Introduction And Thesis

Reynolds Consumer Products Inc. (NASDAQ:REYN) is a leading consumer goods company known for its innovative and sustainable solutions. The company is recognized for its iconic brands like Reynolds Wrap and Hefty, offering a wide range of products including food storage, aluminum foil, and disposable tableware.

REYN has a leading commercial position across a number of segments in the US market, allowing it to generate consistent demand and maintain its position through retail relationships.

The concerns we have are around the execution of its recovery strategy, as Management seeks to maintain growth while improving margins. Competition will make this difficult, as will its elastic nature, as evidenced by recent demand.

We suggest investors remain patient for further improvement before considering REYN.

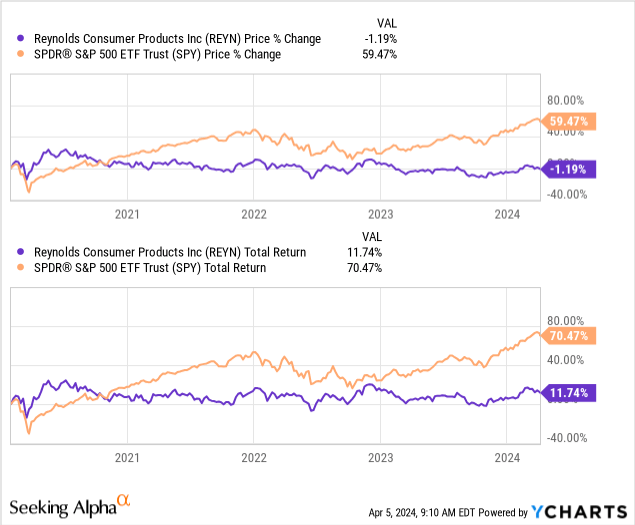

Share Price

REYN’s share price performance has been mediocre since the business was listed, although appreciating that it was impacted by the pandemic, subsequent revival and now the current weaker macroeconomic environment.

Financial Analysis

Capital IQ

Presented above are REYN’s financial results.

Business Model

REYN has an extensive range of products that include aluminum foil, plastic wrap, parchment paper, and disposable plates. It operates across a range of well-known brands like Reynolds Wrap, Hefty, and Pan Lining Paper.

A staggering 95% of US households have at least 1 REYN product, while the company is the #1 or #2 player in the majority of its product categories (Source: Management).

Its strong brand has been developed through a combination of:

- Distribution: REYN has an unrivaled presence in various distribution channels like supermarkets, online retailers, and mass merchandisers. For many consumers who are not necessarily overly picky, REYN is front-and-center. This point does have its drawbacks, however, as during a period of inflation (such as currently), consumers may become more picky and not see sufficient value in REYN.

- Innovation and Research: REYN has invested significantly in R&D to drive continuous product development to keep ahead.

This high brand recall has a positive compounding impact as consumers can rely on its products, retailers provide preferential treatment and maximum stocking, and launching new products becomes easier.

Competitive Positioning

Despite its strong competitive position, REYN has struggled to achieve standout growth, attributable to overarching factors in its industry:

- Simplicity of products: Many of REYN’s products are relatively simple in nature, which limits the degree of differentiation and thus pricing power. This creates sensitivity to pricing.

- Saturated Market Dynamics: New entrants and developments in production have contributed to saturation, once again limiting differentiation and the scope for aggressive pricing.

- Economic Sensitivity: The sale of home goods, alongside the premium nature of simplistic goods, leaves the company vulnerable to economic conditions.

- Marketing Strategies: The lack of innovative marketing limits the ability to disrupt the market and change the status quo positively.

Financials

REYN’s recent financial performance has been a mixed bag. Its top-line growth has been underwhelming, with a growth rate of +3.4%, +2.5%, (3.3)%, and (7.4)% in its last four quarters. In conjunction with this, margins have improved.

Operationally, Management has been poor in the last few years in our view. The recent improvement in margins is broadly attributable to softening inflationary pressures, alongside some positive pricing, while the business has bizarrely seen a negative partial offset due to lower pricing in its Cooking and Baking segment.

The broader market conditions are negatively weighing on the company, particularly due to the impact of higher interest rates on the housing market as consumers seek to scale back costs. This is primarily why growth struggles to remain positive.

Looking ahead, we suspect growth will remain muted until expansionary government policy can return, while margins will sequentially step up.

Capital IQ

REYN’s margin development has been disappointing since the company’s IPO, with EBITDA-M declining from 21% in FY16 to 17% in FY23. This is primarily due to the impact of inflation, with GM% falling by 5ppts since FY20.

REYN has struggled with rapidly increasing material costs, with an inability to lift prices sufficiently to offset the impact. Compounding this is a negative change in volume, particularly during FY21 and into FY22. This is highly disappointing for an FMCG business, suggesting its brand power and value proposition are not sufficient to offset cyclicality.

As inflationary pressure continues to subside, REYN will likely experience a natural improvement, although we are hesitant to suggest this will be sufficient to wholly return to its pre-pandemic levels. The company has also been negatively impacted by wage inflation, impacting both the cost of sales and operating costs.

Capital IQ

Presented above is Wall Street’s consensus view on the coming years.

Analysts are forecasting mediocre growth in the coming years, with a CAGR of 0% into FY27F. In conjunction with this, margins are expected to incrementally improve to an EBITDA-M of ~20%.

The growth forecasts are disappointing and below what we are expecting, suggesting the negative conditions in the housing market are expected to continue in the short term. Further, a degree of this is likely associated with brand weakness and a slower recovery in its Cooking and Baking segment.

Further, we consider the margin improvement forecasts to be highly bullish. We are less convinced due to the limited gains achieved thus far. We expect EBITDA-M to normalize closer to ~18%.

Balance Sheet & Cash Flows

Following a period of restructuring, REYN is reasonably financed, with an ND/EBITDA ratio of 3.1x and interest comprising 3% of revenue. This positions the business well to maintain and grow its distributions, particularly as its FCF margin has been reasonably good. Further, this provides REYN with the optionality to conduct M&A to improve its growth trajectory.

Capital IQ

Industry Analysis

Seeking Alpha

Presented above is a comparison of REYN’s growth and profitability to the average of its industry, as defined by Seeking Alpha (12 companies).

REYN’s performance relative to its peers leaves a lot to be desired. The company’s margins are slightly below its peers, although the gap widens on an FCF and ROTC basis. This is attributable to its greater-than-average negative influence from macroeconomic conditions.

The company has performed better from a growth perspective, however, and so if it is able to improve margins sufficiently, REYN could quickly become a leading player in the industry.

Valuation

Capital IQ

REYN is currently trading at 12x LTM EBITDA and 12x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, owing to the execution risk associated with margin improvement, as well as the weaknesses identified following the recent decline in financial performance.

Further, REYN is trading at a ~30% discount to its peers on an LTM EBITDA basis and a ~25% discount on a P/E basis. We consider the current discount broadly reasonable, although we would suggest closer to ~20%. This would adequately reflect its current weakness while accounting for potential improvement.

Based on this, we broadly consider REYN to be adequately valued, although suspect an improvement in execution will rapidly contribute to the stock being undervalued. Investors with greater risk appetite may consider this a good entry point.

Key Risks With Our Thesis

The risks to our current thesis are:

- [Upside] Strong performance in e-commerce markets.

- [Upside] Expansion overseas through retail relationships.

- [Downside] Further struggles with rising raw material costs.

- [Downside] Inability to adapt to changing consumer preferences contributing to brand erosion.

Final Thoughts

REYN is a solid FMCG business, owing to its leading brands, unrivaled market reach, and scale. This said, its cyclicality and broader weaknesses illustrated in recent years leave much to be desired. We do expect its performance to improve in the coming years, although would like to see further proof before considering the stock a buy.

Read the full article here

")

")

Q2 2025 Earnings Call Transcript")

")

")

")

")