")

Since the initial SPAC approval, the whole focus of Trump Media & Technology Group Corp. (NASDAQ:DJT) has been the expiration of the major share lockups from the going public process. The main focus is definitely former President Trump’s shares, amounting to the majority of the company. My investment thesis remains ultra-Bearish on the stock following another weak quarter and the large share lock-up expiration in September.

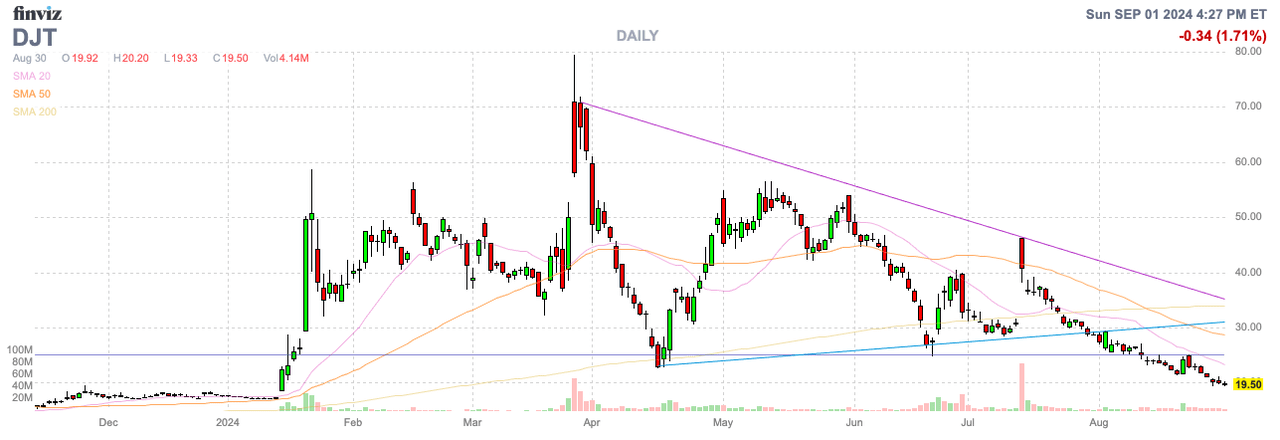

Source: Finviz

Another Dismal Quarter

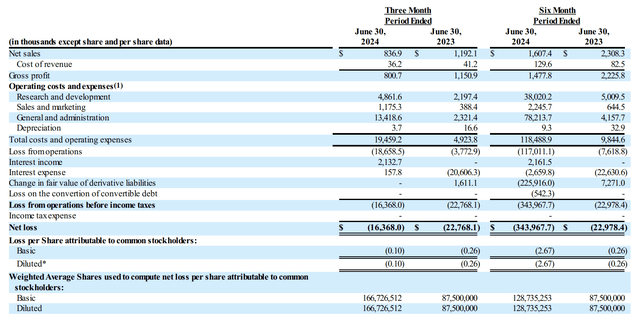

Back in early August, Trump Media released Q2’24 results without providing investors a lot of details. The social media company reported revenue slid below $1 million while expenses jumped, mostly due to going public costs.

Source: Trump Media Q2’24 10-Q

The original SPAC deal was announced in late 2021 and the Truth Social site was launched in early 2022, yet the business hasn’t really evolved much. Even worse, Donald Trump recently started posting on Twitter/X again after doing a Spaces interview live with Twitter/X owner Elon Musk.

Trump posts on X can get 5+ million likes/hearts, while similar posts on Truth Social only get likes/hearts in the thousands. A similar post on Israeli hostages on September 1 got only 14.4K likes on Truth Social, while the X post had 8.3 million likes.

The case for owning Trump Media has only gotten weaker, as the business hasn’t taken steps to expand since the going public process started nearly 3 years ago. The company has recently launched a CDN and closed on the transaction for the streaming technology business, leading to the launch of Truth+.

As with Truth Social, Trump Media has launched businesses without any real detail on how the media company is going to turn a TV streaming service into a real business. The company hasn’t actually announced any new content partners on either platform to build on former President Trump’s audience.

As with the prior quarter, Trump Media didn’t provide any usage metrics for Truth Social, including popular user counts. The company hasn’t provided any data on how the business is going to grow users, engagement and hence ad revenues

Trump Media only lost $16 million in the quarter, though the company hasn’t provided any indication of the spending level required to boost traffic and grow revenues.

Big Lock-up Expiration

Since the finalization of the SPAC deal on March 25, the whole stock story has centered around the lock-up expiration, specifically on the shares owned by Donald Trump. After the 40 million earnout shares, of which 36 million were earned by Trump, were executed on April 26 with the stock trading above required levels, Trump now owns 114.75 million shares with a lock-up expiration officially on September 25.

Due to rules surrounding the stock trading above $12, the lock-up expiration could actually end on September 20. These specific rules designed to bring forward the lock-up expiration a meager 5 days would suggest some level of interest in unloading shares.

Source: Trump Media prospectus

In combination with ARC Capital and others, shares under lock-up agreements controlled 70% of the shares and warrants outstanding. All of these shares will be open to sell within the next couple of weeks.

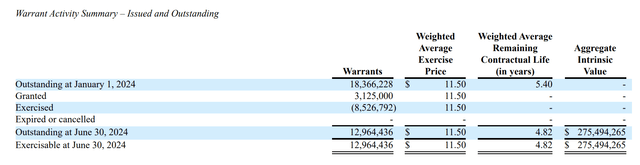

In total, Trump Media had ~191.5 million shares outstanding at the end of Q2. The company still lists 13 million warrants outstanding with an exercise price of $11.50 after 8.5 million have been exercised.

Source: Trump Media Q2’24 10-Q

The company recently issued up to 5.1 million shares for access to the IPTV business for their streaming technology. In addition, Trump Media recently signed a SEPA with Yorkville Capital in order to raise up to $2.5 billion by selling no more than 38 million shares (19.99% of outstanding shares) at a 2.5% discount to the current price.

In essence, Trump Media could attempt to raise cash at the same time that insiders are freed up to dump shares. So far, Donald Trump hasn’t made any apparent disclosure of any plans to sell any shares, but naturally the former President could use the cash during a bid to return to the White House.

Trump has nearly $2.2 billion worth of stock, with shares trading at $19.50. The big issue for the former President is that any decisions to sell shares could tank the stock.

The company ended Q2 with a cash balance of $344 million, and the additional warrants could raise another $150 million. Trump Media doesn’t have any clear need to raise any additional cash at this point, but the media company did sign the SEPA with apparent interest in raising additional funds to build a media empire.

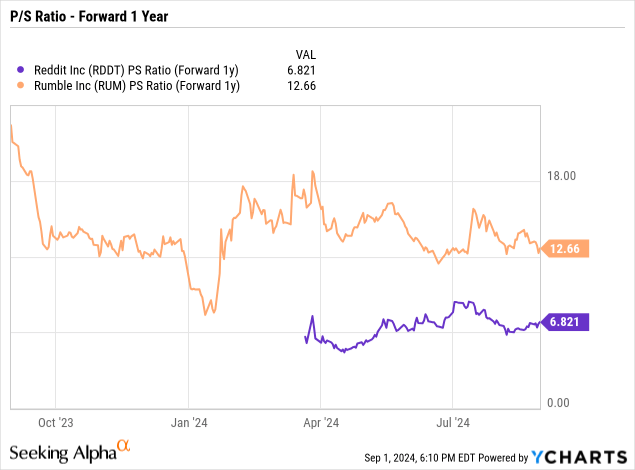

Trump Media doesn’t have any analyst targets, but social media peers that have most recently gone public trade around 10x forward sales targets. Rumble (RUM) trades at nearly 13x sales targets while Reddit (RDDT) trades at only 7x while Trump Media has a market cap topping $4 billion and revenue estimates for 2025 can’t be much above $10 to $20 million, at this point.

The valuations would definitely suggest insiders have every reason to start unloading shares. Rumble is only worth $1.6 billion, despite having revenue expectations for 2025 in the $129 million range.

The company has a faced a difficult time ramping up usage and ad revenues due in part to advertiser strikes against the platform and the lack of exclusive content. Most content providers still use YouTube and TwitterX due to much larger user bases, thereby, reducing the need for users to go directly to Rumble.

One has to really question how Trump Media tops the Rumble business or grows to match Reddit, yet the stock is already valued in the middle of these 2 businesses. An investor would have to use fairly aggressive targets to even value Trump Media at $500 million with a current $4 billion valuation. At 10x forward revenue estimates of peers, the social media company would need to generate an unlikely $50 million in 2025 sales, or the company would need to produce $10 million in sales and obtain a 50x P/S multiple. Neither outcome appears likely for the stock.

Takeaway

The key investor takeaway is that investors need to brace for major downside risk in Trump Media with the upcoming lock-up expiration in the next few weeks. The insiders haven’t announced any intentions to sell shares, but the logical move would be to cash out shares at the current valuation, considering the lack of progress in developing a viable business worthy of the current valuation.

Read the full article here