")

I last mentioned The Mosaic Company (NYSE:MOS) in November here, as having the potential to witness better product pricing and sales during the upcoming North American crop planting season. While the usual seasonal bottoming pattern in Mosaic’s stock price did exactly play out, the -20% quote decline into June has opened a whole new level of “value” for long-term investors.

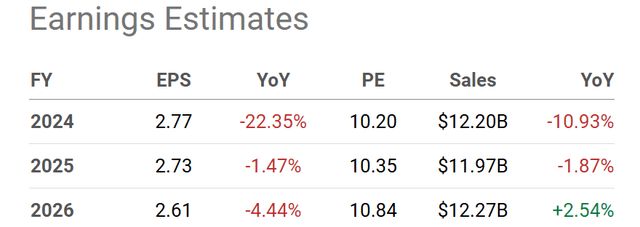

Based on a large variety of raw statistics, MOS may now be one of the cheapest larger capitalization agriculture-related names focused on grains/crops you can own in June 2024. And, after a steady -65% price drop from the first part of 2022, few on Wall Street are seriously recommending a position or pushing the idea of a significant upturn in operations. You can review the lackluster business growth forecast by analysts below.

Seeking Alpha Table – Mosaic, Analyst Estimates for 2024-26, Made June 7th, 2024

What this means is Mosaic may have an enviable and rare combination of long-term value and reversing contrarian sentiment to build upon the remainder of this year and all of next. Let me explain its value and classic turnaround proposition for new investment.

Top Value Pick in Ag-Related Sectors?

Headquartered in Florida, Mosaic produces and markets concentrated phosphate and potash crop nutrients, mostly in the U.S., Canada, and Brazil. As main ingredients for higher crop yields, business performance typically follows the health of farm income levels (tied to grain prices). In addition, supply disruptions for fertilizers like witnessed during the early 2022 Russian invasion of Ukraine can/will affect Mosaic’s fortunes.

Market-size volume growth for both phosphate and potash are expected to be in the 3% range annually into 2030. Demand is being pulled by rising population globally, expanding food consumption per capita, shrinking arable land available to plant crops (from climate change and commercial/housing development), general economic growth, favorable government tax incentives, plus hotter and dryer weather conditions in many parts of the world, as the main drivers. Essentially, with fewer acres available for farming, fertilizers are becoming more critical each year to feed the planet.

The interesting part of the investment equation today is expectations for the fertilizer marketplace are very muted to bearish by market players. As a consequence, still solid sales/income performance by Mosaic is being given an exceptionally low valuation.

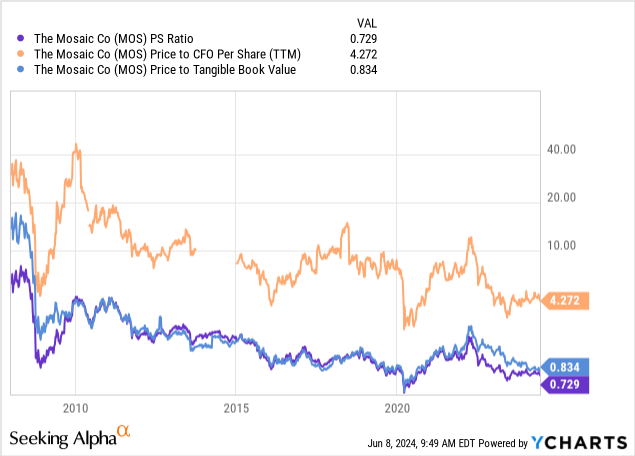

On price to sales, cash flow, and tangible book value since 2008, only the 2020 pandemic experience (with a stock price implosion over six months) delivered a lower valuation on trailing 12-month results than today. Believe it or not, 0.73x sales, 4.3x cash flow, and 0.83x tangible book value are a good 50% discount to “average” ratios experienced over the last 16 years.

YCharts – Mosaic, Price to Trailing Fundamentals, Since 2008

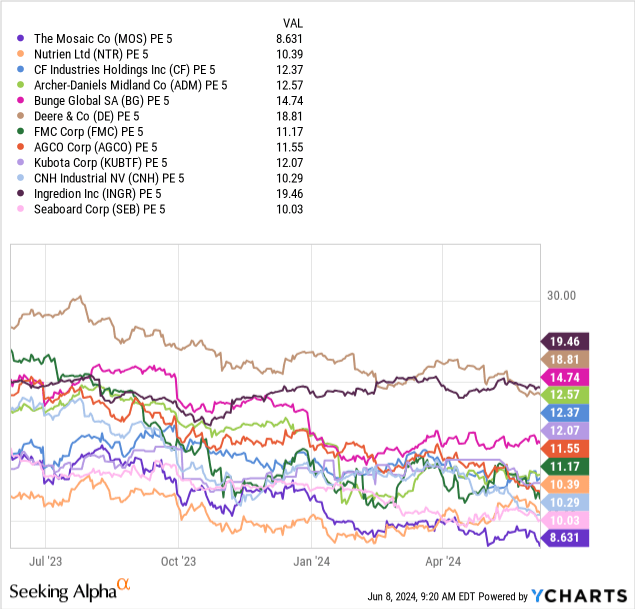

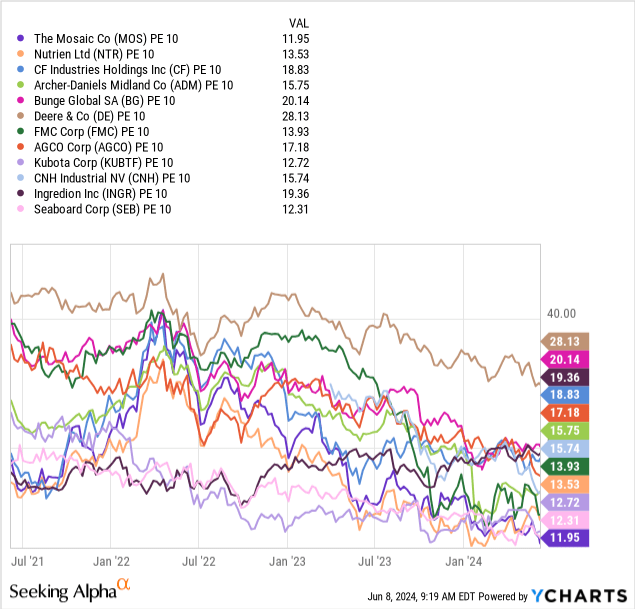

Another interesting idea to munch on is Mosaic’s “long-term” earnings generation has become quite cheap to own. It is actually the lowest ag-related P/E setup in the large-cap space of Wall Street trading. Using the current price divided by average earnings over many years, Mosaic appears to be less expensive than direct competitors Nutrien (NTR) and CF Industries (CF), or grain-economy peers Archer-Daniels Midland (ADM), Bunge Global (SA), Deere & Co. (DE), FMC Corp. (FMC), AGCO (AGCO), CNH Industrial (CNH), Ingredion (INGR), and Seaboard (SEB). Mosaic’s PE 5-year number of 8.6x is a rough 30% discount vs. the group median average. Just recently, MOS fell to the lowest PE 10-year (economic cycle-adjusted) reading out of the group, now sitting at 11.9x, which is a 25% discount to the current median average.

YCharts – Mosaic vs. Large-Cap Grain-Related Names, PE 5, Over 1 Year YCharts – Mosaic vs. Large-Cap Grain-Related Names, PE 10, Over 3 Years

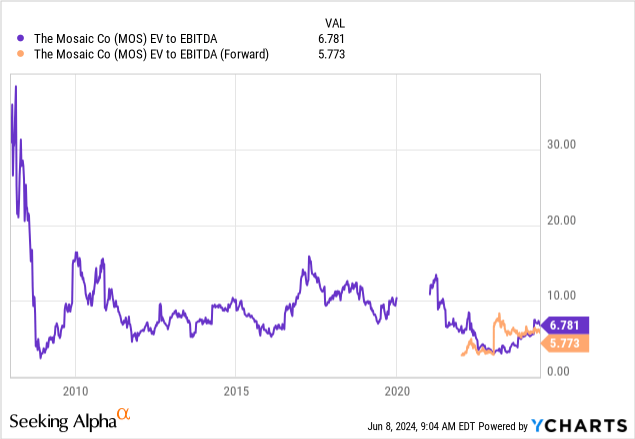

When we take into account changing debt and cash levels, the enterprise value to EBITDA multiple is also incredibly attractive, with a trailing EV ratio of 6.8x and forward estimated 5.8x multiple. Reviewing a long-term average closer to 10x, if business trends hold up over the next year, today’s 40% discount to historical readings is worth a serious look.

YCharts – Mosaic, EV to EBITDA, Since 2008

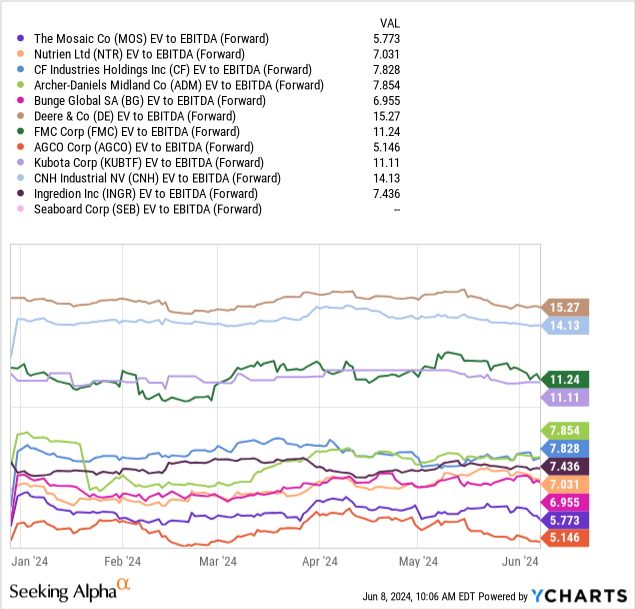

On a forward-looking basis, Mosaic’s 5.8x EV to EBITDA calculation is the lowest in the group outside of farm equipment maker AGCO. This ratio is also a 25% discount to peers. (Note: Seaboard has little to no analyst coverage right now.)

YCharts – Mosaic vs. Large-Cap Grain-Related Names, EV to Forward EBITDA Estimates, YTD 2024

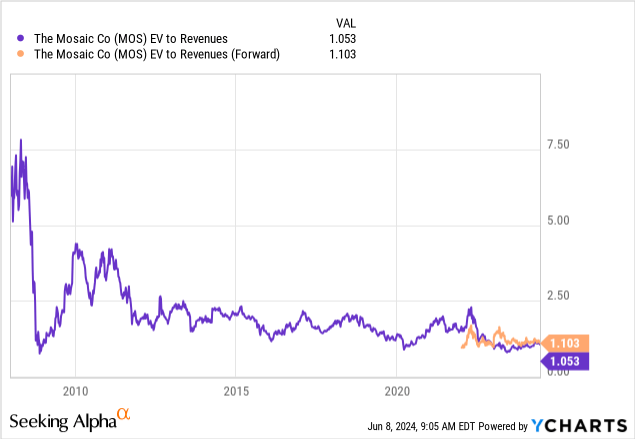

The clearest bargain valuation datapoint may be the EV to Revenue ratio. Ignoring the latest income and profitability results, to just focus on sustainable revenue production can be the easiest barebones way to review company worth over many decades. Well, the current 1.05x to 1.10x setup for total company value (including debt) vs. sales is a 55% discount to long-term averages back to 2008. It’s cheaper than the 2020 pandemic low and just off the modern-record bargain level outlined during the 2008-09 recession. The readout is plenty of runway exists for share price gains.

YCharts – Mosaic, EV to Revenue, Since 2008

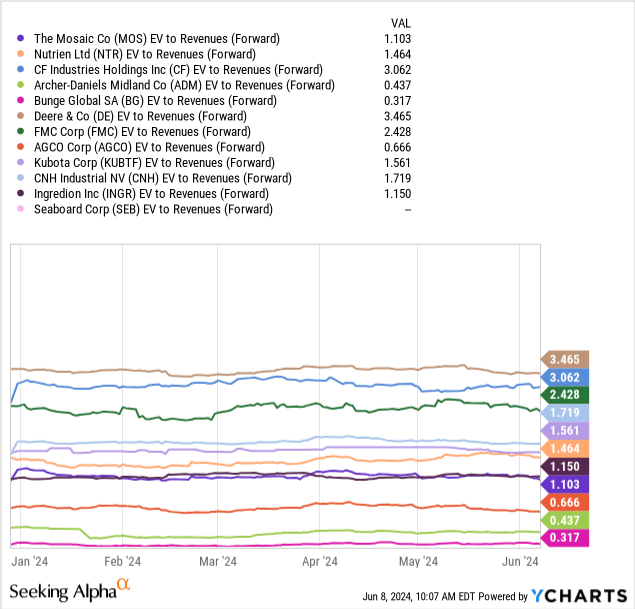

While peer comparisons do not show the same undervaluation extreme, Mosaic’s forward 1.1x ratio is still in the bottom half of grain-related companies and a 30% discount to the median average.

YCharts – Mosaic vs. Large-Cap Grain-Related Names, EV to Forward Revenue Estimates, YTD 2024

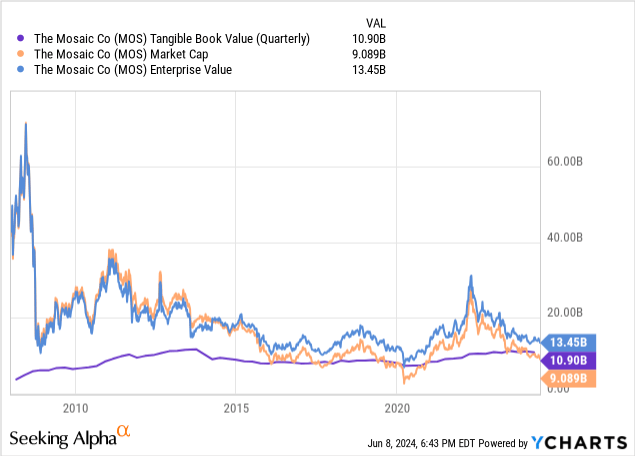

As a function of tangible book value, Mosaic’s equity market capitalization and enterprise value are approaching the lows that have proved a bottoming area for share price over the past decade.

YCharts – Mosaic, Tangible BV vs. Market Cap & Enterprise Value, Since 2008

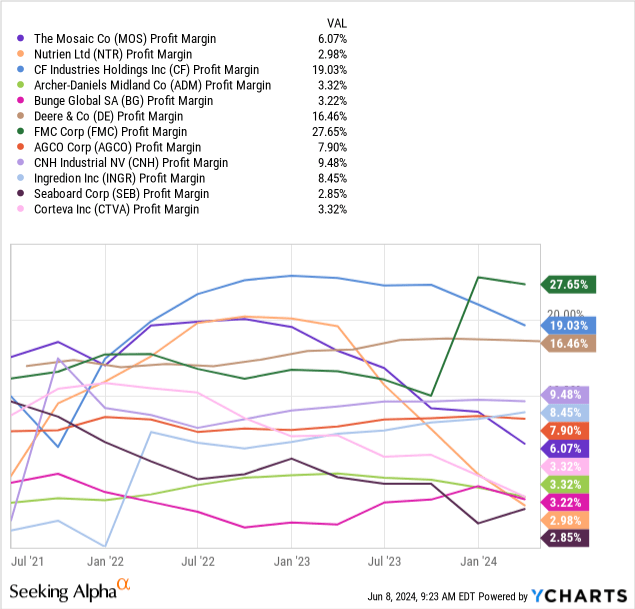

You would think Wall Street is throwing Mosaic under the bus because of low profit margins. That would make logical sense to me. However, profit margins were leading the group in late 2021, while they remain in the middle of the pack during 2024.

YCharts – Mosaic vs. Large-Cap Grain-Related Names, Profit Margins, 3 Years

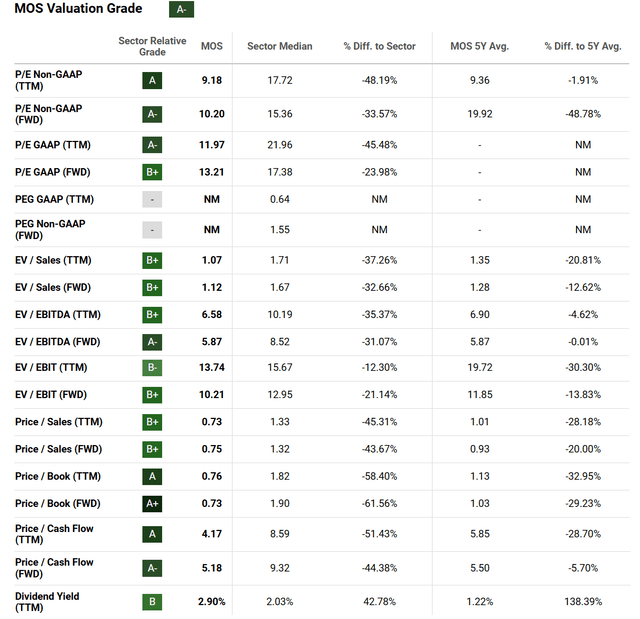

Seeking Alpha’s own computer-algorithm ranking system puts an “A-” Quant Valuation Grade on Mosaic presently. When compared to its 5-year history and current sector median scores on a variety of operating metrics, Mosaic appears to have considerable upside for investors.

Seeking Alpha Table – Mosaic, Quant Valuation Grade, June 7th, 2024

Final Thoughts

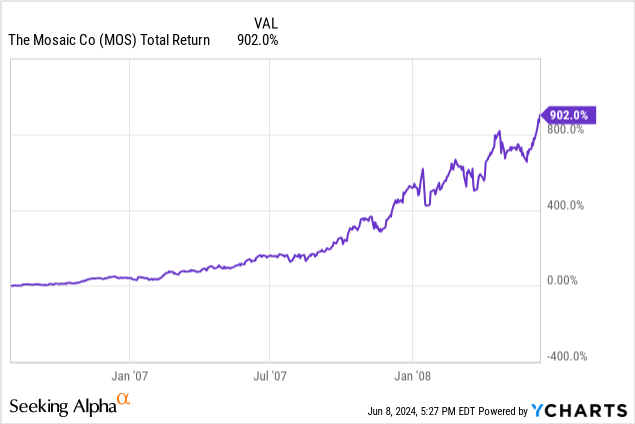

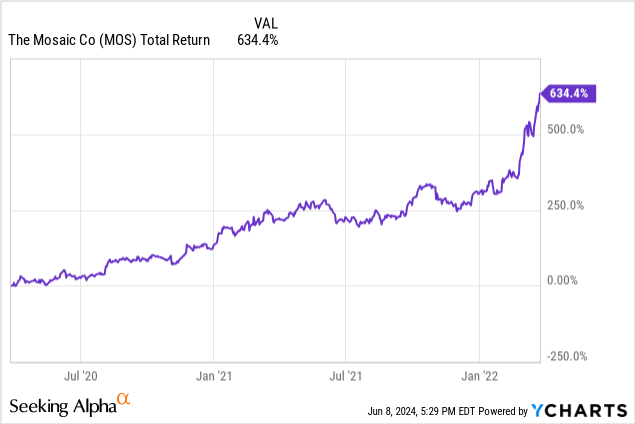

Starting from a low valuation base, with little growth expected from the underlying business, does support a bullish view for share pricing over time. Mosaic’s fertilizer business can be cyclical, but the real-world payoffs for investors purchasing shares near a cycle bottom can be quite extraordinary. For example, between August 2006 and June 2008, MOS achieved a total return of +902%. Between the end of March 2020 and March 2022, shares gained +635% for owners.

YCharts – Mosaic, Total Returns, August 2006 to June 2008 YCharts – Mosaic, Total Returns, End of March 2020 to March 2022

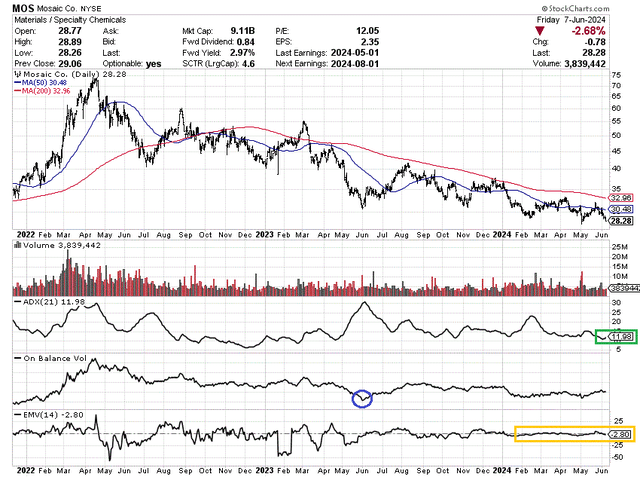

The technical momentum picture has been improving, although it’s been painstakingly slow. Below is a 30-month chart of daily price and volume trading. The 21-day Average Directional Index score under 12 (boxed in green) is the lowest volatility reading since late 2022. I like to use ADX to identify a bottoming pattern ready for reversal. On Balance Volume reached a low in May 2023 (circled in blue). And, the 14-day Ease of Movement indicator has flatlined throughout 2024 (boxed in gold), which signals a very balanced supply/demand situation, void of aggressive selling.

StockCharts.com – Mosaic, 30 Months of Daily Price & Volume Changes, Author Reference Points

That’s not to say Mosaic cannot fall another -20% or -30% first, before a multi-year upturn begins. If grain prices move in reverse and a global recession is next, the stock quote will likely go nowhere fast.

Although grain prices are relatively uncorrelated assets to recessions and stock market swings, falling consumer incomes could dent food demand on the fringes and cause a lower valuation re-rating of Mosaic (at least for a short period of time).

On top of recession fears, the phosphate and potash markets do appear to be well supplied at the moment, while prices have come down dramatically from early 2022 peaks. If fertilizer markets witness lower-than-expected demand from farmers into 2025, a surplus of phosphate and potash could hold Mosaic’s business results and share price in check for several years.

However, if you believe like I do, food inflation will resume its torrid pace soon (from governments around the world printing fiat money to finance oversized debts), why not own some farm and grain-related investments? Follow my logic: if grains rise sharply in price (climate change could goose the advance if droughts create low yields and failed crops), farmers will be flush with extra cash/income, while both the funding and profit-incentive to increase fertilizer usage could push supply/demand dynamics back into shortage.

My investment conclusion is Mosaic may be positioned in a reduced risk, high potential reward environment under $30 per share during June 2024. I rate shares a Buy, and own a small position in my portfolio.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Read the full article here

")

Q3 2025 Earnings Call Transcript")

")

")