PriceSmart (NASDAQ:PSMT) was founded in 1996 in California with the intention of bringing U.S.-style warehouse club shopping experiences, similar to those of Sam’s Club, BJ’s (BJ), and Costco (COST), to emerging and developing countries.

At present, their operations span 50 warehouse clubs in 12 countries and one U.S. territory within Central America, the Caribbean, and Colombia.

The business benefits from a competitive moat in that they do not currently face direct competition from U.S. membership warehouse club operators in their markets. While they do face significant competition from various local and international entities, their long operating history and current scale provides them with an outsized advantage.

For example, the company currently boasts of total memberships approximating 1.8M. And in the trailing twelve-month period ended February 28, 2023, the company generated +$4.2B in total revenues.

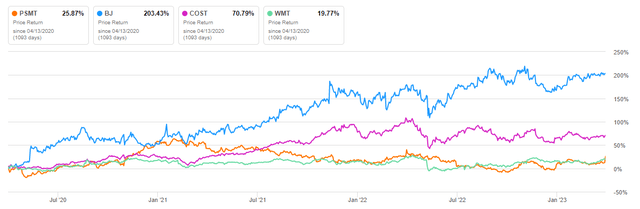

Over a three-year period, PSMT has consistently trailed their U.S.-focused club operators by wide margins in delivering total returns, but they have outperformed more diversified retailers, such as Walmart (WMT).

Seeking Alpha – 3-Yr Returns Of PSMT Compared To Related Peers

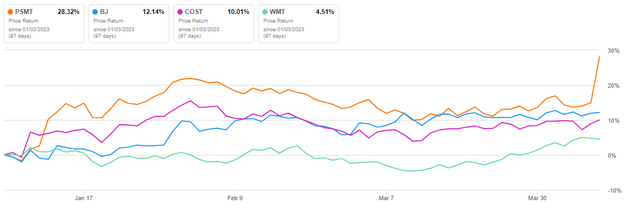

And on a YTD basis, the company has significantly outperformed. Though it is worth noting shares received a sizeable boost following the release of their Q2 earnings results, which surprised to the upside.

Seeking Alpha – YTD Returns Of PSMT Compared To Related Peers

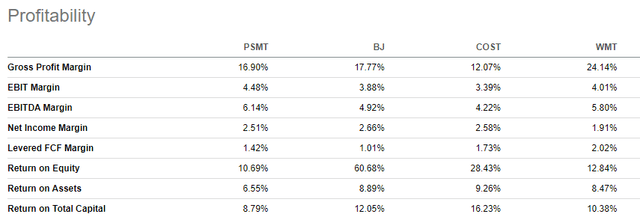

Another point that warrants attention is their profitability. Despite operating at a fraction of the size of their larger counterparts, the company still generates comparable margins.

Seeking Alpha – Profitability Metrics Of PSMT Compared To Related Peers

Following recently released results, shares are trading near the top of their 52-week range. Though shares trade at a discount to their larger U.S-based warehouse peers, current valuations are generally in-line with five-year averages and consensus Wall Street estimates. An expected decline in margins in the coming quarters also invites a pause on new initiation. While the stock is an interesting watch, I don’t view it as a “screaming buy” at this point in time.

Strong Net Merchandise Sales Growth

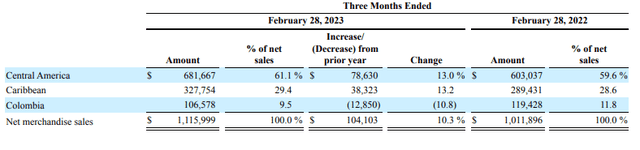

In Q2 of fiscal 2023, total net merchandise sales increased 10.3%, led by strong gains in both their Central American and Caribbean segments, which, together, account for about 90% of their total net sales.

Sales in both regions were up 13% from the same period last year. Contributing to overall sales growth was a 3.8% increase in transactions and a 6.2% increase in average sales ticket, which represents the amount their members spend on each visit or online order. While transactions were up, average items per basket were down 3.3% during the quarter. This came as average prices increased 9.7%.

Q2FY23 Form 10-Q – Comparative Summary Of Quarterly Net Merchandise Sales

Partially offsetting the gains in Central America and the Caribbean region was weakness in their Colombian market. Total net sales here declined 10.8%, due principally to a significant devaluation in the Colombian peso during the fiscal year. For the quarter, currency fluctuations in the region had a 18.1% negative impact on net merchandise sales, bringing the negative impact on the year to 19.3%.

Expanding Margins

For the quarter, total gross margins on net merchandise sales expanded 40 basis points (“bps”) to 16%, due primarily to general improvement across all sales categories, but particularly from their other business services, such as their food services and bakery.

The higher gross margins led to an expansion in total gross revenue margins, which includes net merchandise sales and all other revenues, of 30bps to 17.3%.

Headwinds In The Colombian Market

Looking ahead, management is expecting lower total gross margins for both the third and fourth fiscal quarters of 2023. The decrease is due in part to the elimination/reduction of both their COVID and Trinidad foreign currency exchange premiums.

Additionally, margins are expected to be negatively impacted in their Colombian market due to their strategic decision not to increase the sales price on select items on which their costs have increased.

The decision to forgo passing through their costs relates to their efforts to reduce the cost burden for their Members, all of whom are experiencing both inflationary pressures, as well significant devaluation in their local currency.

Post-Earnings Insights

PSMT launched nearly 12% higher following their fiscal Q2 earnings release that beat on both earnings and revenue by $0.13/share and +$10M, respectively. Finer details within the release also added to investor enthusiasm.

Total member accounts grew 3.2% versus the prior year, bringing their total accounts to nearly 1.8M. And looking ahead, PSMT has four warehouse clubs under construction or in preparation for opening. Upon completion, I can see total accounts eventually surpassing the 2.0M mark.

Their balance sheet and cash flow position are also supportive of their expansion plans. Through six months of the fiscal year, for example, the company has generated over +$60M of free cash flow or about +$44M on a retained basis, after accounting for dividends and repurchases. In addition, they have +$260M in cash on hand and operate on a lighter debt load.

Margins also remain robust. Trailing twelve-month operating and revenue margins, for example, presently stand at 4.3% and 16.9%, respectively. In 2019, by comparison, they were operating at 3.6% and 16.4%. While they’ve experienced pressure in their Columbian market, the weakness has been more than offset by strength in their Central American and Caribbean markets.

In terms of profitability, PSMT operates comparably to BJ. And in some metrics, such as EBITDA margins, PSMT tends to outperform. Despite the similarities, PSMT trades several notches below their peers. Their EV/EBITDA multiple, for example, presently stands at about 9x. This compares to a 12x range for both BJ and WMT and 20x for COST.

I view the discount as appropriate, however. Though their geographic concentration in emerging and developing markets presents upside opportunity, it also exposes them to unique risks that can be significant.

Political instability, for example, is an ever-present risk that the company must navigate through. In the third quarter of fiscal 2021, for example, civil unrest in Colombia significantly impacted the country’s infrastructure. And there were similar levels of unrest in Nicaragua and Honduras in 2019, as well as in Costa Rica in 2018.

Currency fluctuations are another thorn that PSMT must consistently address. While they’ve done so successfully thus far, there are signs the company needs to take a step back. In the past, the company would raise local prices to maintain their targeted margins in response to currency devaluation.

But, as was mentioned in the current release, there’s a limit to how much their Members could absorb, as in the case in their Colombian market, which is expected to experience margin compression in the quarters ahead due to PSMT’s strategic decision to pause their passthroughs.

I, therefore, view shares as fairly valued at current trading levels in light of these considerations. While shares are worth continued monitoring, I am maintaining a “hold” position on the stock.

Read the full article here