")

While most of the stock market has performed well in recent months, some segments have not kept up. Notably, the transportation industry has struggled with lower demand and, more importantly, significantly higher operating and input costs. That trend is evident from air travel to ground package transportation. Fundamentally, the cost of paying transportation operators is rising too quickly compared to the demand for transportation, stemming from the industry’s labor shortage. Previously, high fuel prices also created issues for the transportation industry. Still, the wage issue is large enough that costs typically have not declined despite a significant drop in fuel costs since 2022.

One exciting example is United Parcel Service (NYSE:UPS). I covered UPS around the end of 2022 in “United Parcel Service: Solid Q3 Report, But Freight Headwinds May Grow Dramatically In 2023.” The stock has lost 12% of its value since then despite a 30% rise in the S&P 500. Admittedly, only a tiny portion of my thesis proved correct. In 2022, I believed that an economic slowdown combined with higher wage pressures would significantly negatively impact UPS’s income. Since then, we’ve seen general economic stagnation (in manufacturing) but no recession. Yet, continued cost pressures still weigh on its bottom line.

Today, most analysts remain bullish on UPS, usually citing its depressed valuation and growth potential from its AI investments. Both of these factors are undoubtedly positive notes for UPS. It is at a slight discount, and the company will likely see lower costs as it lays off ~12K workers (~2.2% of its workforce). These workers are generally in management-type positions, which are being replaced with AI. UPS is expected to save $1B from this change, although much of that will only partially offset higher costs from union agreements.

Although this change will not dramatically improve the firm’s bottom line, it indicates potential for long-term improvement through greater AI adoption. Still, in light of the macroeconomic environment facing transportation, UPS requires closer analysis to assess its immediate and long-term potential.

Immediate Profit Potential for UPS

We must consider two aspects of UPS: its immediate income horizon and its long-term growth. Often, these two horizons can become confused. For example, the impact of AI growth for UPS is likely inconsequential in the short term, only aiding in the layoffs of a tiny portion of its sales employees.

However, in the long term, more than two to three years out, AI may replace a more significant portion of the company’s logistics and even potentially its drivers. On that note, the company has been actively testing driverless trucks with Waymo and its warehouse using autonomous guided vehicles to move packages around for years. UPS drivers will make ~$170K on average following recent union deals, making them among the highest paid in the industry.

If the company can overcome the technical challenges in automating some, most, or all of its tasks, it will save a considerable portion of its spending. Still, that is a long-term potential. It is not guaranteed, and any profit gains from it are subject to the competitive risk that UPS’s peers will pursue the same technologies, which is virtually certain. Further, these investments may have high initial CapEx costs that add to short-term pressures.

Still, I believe UPS has more to gain from AI than the technology firms developing artificial intelligence. For the most part, I expect the labor-heavy transportation industry will likely have the most overall upside from AI investments, particularly given the negative impact union deals have had on profits in recent years. That is not a statement regarding the ethics or morality of AI replacing these jobs or of unions, but an objective fact that investors must consider.

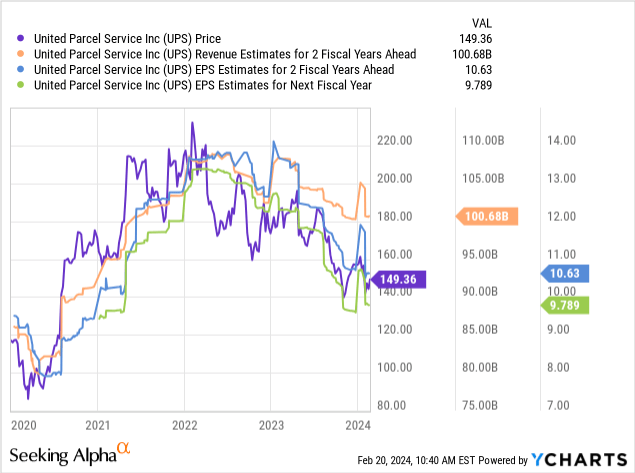

The recent union deal represents a 3.3% compounded annual increase through 2028, indicating above-inflation wage growth if we assume inflation will remain near current levels (which is not necessarily true). Still, with this in mind, it appears likely that UPS will face continued profit struggles over the next year or two. The current EPS projection from the analyst consensus sees UPS’s income falling to $8.28 per share by 2025, down from nearly $13 at its 2022 peak. Thus, there is a growing gap between the company’s poor immediate horizon and its long-term growth potential from AI investments.

Again, the short-term horizon for UPS is declining, showing a reversal of the profit gains since 2020. See below:

UPS’s primary issue is the negative margin impact of higher wages on its union employees. That said, the company’s revenue estimates have also been slipping, with a ~5% overall loss since 2022 despite continued inflation. In other words, UPS is also facing a decline in demand stemming from stagnation and a slowdown in the manufacturing sector. In my view, based on the position of US households, financial stability points to a decline in consumer spending that I expect will continue to strain its sales estimates.

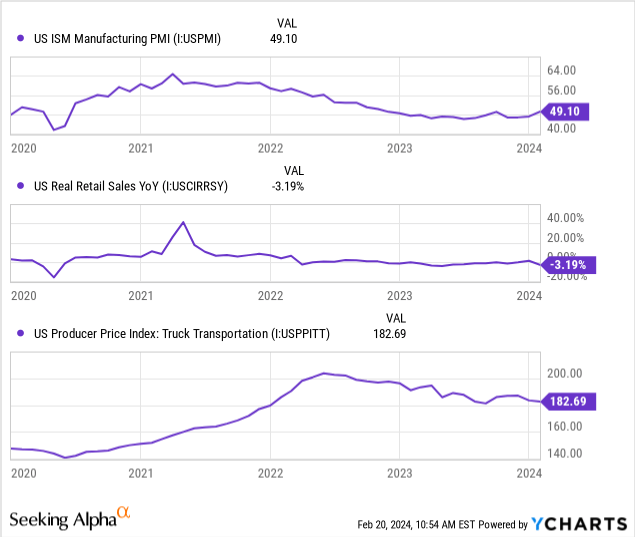

The economic front remains subpar. The manufacturing PMI remains at 49, indicating a slight declining trend despite moderate improvement. Real retail sales, however, are now declining at a fast pace of ~3.2% annually, indicating a negative trend growing in the goods market. Further, the PPI for truck transportation is on a steady negative trend. See below:

Problematically, UPS’s cost trend is decidedly positive, with its recent layoffs likely hardly offsetting the negative headwinds on the economic front. The economic issues include the apparent rise in costs associated with the labor shortage. That said, investors may underappreciate the growing demand headwinds, as indicated by the falling transportation PPI and consumer demand for goods.

The Bottom Line

Overall, there appears to be a sharp dichotomy between the company’s short-term outlook and long-term potential. I believe investors would be best off valuing the company based on the negative short-term headwinds. That is not to say the growth potential from AI will benefit it over the coming years, only to say that the negative immediate trend is clear and very likely, while the long-term benefits from AI remain unproven and unestablished. Mainly, if we see a further deceleration in demand factors combined with rising costs, I expect UPS will see its EPS outlook continue to decline, resulting in a further decline in its equity value.

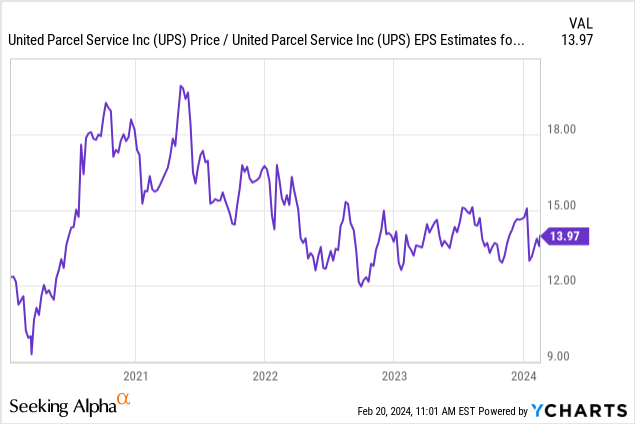

For the most part, UPS’s forward price-to-earnings based on its two-year ahead estimated EPS has been fixed since its reversal in 2022. Currently, that figure is around 14X. See below:

Over the past five years, UPS has had a TTM “P/E” average of 16.4X (non-GAAP). Its current non-GAAP forward “P/E” is higher at 17.9X, but its two-year ahead valuation is lower than the average. To me, that indicates UPS is valued today with the general view that its EPS outlook will not continue to deteriorate and that its income will rebound after around 2026.

Without a doubt, I believe that makes UPS not significantly overvalued or undervalued today. That said, I continue to have a slight bearish bias on UPS because it seems the full extent of its headwinds are not accounted for. Notably, the decline in its revenue associated with the reversal of strong retail sales conditions created ~2021, stemming from the excessive rise in credit card debt combined with the stagnation in median wages compared to consumer prices.

For these reasons, I believe UPS would be most fairly valued at ~$120, as I expect its income to fall back to pre-COVID levels. However, it is within a reasonable valuation range, so UPS is certainly not a short opportunity today.

Read the full article here