")

Vertex Pharmaceuticals (NASDAQ:VRTX) announced yesterday it will acquire Alpine Immune Sciences (NASDAQ:ALPN) for $65 per share, which translates to $4.9 billion market value or $4.6 billion net of cash. Vertex is gaining povetacicept, a phase 3-ready clinical candidate for the treatment of IgA nephropathy with pipeline in a drug potential for rare kidney diseases and also in autoimmune cytopenias. Vertex is also getting Alpine’s protein engineering and autoimmune expertise that it claims can be used to develop treatments for diseases Alpine was working on and also for diseases of Vertex’s ongoing and potential interest. And finally, Vertex is also inheriting two big pharma collaborations, but both seem to be going nowhere.

I rate this acquisition as negative in the near-term as povetacicept is 3+ years away from generating revenue for Vertex, neutral to slightly positive in the medium-term and potentially very positive in the long run, assuming povetacicept can live up to its pipeline in a drug potential. Vertex is up 13-14% since my previous article where I downgraded the stock to neutral/hold based on the lack of upside compared to my valuation range and I remain neutral despite this week’s acquisition and an increase in the valuation range from $332-$363 to $372-$411 per share.

Deal terms

Vertex has agreed to pay $65 for Alpine Immune Sciences, a fully diluted market cap of $4.9 billion and an enterprise value of $4.6 billion. The deal is expected to close this quarter, subject to customary closing conditions and Vertex will use cash on hand to fund the acquisition.

Povetacicept is largely de-risked in IgA nephropathy with pipeline in a drug potential

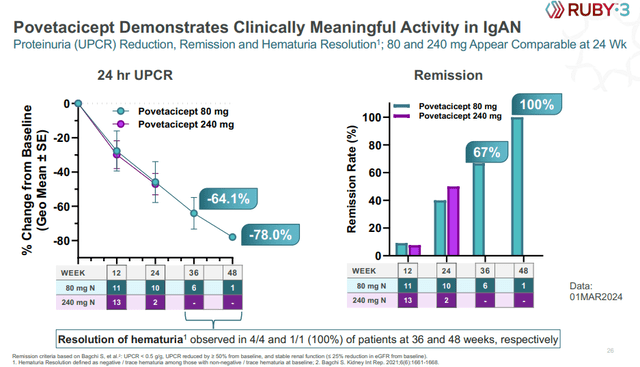

Povetacicept previously generated positive results in IgA nephropathy (‘IgAN’) patients and the updated results Alpine reported yesterday look similarly impressive. The number of patients at later time points is still very small with only six patients in the 80mg dose arm reaching week 36 and just one patient reaching week 48 in the trial, but proteinuria reductions look very strong and so do remission rates.

Alpine Immune Sciences investor presentation

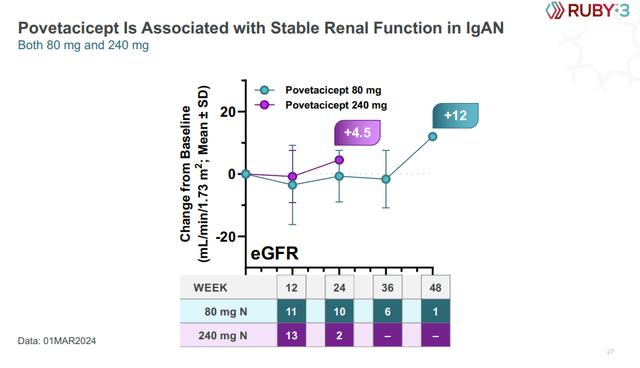

Importantly, eGFR data look strong with stable readings or improvements, depending on the time point, but with the same caveat of a small number of patients at later time points.

Alpine Immune Sciences investor presentation

Povetacicept also reduces several key disease biomarkers and it was well tolerated following multiple subcutaneous injections every four weeks and without causing severe infections or hypogammaglobulinemia.

These proteinuria reduction levels would put povetacicept in an excellent competitive position and it is no coincidence that Vertex is claiming it is acquiring a best-in-class candidate for the treatment of IgAN. Proteinuria reductions of acquired products like Filspari and Tarpeyo are 45% and 34%, respectively, or 30% and 29% placebo-adjusted, respectively.

But the IgAN data are far from being the only reason for the acquisition of Alpine. Povetacicept can become a true pipeline in a drug as Alpine is conducting two basket phase 1b/2 trials. The first is a kidney basket trial in IgAN, lupus nephritis, membranous nephropathy, and ANCA vasculitis, and the second is a basket of autoimmune cytopenias with povetacicept as a potential treatment for immune thrombocytopenia, autoimmune hemolytic anemia and cold agglutinin disease. Alpine and Vertex expect to report data from both basket trials in the second half of the year.

The other potential reasons for the acquisition are discussed in the next section of the article, but it is clear that the substantial majority of the valuation is based on povetacicept due to its impressive IgAN data and the upside potential in up to seven additional indications.

The U.S. prevalence of IgAN is 130,000 patients with an approximate market value of $13 billion based on the current annual price of the competing product Filspari. I am a bit cautious about the market penetration rates given the very disappointing uptake of currently approved drugs in IgAN but also in lupus nephritis which povetacicept is also targeting and which I will discuss in the valuation section. However, should povetacicept generate more impressive clinical data than existing treatments with acceptable safety, physicians are likely to be more motivated to prescribe drugs for the treatment of IgAN and patients themselves should be more motivated to start taking and staying on a drug like povetacicept.

Vertex Pharmaceuticals investor presentation

Vertex also gets protein engineering and autoimmune disease expertise and collaborations with Amgen and AbbVie

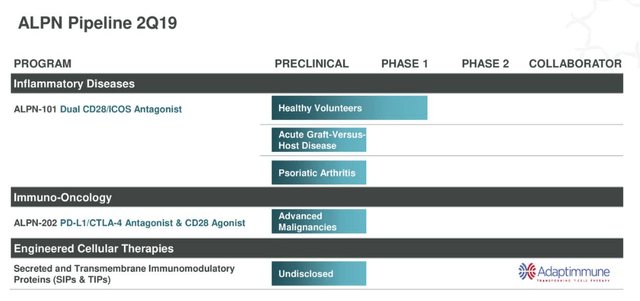

Vertex is also getting Alpine’s protein engineering and autoimmune disease expertise. If we are to judge by povetacicept’s profile and the impressive clinical data it generated to date, this could translate to multiple additional quality product candidates and billions in additional annual peak sales in the 2030s, but this could just be recency bias. Looking back, Alpine is not immune to failure and this is how its pipeline looked like back in 2019.

Seeking Alpha, Alpine Immune Sciences 2019 presentation

ALPN-101 is now called acazicolcept and AbbVie (ABBV) attained an exclusive option on this program in 2020 and Vertex is inheriting this collaboration. However, the agreement was amended in December 2023 to stop enrollment in the Synergy study for the treatment of patients with systemic lupus erythematosus (‘SLE’) to allow for an early assessment of the data, and to reduce the potential milestone payments and royalties by 25%. The final analysis of the Synergy trial is expected by the end of 2024 after which AbbVie has 90 days to exercise the option. SLE is an extremely difficult disease for drug development and my assumption is that this trial will fail and that AbbVie will not exercise its option and that Vertex itself is unlikely to proceed with development of acazicolcept if AbbVie gives up.

Back in December 2021, Alpine partnered with my portfolio company at the time, Horizon Therapeutics, which was acquired last year by Amgen (AMGN), and the deal covered one of Alpine’s existing preclinical biologic therapeutic programs and up to three additional autoimmune and inflammatory diseases. According to Alpine’s 2023 annual report, Amgen terminated the non-exclusive option for the second target in January 2024 and the option for the third target expired. If Amgen chooses to develop the first program, Vertex will be entitled to development, regulatory and commercial milestone payments of up to $381 million and mid-single digit to low double-digit royalties on net sales.

For the time being, I would put the value of these collaborations at zero, and based on Alpine’s track record, I would also not put too high of a value on its protein engineering and autoimmune disease expertise.

Vertex still looks fairly valued at current levels

As I mentioned in the introduction, my view of the deal is negative in the near-term as the acquisition will not produce revenues at least until 2027, and I would not expect earnings accretion until 2029. For the time being, I would put a placeholder valuation of $18 per share on povetacicept and this is what Vertex is paying for it.

But Vertex is looking at the long-term upside and it could be significant. IgAN alone is a $1 billion+ a year revenue opportunity and the other three kidney indications could add +$1 billion as well and with reasonable probability of success. The autoimmune cytopenias are an open question, but I can see annual revenues in excess of $2 billion for the three targeted indications combined.

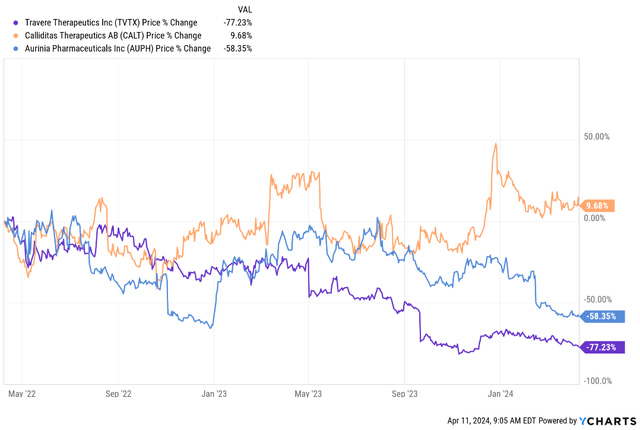

These estimates could prove conservative, particularly for IgAN and lupus nephritis, but I still think conservative assumptions should be made at the moment given the disappointing uptake of recently approved drugs such as Travere Therapeutics’ (TVTX) Filspari and Calliditas Therapeutics’ (CALT) Tarpeyo for the treatment of IgAN. Aurinia Pharmaceuticals’ (AUPH) Lupkynis has similarly disappointed in the lupus nephritis market, and the market has punished these stocks for underwhelming sales since launch with the exception of Calliditas as it launched Tarpeyo when its valuation was already quite low.

YCharts

The additional consideration for the IgAN market itself is increased competition down the road from the likes of Novartis (NVS) which acquired Chinook Therapeutics last year for $3.2 billion and gained two IgAN candidates with competitive proteinuria reduction.

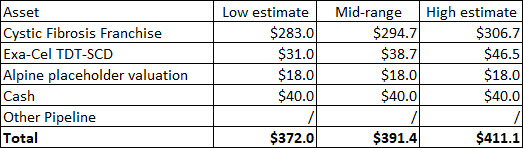

Going back to Vertex’s valuation, the passage of time adjustments, the increased valuation of Casgevy (exa-cel) following its regulatory de-risking (probability of approval going from 80% to 100%), the adjustment for the estimated year-end cash position minus the cash outlay for Alpine and the addition of $18 per share as the placeholder valuation for Alpine increase my valuation range from $332-$363 to $372-$411. I am still not giving credit to the rest of the pipeline which provides upside optionality to the valuation, but I do not consider the upside as material in the next few years. This means I remain neutral on Vertex as the stock is trading just below the high end of the range.

Author’s estimates

Conclusion

Vertex has finally made a sizable acquisition after years of very conservative business development activity and modest financial commitments through in-licensing and partnerships. I believe the acquisition of Alpine Immune Sciences is negative in the near-term as it only brings costs through at least 2027, and modest revenue generating potential in the next 5-6 years. Longer-term, the deal could pay off handsomely, especially if povetacicept generates positive data in one or more additional indications beyond IgAN.

I remain neutral on Vertex as I see limited upside for the stock based on my valuation range.

Read the full article here