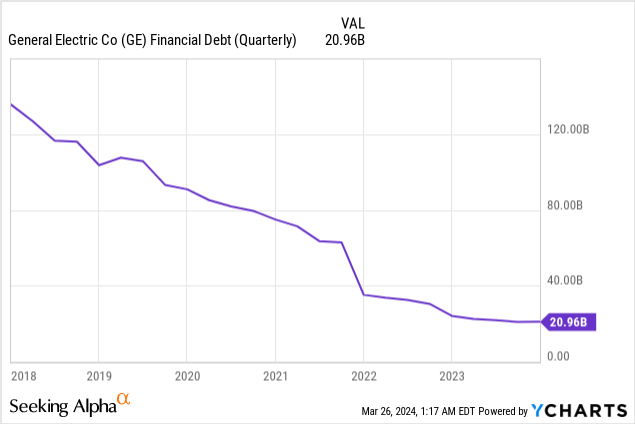

Alongside those external cash inflows, GE also made significant internal progress with FCF improving from negative when Culp took over to a combined $6.6B in 2021 and 2022, enabling further deleveraging. Another significant part in achieving further debt paydowns was Culp’s bold decision to slash GE’s dividend from 12¢ to 1¢/share. Over the years it is estimated that this freed up around $30B in cash, greatly needed to aid the company’s deleveraging efforts. Through all those measures Culp was able to reduce GE’s debt from ~$130B at YE17 to ~$21B as of YE23, a reduction of almost 85%.

Having opposed the plan previously in favor of deleveraging and simplifying, in late 2021 Culp announced that GE with its fully transformed debt profile was finally ready to undertake its intended split into three separate enterprises: GE Healthcare, GE Vernova and GE Aerospace (then named GE Aviation). On January 3, 2023 GE completed the spin-off of 80.1% of GE Healthcare, holding a remaining stake of 19.9% which was over time reduced to stand at ~13.5% by YE23 with Culp aiming to fully exit the investment over the coming years.

Following the successful spin-off of GE Healthcare, the company announced the further spin-off of GE’s power and renewable energy division (GE Vernova) to be launched in April 2024. On April 2, 2024 before New York market open the company spun-off 100% of Vernova’s share capital at an exchange rate of 1 new share per 4 existing GE shares with Vernova ending its first trading day at a total market capitalization of ~$37B. With Vernova fully spun-off and the remaining stake in Healthcare to be exited subsequently, the remaining General Electric changed its name to GE Aerospace, assuming GE’s legal status and all of its outstanding financial debt as well as $13B in cash.

Proven razor-blade model with largest installed base and rollout of next-gen engines provide earnings visibility for decades. As of 2024, GE Aerospace has the largest installed base across commercial and military aviation propulsion systems with ~70k engines of which ~44k are large-scale commercial with just the narrowbody CFM56/LEAP at ~26k. At ~85k, P&W does have a larger installed base overall, however the majority of this is contributed by smaller regional and turboprop engines with only ~12k large commercial engines currently in service. Given its skew towards the widebody end market Rolls-Royce ranks lowest among the big three on installed engine base with ~6k.

Across the entire commercial market of narrow- and widebodies, GE is estimated to hold a dominant ~55% market share, surpassing P&W and RR combined which are seen at ~26% and ~18% market shares respectively. I view this dominance on installed base as a significant competitive advantage for GE given the engine manufacturing’s industry characteristics to operate less like traditional one-time sale manufacturing but more akin to a service industry with MRO and spare parts contributing most of profits.

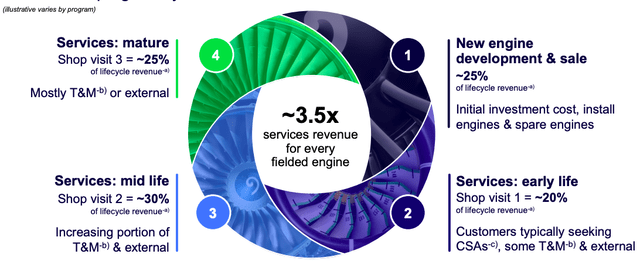

The engine, and with it most of the Aerospace manufacturing industry is characterized by long product lifecycles with the majority of revenues not coming at initial delivery but from consequent servicing and maintenance (aftermarket). As such, profitability of new products which have just began to be rolled-out often remains in the red for years until higher margin service and aftermarket revenues offset initial losses and generate a high degree of predictable and stable earnings for decades (CFM56 began its service in 1982).

Across its major engine families, GE estimates that only ~25% of sales come from OE with the remainder constituted of aftermarket sales. At typically 3 shop visits or maintenance overhauls across the engine’s lifecycle, revenues and profits typically increase over time implying a profitability and revenue generation sweetspot towards the back end of the engine’s maturity curve.

GE Typical Engine Lifecycle (GE IR)

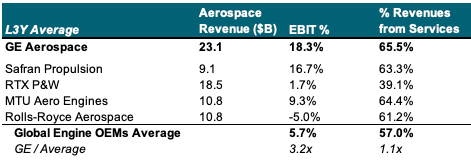

Compared to peers, GE has a highly favorable % of revenue derived from those services. Over the last 3 years, MRO and spare parts contributed ~66% to GE’s total revenues. This significantly benefitted margins vs competitors which on average only generated ~55% of revenues from services with Pratt & Whitney at the low end at with ~39% service revenue.

Bloomberg

With both the top-selling CFM56 (~19k installed) and its current-gen widebody options GE90 and CF6 (~7.2k installed) in or near maturity stage, I see GE in an excellent position to capitalize on growing profitability in ramping-up aftermarket sales while OE sales increasingly shift to the next-gen programs. Especially the CFM56, developed in partnership with French Safran, has also been a benefactor of recent issues at Pratt & Whitney and the overall extended life times of older aircraft (and engines) with latest departure forecasts implying higher utilization in the near term.

CFM56 Departures Forecast (GE IR)

With ~45% of installed CFM56 base also not having seen any shop visit and therefore being at the beginning of their lifecycle curve, shop visit frequency for the program should remain roughly stable through the decade with GE also estimating a near term ramp-up in MRO demand.

CFM56 Shop Visits Forecasts (GE IR)

With its current-gen engines approaching their profitability sweetspot, GE is in an excellent position to focus on the rollout of the next generation. In the narrowbody end markets this is the LEAP engine, aimed at replacing the aging CFM56 by offering ~15% higher fuel efficiency on the A320neo and B737MAX platforms. In the widebody segment, GE is currently transitioning its aging CF6 and GE90 engines towards the GEnx and GE9X which both offer 10-15% fuel savings with the latter being exclusively produced for the B777X.

GE IR

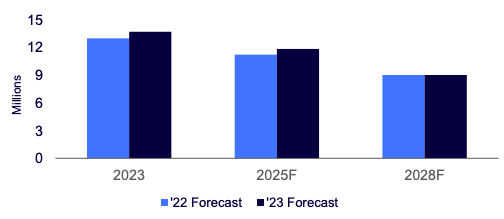

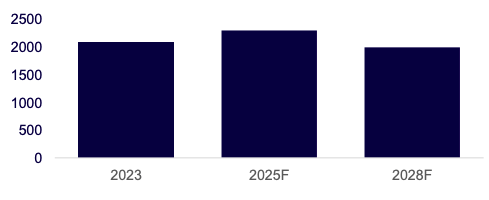

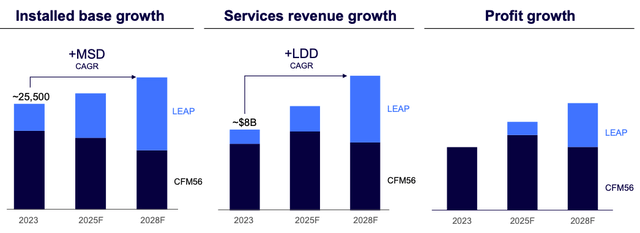

Across the narrowbody segment, installed base is expected to grow at MSD throughout the decade with LEAP deliveries ramping up more than 100% by 2028 to constitute roughly 50% of installed base at ~15k. With shop visit 1 coming in for the LEAP and the CFM56 in its lifecycle sweetspot, MRO and spare parts revenues are estimated to grow at LDD through 2028 with the LEAP reaching 50% of total by 2028. Driven by a strong near term OE outlook with ~1.1k LEAPs ordered in Q4 23 alone (Book-to-Bill: ~2.7), overall revenues from the program are expected to exceed those of the CFM56 by 2026.

Profits generated from the LEAP are also expected to ramp up significantly through the decade, breaking even by 2024. By 2030 GE estimates that the LEAP will have surpassed its predecessor after more than doubling profits between 2025 and 2028. Key drivers to profit growth will be both external in higher servicing sales share vs OE and internal in increased production efficiencies leading to better metrics such as realized time-on-wing.

GE IR

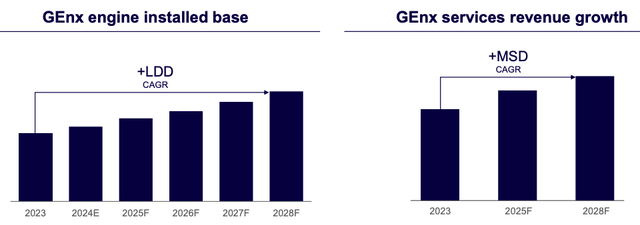

The widebody option GEnx is also expected to grow significantly through the decade with installed base projected at a LDD CAGR to 2028. With increasing maturity and further rollout, profitability is estimated to grow with service revenues growing at MSD from 2023 to 2028.

GE IR

Alongside the GEnx, the GE9X, the company’s other next-gen widebody option is also on a strong growth trajectory with ~900 engines on order and expected profitability breakeven by 2030 while the current-gen GE90 and CF6 engines will continue to generate a long tail of servicing revenues well into the 2030s.

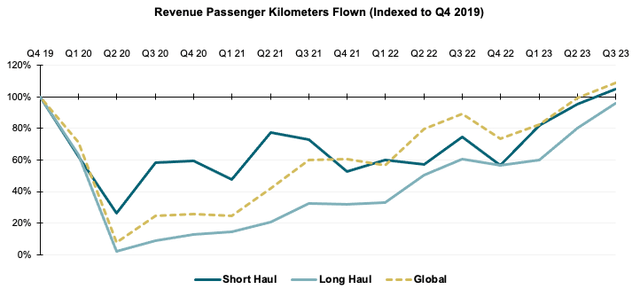

Industry outlook remains highly favorable with ongoing rebound in air traffic and record backlogs at aircraft OEMs. After the initial shock from Covid-19 which cut global air traffic to almost zero, the industry has experienced a strong rebound in activity, led by short haul flights at first and recently joined by long haul. Overall global revenue passenger kilometers flown (“RPM”), the key measure of air travel demand, have first exceeded pre-Covid levels during Q2 23, led by strong US domestic demand while European and Asian short haul remains weaker. Long haul demand, consisting of international i.e. transatlantic and transpacific flights has not fully reached pre-Covid status yet but can be expected to catch up later this year.

Bloomberg, IATA

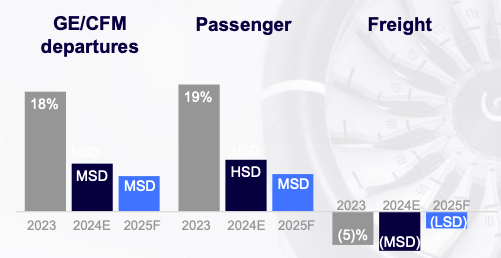

With only pre-Covid levels reached and still at a gap to implied long term GDP+ demand growth, I estimate the current Aerospace upcycle can continue in the near and mid term. GE management expects MSD growth in CFM-powered fleet departures through 25E, driven further by passenger demand which is projected at HSD and MSD while freight, although a smaller component of GE’s addressable market, is likely to come near recovery by 25E.

GE IR

With record growth in demand against continued supply chain challenges, backlogs for the major aircraft OEMs have also skyrocketed in recent quarters, further providing GE with high earnings visibility as Airbus and Boeing feed through their backlog.

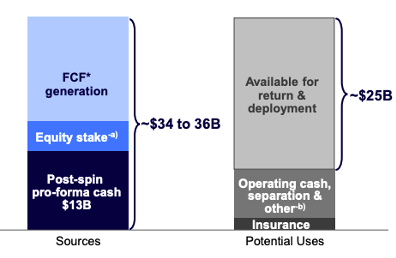

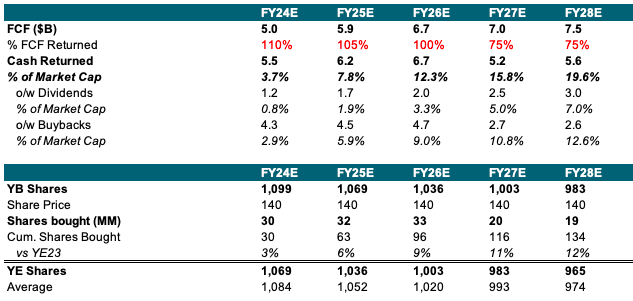

Management is committed to grow shareholder distributions at >100% of excess FCF, retiring ~9% of shares by YE26. During the March 7 Investor Day, CEO Larry Culp laid out his capital allocation framework for the new entity, notably aiming to return >100% of FCF through 26E (~70-75% of currently available funds) to shareholders. In total GE aims to have ~$25B of cash available to deploy through 26E, made up of the new entity’s sizeable FCF generation, further monetization of its GEHC stake and the post-spin cash position of $13B.

GE IR

At an initial payout ratio at ~30% of net income, I expect a starting dividend of $1.15 per share for a yield of 0.8% at current share price. Management has further reached a share buyback authorization of $15B which I estimate to be fully completed by YE26, potentially retiring up to 9% of current shares outstanding, providing a further boost to Earnings and FCF per share beyond organic growth and operational improvements. Overall I see GE returning more than 12% of its current market cap to shareholders in the coming years, highlighting its strong value proposition for investors.

GE Cash Returns (Company Filings, WSR Estimates)

With GE Aerospace assuming all currently held debt, I estimate a total post-spin net debt of ~$10B based on pro-forma cash of $13B and gross debt of $23B. With 24E EBITDA at ~$7.5B, I see net leverage of 1.3x, putting GE in a strong financial position to remain its investment grade credit rating. Beyond some maturities due in 2024, debt repayment will therefore not be a focus in the new company’s cash allocation. M&A will further not be a priority with management noting that any potential deal would likely be small in size and have to have significant strategic, operational and financial synergies.

Valuation

Financial Model

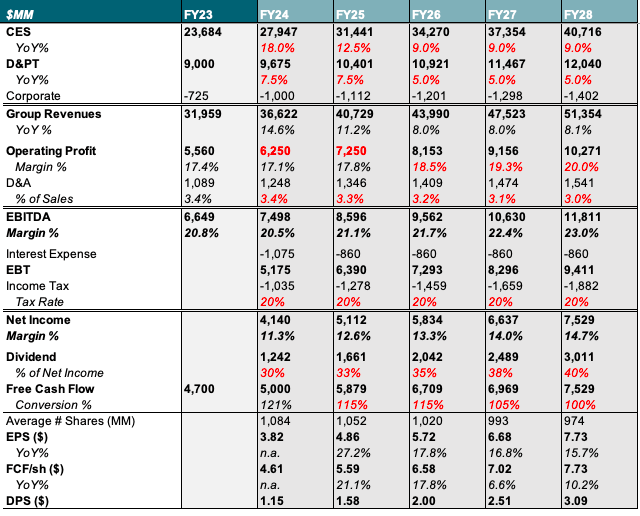

Forecasting GE financials I rely largely on management guidance as provided during the Investor Day. For the CES segment I model 18% and 12.5% YoY growth for 24E and 25E after which I expect a growth rate in the HSD at 9%. For DP&T I estimate growth rates at 7.5% through 25E after which I model a decrease to 5% annually. Coupled with corporate eliminations I see a total annual topline growth of 15%/11%/8% respectively for 24E/25E/26-28E.

GE guided for 24E and 25E operating profit in the $6-6.5B and $7-7.5B ranges for which I currently estimate the midpoint. Following an initial decline in margins as the LEAP engine OE rollout lowers share of aftermarket and services, I estimate margins to reexpand towards ~20% for a 28E operating profit of $10.3B, in line with management target to reach $10B by 28E. With D&A trending towards guided capex at 3% of sales, I estimate total EBITDA margins to grow from 20.8% as of FY23 to ~23% in 28E.

For FCF I model a 115% Net Income/FCF conversion rate for 24E and 25E, after which I see a decrease towards a stable 100% as initial working capital effects subside. Benefitted further by a significant reduction in share count through buybacks I see an overall EPS growth CAGR of ~15% through 28E and a ~11% CAGR for FCF/share.

GE Financial Model (Company Filings, WSR Estimates)

Valuation

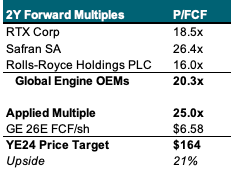

I value GE based on a peer-derived 2Y forward multiple on my 26E FCF/share, leading to a price target as of YE24.

GE’s key engine OEM peers currently trade at a 2Y forward P/FCF multiple of 20.3x with Safran at 26x and Rolls Royce as low as 16x. I exclude MTU due to its currently extremely discounted valuation on the back of its exposure to the GTF powder metal issues which is even more significant than RTX’.

I assign a 25% premium to engine OEM peers to reflect GE’s leading installed base, margins and highly favorable shareholder return outlook for a target multiple of ~25x. I note that this is slightly below Safran’s standalone multiple, which I believe is appropriate to account for GE’s comparably lower exposure to the highly profitable CFM engine programs and its less profitable and growing defense franchise.

Applying a 25x multiple on my 26E FCF/sh of $6.58 results in a price target of $164 as of YE24, implying ~21% upside potential from current levels.

Company Filings, WSR Estimates

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here