Intro

On the most recent Q4 earnings call, Markforged (NYSE:MKFG) CEO gave some upbeat comments regarding the trajectory of Markforged as a whole. This company operates in the additive 3D manufacturing space where the company’s cloud-based AI-powered platform (Digital Forge) facilitates seamless connectivity between materials & software resulting in laser-fast manufacturing results. The CEO’s clear message to investors was that by investing aggressively today, Markforged has the capability to generate outsized returns going forward.

Unfortunately, post the announcement of the company’s fourth-quarter earnings (Where the negative EPS of $0.07 actually beat expectations), the market was not as enthused with management’s optimism. In fact, the company has lost over 30% of its market cap over the past five weeks alone. As a result, shares have now dropped well below $1 a share and trade with a present market cap of $171.58 million.

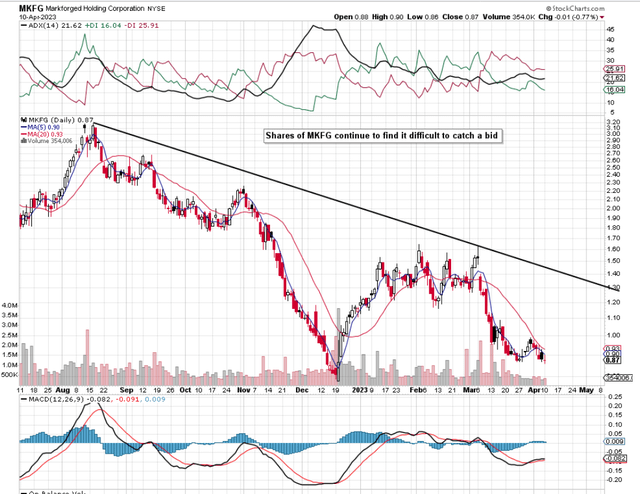

Although short interest in the stock has remained around the 5% mark, we can see below on the technical chart that the stock continues to print lower lows which is obviously worrying. Bulls will be hoping that the recent December’22 lows can hold here but this remains to be seen.

Management though as mentioned remains bullish on how its Digital Force platform can shake things up in the manufacturing space going forward. Furthermore, the absence of any significant debt on the balance sheet as well as the company’s robust pipeline all point to strong fundamentals and the willingness to literally ride this out until the company can finally become profitable.

In saying this, management stated that it does not expect the company to become profitable until Q4 in fiscal 2024 and this will only be on a non-GAAP earnings basis. This begs the question of whether the company’s sustained cash-flow burn will be enough to keep the market interested in the interim period.

Suffice it to say, over the short-term, to settle the ship so to speak, we need to see stability in the following two areas to ensure shares of Markforged do not fall any further from their current levels.

MKFG Technical Chart (Stockchrts.com)

Gross Margin

Although management has taken close to $20 million out of its cost structure since the second quarter of last year, we saw the company’s gross margin drop to 47.5% in Q4. This was a sizable drop compared to the same quarter 12 months prior (57.6%) and warrants attention. The reason being is that although sales grew in the quarter, higher-than-expected costs from the recent commercialization of the FX20 led to a negative operating profit print of $19.3 million and a negative operating cash flow of $8.2 million for the quarter. Suffice it to say, although costs may be moving in the right direction, there remains a long road ahead to positive profitability.

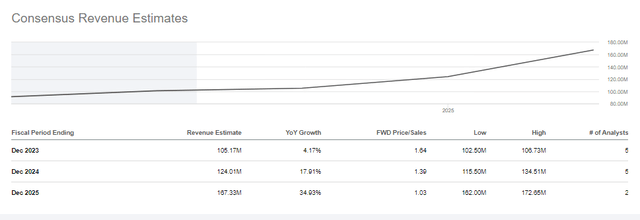

Therefore, with sustained cost-cutting measures needing to remain fully on the agenda in fiscal 2023 and beyond, it will be interesting to see whether the company can keep on growing its sales aggressively in this aggressive cost-cutting environment. Although just over 4% top-line growth is expected in fiscal 2023, analysts who cover Markforged are predicting over 17% growth in fiscal 2024. These numbers will at least be needed in order to keep the market interested as cost-cutting as we know has a finite life. Top-line growth on the other hand has an unlimited ceiling.

MKFG Forward-Looking Sales Numbers (Seeking Alpha)

Growth

From a growth standpoint, the CEO went into the bullish fundamentals of the “Digital Forge” and how manufacturers continue to leverage the platform. It is evident here that as the value of Markforged offerings continues to improve, more customers are beginning to leverage the technology. Trends from the recent incorporation of 2022 acquisitions (Tetan Simulation & Digital Metal) already point to more value being added which will result in higher revenues (Most likely recurring revenues on the Tetan Simulation side).

Given how quickly this industry is changing, we believe more M&A will be needed for Markforged to stay ahead of the curve (Which will keep the cash-flow burn elevated over the near term). Therefore managing working capital on the balance sheet will be key to ensuring the balance sheet can be protected to the best of the company’s ability.

Conclusion

Markforged’s strong balance sheet and growing sales are encouraging trends in this beaten-down play. Management continues its relentless mission of bringing down costs as much as possible while at the same time investing heavily in the company. The market though needs to see more evidence that profitability is on the way. Let’s see what Q1 brings. We look forward to continued coverage.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here